MalibuJay

-

Posts

25 -

Joined

-

Last visited

Content Type

Profiles

Forums

Downloads

Posts posted by MalibuJay

-

-

Richard Barrow says that there has been a positive case identified in Chiang Mai. A press conference is supposedly coming soon with details.

https://twitter.com/RichardBarrow/status/1332513348378710016

-

2

2

-

1

1

-

-

I was in the Virgin Active Gym at about 10AM when the staff came through to tell everyone that Central Festival was closing in 5 minutes. When I asked why, they said it was for Covid cleaning. It looks like it wasn't planned. All of the staff were already in place in the shops and were ready to open at 10AM as usual. They're all standing around talking on their cell phones now or putting tarps over their displays. I haven't seen any information about it online yet. I can't confirm that it's for Covid, but I'm assuming that it's just a precaution. It's still odd that they didn't provide advance notice.

-

1

1

-

-

- Popular Post

- Popular Post

It closed a little earlier today as well. It looks like 8PM is the new closing time on Saturday. If you want to eat at a restaurant, plan to be there by 7:30 or before. Quite a few weren't accepting new diners after that.

-

1

-

3

3

-

33 minutes ago, TallGuyJohninBKK said:

I've been with them for years... But I've never heard or read anything about them having a verbal password.. other than the call in one we're both aware of... So, that whole thing is news to me!

How does it work? How/where do you use it?

You use it when you call them on the phone. Rather than asking you a set of security questions or using the voice recognition tool, they just ask for your verbal password. It's not in play when you log in to the website. Your standard username and password still works on the website.

-

1

-

-

4 hours ago, TallGuyJohninBKK said:

--the only voice password I'm familiar with re Schwab is not in place of a login ID or password, but instead is used for when you call them on the phone. In order to pass security for the phone call, you can set it up ahead of time by doing a voice recording over the phone where you say "With Schwab, my voice is my password." And then from then on, when you call in, you just repeat that phrase, and their system clears you to go ahead and talk with an agent without having to go thru all kinds of personal verification Q and As.

The verbal password was something different from the standard "With Schwab, my voice is my password" voice ID. If fact it superseded the voice ID along with everything else. I had previously used "At Schwab, my voice is my password" and they wouldn't let me fall back to that when I forgot the verbal password. I never understood why they thought they verbal password was especially secure. If you were logging in from a public place using that technique, everyone within earshot would know your password. One of the customer service reps suggested that I switch to that method when I was on a phone call with them. Maybe they've discontinued it now, I don't know. I wouldn't recommend using it, especially for overseas folks: if you're in the US, you can go into a branch office to reset it, but if you're overseas, you'll need a notarized affidavit and that could create a problem, as it did in my case.

The day may come at Schwab when they tighten up their procedures about this and implement more stringent, and even automated, checking for foreign residents, but for now the biggest risk seems to be letting it slip when you're dealing with the humans there. Just be aware that you need to keep it quiet. Masking technology geolocations when you can would be another prudent step. VPNs still seem to work quite well at the moment. There are probably quite a few US residents who access the Schwab site using a VPN as well. They're not going to want to have to ask every VPN user for a utility bill. It's not necessarily foolproof and it may not work forever, but for now it's another level of protection that can still make a difference.

-

1 hour ago, TallGuyJohninBKK said:

How/why did the issue of your residency status arise with Schwab?

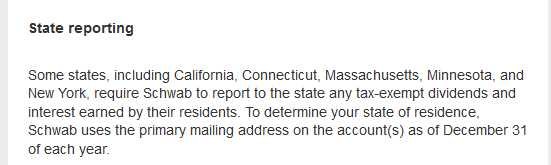

BTW, here is what Schwab has said in the past about how they determine a client's residency, and it does appear to be driven by the accountholder's reported mailing address, not listed physical address:

In my case, I didn't use my voice password for over a year and I forgot it. I thought I had it written down offline but I couldn't find that either. That became an issue when I needed to get a new debit card for the Schwab Bank account due to fraud. Apparently once you set up a voice password as your verification method, nothing else matters anymore. You are not allowed to answer security questions or do anything else to verify your identity. I had to submit a notarized form to get the voice password reset, and since I was in Thailand, I had to go to the US local consulate. That affidavit from Thailand set off bells for some officious Compliance officer and I awoke one morning to an email telling me that they were closing my US account in 30 days unless I provided proof of US residency.

So my unusual situation brought them face to face with the issue, probably due to manual handling of that affidavit, whereas otherwise they didn't seem to be on the lookout for a foreign residence and aren't automating their search for them, at least not yet. I had been doing regular ATM withdrawals in Thailand without triggering any problems. I have a friend however who made a habit of logging into his Fidelity account without masking his Thai ISP using a VPN, and then one day Fidelity intervened and forced him to switch to a foreign account, so they were monitoring ISP addresses. I don't think Schwab is policing ISPs yet, but they could. And if they wanted to verify that your mailing address is truly residential and not a P.O. Box, I suppose they could start that at any time too, like USAA apparently did. For now, if you're laying low with a US mailing address, you're probably OK.

Based on my experience, however, I would say: 1) never let them know that you live overseas; 2) if you do have to deal with them from overseas, allow them to assume that you are on a vacation trip and will be returning to the US soon; 3) always use a VPN with a US city IP address, preferably somewhere near your mailing address; 3) if possible, have a US phone number they can call you on that, again, preferably has a prefix that is consistent with your mailing address. I have a Skype number from a US city that rings on my computer and that is the phone number listed on my account. When I finally got the debit card issue straightened out, there was a point in the process when they made a robocall to that number to verify that I was in the US. I was able to pass that test. Now if I ever need to call Client Services, I always call them via that number which is set to show the US city caller ID. That has also come in handy. I have had them say to me, "I see that you are calling from your US number" and then assume that I am in fact in the US.

-

2

-

-

23 hours ago, JimGant said:

But what will become interesting is that, in a couple of months, my USAA Investments will be taken over by Schwab. Now, my account with Schwab uses my CMRA mailing address -- and when I recently tried to change it to my Thai address, I got a 'no can do' because my Schwab account is a domestic account. So, will be interesting on how all of this sorts out. I just might lose my Schwab Debit/ATM card, with if fee free bennies for international transactions. But, so be it, as these days I get all my baht thru SWiFT or TransferWise, so the Schwab ATM card is no longer the golden attraction it once was.

You may lose your Schwab Bank account altogether. If you have an IRA account at Schwab, they will also flag it as foreign and require a mandatory 10% withholding on all Distributions, which is an IRS rule for all non-US residents. Opening a International account at Schwab would require a $25,000 minimum and wouldn't allow you to have an associated Schwab Bank or IRA account, and wouldn't allow you to own mutual funds. I had quite a battle with them until I closed the IRA account to defuse that issue and pointed out that someone can be a part-time foreign resident and a part-time US resident each year, which should generally make you US for tax purposes if you spend at least 30 days a year there. Their systems are designed to make a black or white, US or foreign, classification without the sophistication to handle anything in between. They may ask you for a US utility bill if you want to prove you're US-based. Schwab can be messy with this kind of thing. I've managed to reach an uneasy truce with them and keep the Schwab Bank account after closing the IRA account, but I quit using it on a regular basis. I keep it now just to use the debit card when I'm traveling short-term on vacation in another country. I don't use it at all in Thailand. Now I do direct deposit.

-

On 2/18/2020 at 9:09 PM, Pib said:

After doing the update I logged off and back on again to check out my ibanking capability to see if I could still do things like add an external transfer acct, wire transfer, doing an ACH transfer, open a CD, etc.,--and I could. However, when checking to see if I could open a mutual fund I couldn't...the screen indicated I couldn't due to my address--probably their way of saying you can't open mutual funds with them if having a foreign address. That's fine....I don't have or plan to have mutual funds with USAA. I only did this mutual fund check since someone told me before when they had a foreign address onfile with USAA they couldn't open mutual funds with USAA due to the foreign address.

I'm pretty sure that the prohibition on owning mutual funds has to do with the complexities of tax withholding that it would create to have people with foreign residences holding the fund. If all holders are US residents, they can apply the simple US withholding rules, which basically bypass all withholding as long as you've submitted a W-4. If you are a foreigner, the game changes: you don't get to wait until the end of the year to file your return in one lump sum and pay whatever net taxes are due, and you don't get to bypass withholding. For you, withholding has to be deducted at the time the payment is made and sent to the IRS withing 24 hours, since the IRS doesn't have an easy and practical way of getting money back from a foreign resident and/or bank if you decide later on that you don't want to pay your US taxes. They might also have to do withholding on behalf of the foreign country in some cases, particularly if they have an office in that country, which gives the foreign country some leverage over them. So if Thailand thought that they had a right to some of the income your earned in the fund due to your full-time residence there, that might be a problem, though in reality it's the UK and Japan that have traditionally forced brokerages to do that sort of thing and not the smaller jurisdictions like Thailand. The world of non-resident withholding can get very complicated, particularly for mutual funds. It's pretty common to block mutual fund ownership for non-US residents with accounts at US financial institutions.

-

Central Festival is quiet too, especially at night. Never seen it like this before. Photos of the main food court at 8PM on Wednesday night:

-

- Popular Post

- Popular Post

I don't think comparisons to the number of people who die daily from heart disease or old age or traffic accidents are really valid. Everyone in the world has already been exposed to those risks. Those just generally reflect the size of the world or national population. What will the death numbers from Coronavirus look like after everyone in the world has been fully exposed to it, if that happens? Then maybe we'll have a valid comparison of that sort.

So far, what's going on is alarming. Have you ever seen restrictions on travel the size of what the Chinese are imposing now? I haven't in my lifetime. We didn't see this with SARS or even with Ebola. If they're trying to fake everyone out and create fear with a false flag, they're really going all in this time - even sabotaging their own GDP, and at a time when national economies are pretty fragile. They seem to be quite concerned about it.-

4

-

I haven't seen any milk kefir in Chiang Mai so far. Even the 2 places I know of that have water kefir (Blue Diamond Restaurant, Good Health store) don't have milk kefir. You could make your own easily enough if you're interested. Halima from HK Probiotics in Bangkok will mail you some grains to Chiang Mai via EMS which will arrive in about 2 days. Milk Kefir Grains. It's around 500 baht or so with postage. You can grow your first batch in less than 24 hours and they last forever.

-

1

-

-

I renewed my passport in Chiang Mai in September 2018. I read through CM Consulate website and it talked extensively about renewing by mail, but there was no obvious mention of renewing in person. I came away with the impression that perhaps it was no longer possible to renew in person, but by chance I had to go in that week to notarize something pertaining to another matter and I was able to ask them if I could renew in person. The answer was yes, so that's how I did it. It seems that they may favor renewal by mail now, so they may be trying to channel people into using that service.

-

1

-

-

The China ruling actually appears to be positive for Bitcoin from what I'm reading. They've essentially classified it as a commodity instead of a currency, which means that Bitcoin exchanges are free to trade Yuan for Bitcoin as they wish without the heavy handed government regulations and confiscations that US Bitcoin exchanges face. BTC exchanges in China are not "financial institutions", they're selling a commodity like rice, so they are free to proceed. Merchants and customers are also free to exchange using bitcoin. Banks and financial institutions cannot offer Bitcoin mutual funds or otherwise offer it to savers and investors, but it's fine for commerce.

That seems positive to me. I don't agree that Bitcoin cannot advance until it's a proper vehicle for savers. Savers will be the last group to adopt it. As someone said, "If my grandparents ask me how to conserve their wealth, I tell them to buy gold bullion. If they ask me how to transport it over distance, I tell them to send Bitcoin." Bitcoin is two things: the payment or transfer network, like PayPal, but also the currency unit (BTC) used on the network. It's as if PayPal had it's own currency unit. It's the utility of the network that should drive the growth, and since BTC is the only currency that can be used on the network and BTC are scare (fixed number of units), they should appreciate in value over time if the network's utility is recognized and adopted. With the current volatility in the price, it's true that current holders figure to be some combination of speculators and nerds (early technology adopters). But if merchants are agnostic and see bitcoin as an opportunity to pay lower fees on transactions, their adoption of the PayPal or network aspect of the technology could grow without savers. Perhaps someday an online merchant, when you place an order, can quickly direct you to a BTC exchange as they now direct you to PayPal, where you can instantly buy BTC for your currency and transfer them to the merchant, who can then instantly sell them and convert to his own currency. The customer woudn't need to BTC. The exchange would have to become a market maker, but isn't that hold gold/silver dealers do it, despite major swings in the metals prices?

As for whether a competitor could replace Bitcoin, they can and do copy the open source code and roll out new cryptocurrencies, but they can't easily replicate the infrastructure that's grown up around Bitcoin. How many miners are there in the other coins and who has even heard of those coins? Bitcoin has a nice head start and it should take years to catch up. What could they offer to offset Bitcoin's advantage, and why couldn't Bitcoin copy that anyway?

Whether it can be eplaced remains to be seen, but it should have utility and growth in the meantime.

I've been sitting on the sidelines watching Bitcoin until recently, but most of the negative comments in this thread have been rebutted in articles I've come across in just the last 72 hours. That doesn't mean that Bitcoin will ultimately survive, but it only takes a few days of research to see that the proponents of Bitcoin have given a lot more though to its problems than the naysayers. A lot of folks are just averse to change. It someone wishes that everyone would just stop changing things and leave them the way there are, there's little you can say to change those feelings.

-

1

-

Central Festival was just Closed for Covid Cleaning

in Chiang Mai

Posted

There is still uncertainty at the mall. It reopened sometime today and I was just there for coffee, but they are telling everyone to leave again as of 4PM and calling all the vendors into a meeting sometime later on. I am friends with one of the vendors. They're not sure right now if they will be open tomorrow.