Roojai

-

Posts

62 -

Joined

-

Last visited

Content Type

Profiles

Forums

Downloads

Posts posted by Roojai

-

-

Dear @watgate, thank you very much for your kind feedback. We shared it with our claim surveyor.

Dear @steve187, although that's true, we do manage the customer service during the accident, including claim support, and garage/hospital network relations.

Dear @Etaoin Shrdlu, we operate with a model called managing general agent, meaning that we are a broker that manages the entire journey, including product design, purchase, customer service and claims. We have one exclusive partner for each product. That includes, KPI for car, motorbike and cancer insurance; AXA for personal accident insurance; MuangThai for extended warranty insurance; and FWD for inbound travel insurance. And more products to come.

Regards,

The Roojai team

-

2

2

-

-

On 10/30/2021 at 11:07 AM, nahkit said:

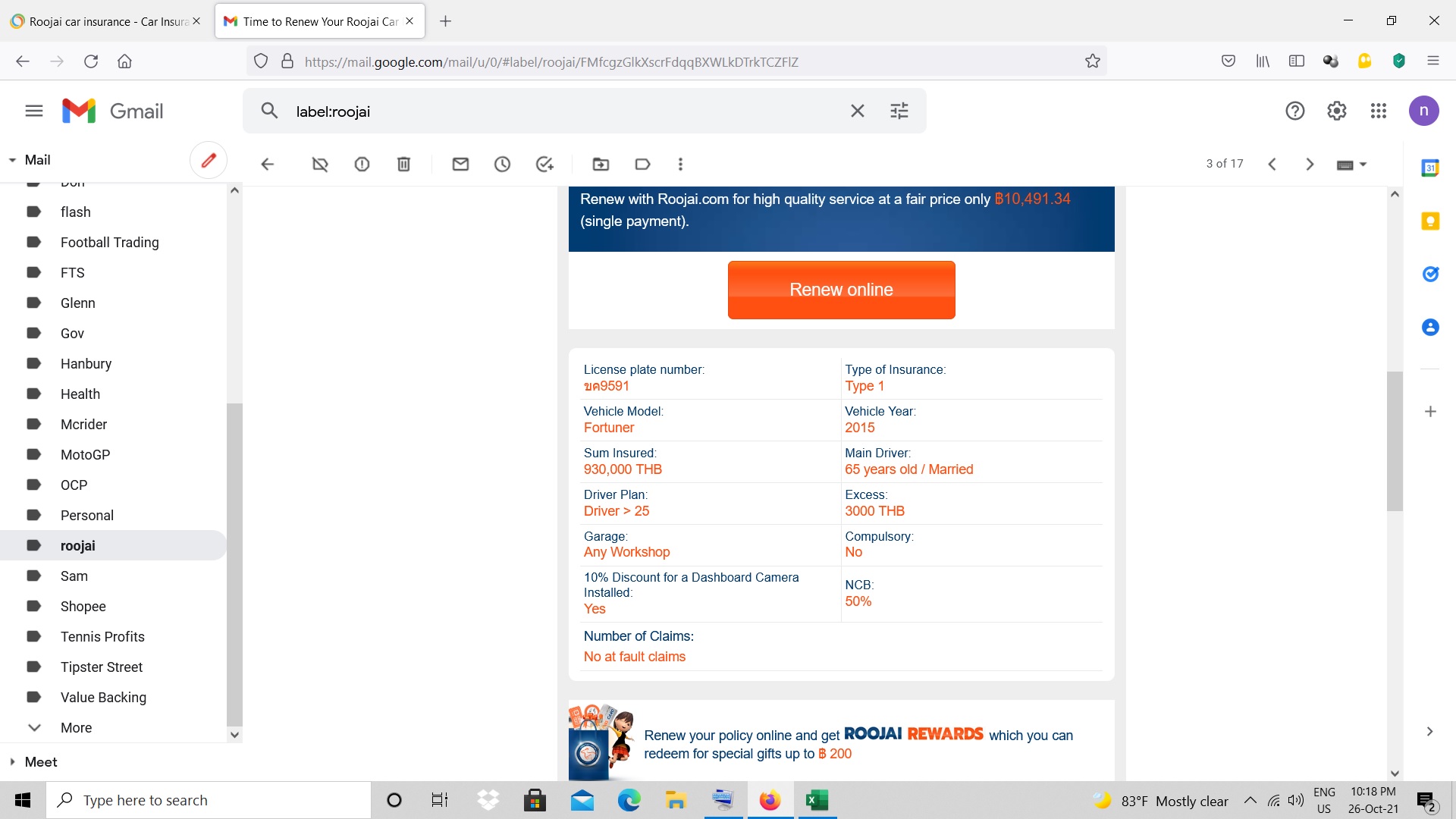

Seems you are the one still confused, the quotation I included in my previous post IS the WEBSITE quotation that I obtained, and it clearly shows under "Driver" that it includes any driver over 25. Your original renewal quote, dated August 22nd, was for 12,645.69 baht and also was for any driver over 25. I have saved the current renewal email containing the terms and will be happy to be post it here. I also have my renewal quotation for 2020 saved, which again is for any driver over 25. I did not request a named driver policy last year and I have not requested one this year.

So my "more expensive" option came in more than 2,000 baht cheaper than your renewal.

You appear to employ the same tactics as your phone representative, i.e. introduce spurious facts and continue to ignore the truth.

As for the the third-party 2 million versus 1 million quote, your agent said that the difference in cost between the two would add about 1,000 baht to the policy not the 2,154.35 baht extra you were trying to charge me on the renewal.

Dear nahkit,

This is Federico, Chief Marketing Officer at Roojai. Allow me to get involved here.

I verified with the call center, claim and social media teams, and all the information they provided are correct. Although, I do apologize if you feel they didn't communicate them properly. You have multiple quotes under your contract and for each one of them I can see there is some difference in the inputted parameters.

Our pricing model is based on dozens of parameters, it is fully automated and there is no individual decision made by any of our agent, nor there are any individual decision taken for any given customer.

We are fully aware that this is a free and open market. We try hard to provide great service at a competitive price for all our customers at all time of their policy lifecycle. We have very competitive market with almost 60 insurers in Thailand, fighting for your business.

If you feel at any time that we are not offering the best value for money I do encourage you to compare quotes in the marketplace. I do suggest to use a comparison website like MrKumka.com (disclaimer: they are a sister company but they offer many insurance quotes other than from Roojai). There are many more available online.

We hope you will find us the best for your needs, but in case we are not, we do fully understand your decision not to renew your policy with us.

We never take any of our customer for granted.Kind Regards,

Federico

-

On 10/28/2021 at 8:47 AM, nahkit said:

Thank you for your detailed reply, however, your answers are just as confusing as when I talk to your telephone operator.

With regard to repairing the vehicle at our garage of choice, the delay had nothing to do with obtaining 24 hour advance clearing, we were still receiving problems from the garage regarding not wanting to do the repair more than one week after the car had been taken to the garage.

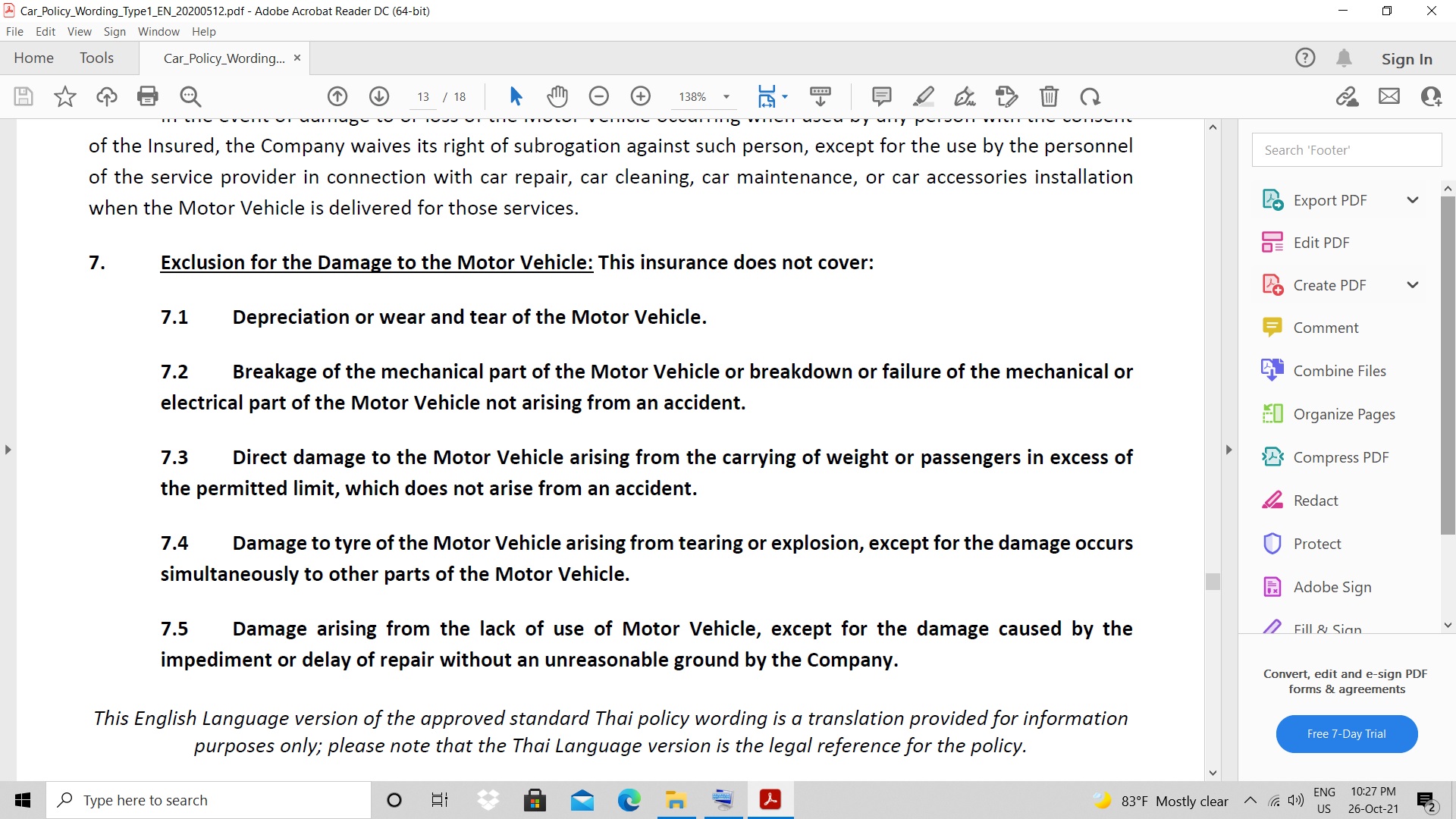

As for the fluids being considered "regular wear and tear" same as tyres, where exactly in the policy does it state that fluids are not covered?

The above is from the insurance coverage booklet provided in English. Section 7.4 states that tyres are not part of the coverage, where does it actually state that fluids are not part of the coverage?

Finally, your statement that the difference in the renewal quotation and the one I obtained online is down to my requesting "named driver" is plain wrong.

The following attachment shows the online coverage quotation I obtained following your renewal quote asking for more than 12,000 baht. You can clearly see that I have requested coverage for "any driver over 25 years of age".

I look forward to your reply, particularly as to why there is no mention of fluids in your coverage exclusion details.

Dear nahkit,

It's the exclusion clause 7.1.

The fluid itself is a consumable part. As such, it is part of the depreciation or wear and tear exclusion.

A wear and tear exclusion is a provision in an insurance policy that states that the normal deterioration of the insured object is not covered by the insurance policy. Insurance is designed only to protect against unforeseen losses. Wear and tear is a common exclusion in property and casualty insurance all over the world.

The fluid change was judged by the claim handler as not part of the necessary repair caused by the claim.

Regarding the different quotation, there is some confusion here. We were talking about the difference between the original renewal quote and the website quote. That is because of the different driver plans: any driver over 25 for the renewal quotation (more expensive), named driver on the website quotation (cheaper).

Regarding the successive renewal invitation after you discussed with the agent, it's because of the reduced coverage in Third-party bodily injuries: 2 million THB for the original renewal quote, 1 million THB for the successive version (max. 10 million THB in both cases).

Finally, regarding the garage experience, please do consider that once you will receive the satisfaction survey for the overall claim. We do show those garage ratings in the garage map so customers can choose their repair garage accordingly.

Regards,

The Roojai team

-

1

-

-

- Popular Post

- Popular Post

On 10/20/2021 at 8:09 PM, nahkit said:I got the call back a couple of hours after I posted and ended up paying slightly less than the online quote and around 2,100 baht less than the renewal quote.

Trying to find out why I had received a much higher renewal quote was a waste of time, went round in circles for about 10 minutes at which point I decided it wasn't worth the hassle.

Dear nahkit,

Apologies for the long wait during the claim process.

Regarding the repair process, although the "Repair at any garage" option gives you total freedom, we do ask customers who decide to repair their vehicle at another garage not in Roojai’s garage list (preferred or dealer), we do ask them to contact us at least 24 hours in advance so that we can make arrangements with the garage to accommodate them. We need to have a letter of agreement even with those who are not in our preferred garage list.

Sorry if the agent was not clear in explaining why the fluids were not covered. The reason is that they are a consumable part of the vehicle, and are considered as regular wear and tear of the vehicle. Same, for example, why tires replacement for simple wear and tear is not included in the coverage.Finally regarding the difference between your new customer quote and renewal quote, it is mainly because you selected different driver plans: “any driver over 25 years old” for your renewal, and “named driver” for the new business quote.

Our pricing model is automated and based on several questions we ask before giving you a quote. We do not ask for nationality before providing a price. And the individual agent has no way of influencing the customer quotation, other than suggesting different coverages, as changing excess, driver plan or garage plan.

We hope this clarifies the points.

The Roojai team

-

4

-

Hi Ryan,

Do you mean you want us to answer some of your questions here?

Regards,

The Roojai team

-

1 hour ago, poohy said:

bought 9 April got diprahaya

You are right, poohy. The renewal was stopped on 12th April, not two weeks ago.

My bad.The Roojai team

-

48 minutes ago, scubascuba3 said:

Not sure about that, lot's of unanswered questions Roojai doesn't seem to want to answer

Hi scubascuba3,

What is the question you would like an answer on?

The Roojai team

-

1

-

-

On 5/18/2021 at 10:27 AM, Tanoshi said:

It would be extremely helpful and answer some questions if Roojai could confirm the date they changed their Covid advertising campaign to KPI on their website.

I only noticed the change 2/3 weeks ago.

Hi Tanoshi,

There are three level of approval from OIC for a new insurance product: traditional sale, telesale, online sale. We launched the KPI product two months ago but were only allowed to sell it through telesale, and kept the Dhipaya product on the website for online sale. On the last week of April we launched the KPI product for online purchase from new customers but kept the renewal customers on the Dhipaya product. Two weeks ago we stopped selling the Dhipaya product even for renewal customers.

Regards,

The Roojai team

-

1

1

-

-

12 minutes ago, scubascuba3 said:

but you sold me the "illness with serious conditions" then subsequently switched it to "coma" only, how can that be right? I'll put it another way, i buy a Honda Click and you switch it after to a Honda Wave for the same price and think that's just fine

Hi scubascuba3,

The policy wording is the same so it is the coverage. The change was only on the website based on the most common words used in the market. Rest assured that the policy covers the same situations.

Here is the policy wording, you can find the additional definitions on page 8.

https://www.roojai.com/policy-wordings/COVID19_policy_wording_version_online_22APR2021_en.pdfRegards,

The Roojai team

-

56 minutes ago, scubascuba3 said:

Hi Roojai

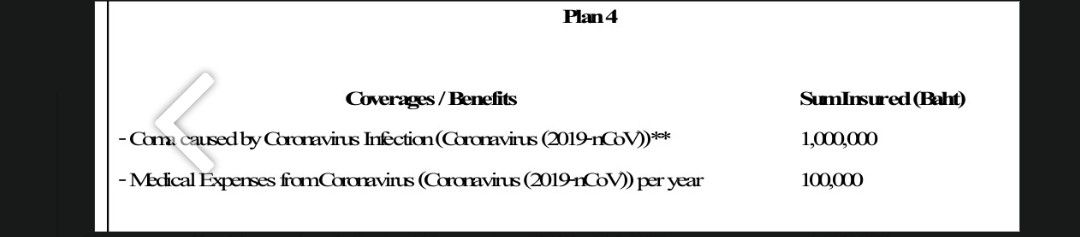

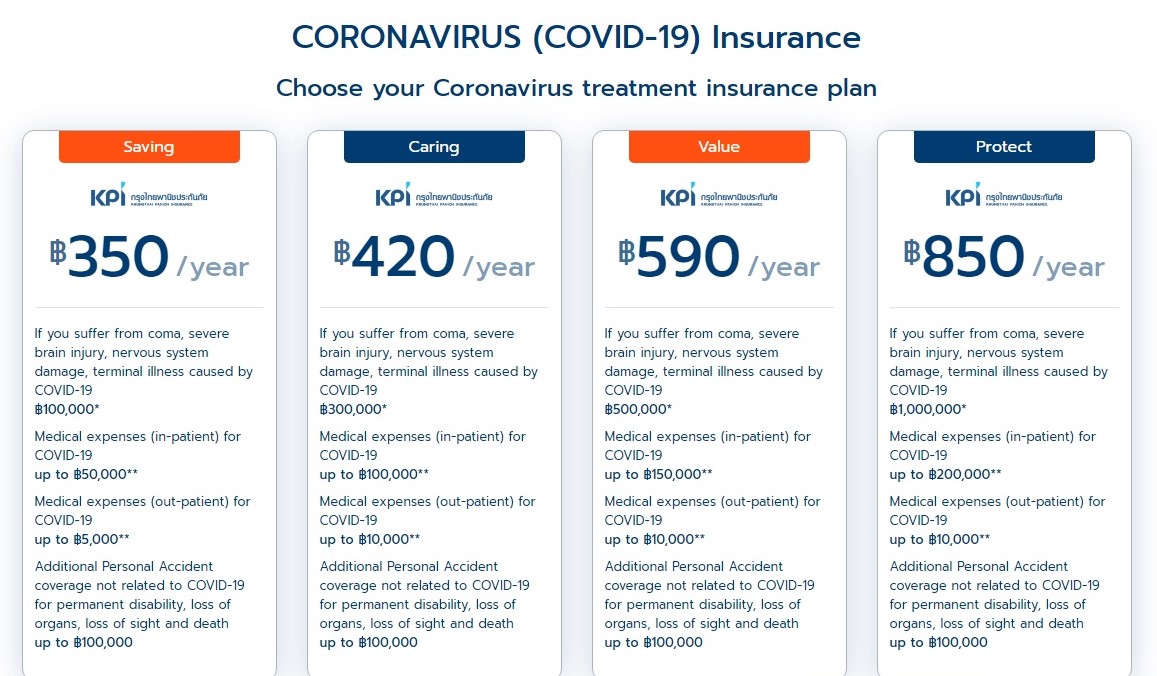

Can you explain the differences below, I signed up to Plan 2 (below) but what was emailed to me was plan 4 (below) which only specifies coma, can you see the difference?

Hi,

The coverage is the same. We changed serious conditions/terminal illness to coma to be in line with the rest of the market.

Regards,

The Roojai team

-

1

-

-

1 hour ago, sandyf said:

Can you please explain why the website states the coverage for medical Expenses(In Patient) would be 200,000 baht for Plan4(Protect), but the policy documents show it as only 100,000 baht.

Hi sandyf,

The comment you quoted is from 2020. That's about the Dhipaya covid-19 insurance product. We stopped selling that product a few months back. The product you shared the image of, is our exclusive product with KPI (only sold through Roojai). They are not the same product.We hope that clarify.

Regards,

The Roojai team

-

11 hours ago, Sheryl said:

Also possible this is just a glitch in the software. Suggest you call them or PM @Roojai

Hi Sheryl,

You are correct once again.

It's a cancer insurance exclusion wrongly applied to Covid-19 insurance.

The fix is already in testing environment and should go live by today.Regards,

The Roojai team

-

2 hours ago, scubascuba3 said:

An idea of the cost of the covid care would be useful? how far does the 100k last? thanks

Hi scubascuba3,

There is no easy answer and really depends on the patient conditions, the hospital, the province, etc.

Sorry but we are not able to give you a definite answer.

-

13 hours ago, Tanoshi said:

I took out the Covid policy a year ago and renewed it this year on 17th March.

I never received a confirmation email but did receive an SMS text with a reference number.

I would hope as this a renewal of an existing policy the 14 day 'waiting' period will not apply?

During Songkran I realised I hadn't received the new policy.

I called your service centre on 16th,19th, 20th, 21st and 22nd only to be promised a call backs, which never happened, hence I kept chasing. On 23rd my wife called, thinking perhaps in Thai she may get a better response. At no time did any of your operatives give any explanation for the delay.

Your operative asked if it could be sent by email, something I previously suggested, which saves on time and cost. Agreeing he promised to email the policy on Monday 26th.

I also sent a complaint via your online system, to which I have had no response

Guess what?

Monday 26th, no email, no contact to explain why and your office is now closed.

As an existing client of Roojai, with other Insurance policies, your service and responses do not do your company any favours in instilling any confidence to continue using your services in the future.

If there is/was a delay you could have blanket emailed existing clients to inform them of such.

The issue may be with Dhipaya Insurance, but you are the agent and as such this poor service reflects directly on your services.

It's now 41 days since you took the money from my account- it's utterly disgraceful.

How many more in the same boat. I don't seek an apology, I seek some action.

On 11th April you did send e an email:

Roojai.com customers can get unlimited Roojai Rewards by referring their friends.

Get ฿400 for each referred friend, and they get extra ฿100.

Refer more, get more!That was a little late for April 1st. (It is a joke, right).

Dear Tanoshi,

We will send you a DM to get the policy information and follow up with Dhipaya.

Apologies,

The Roojai team

-

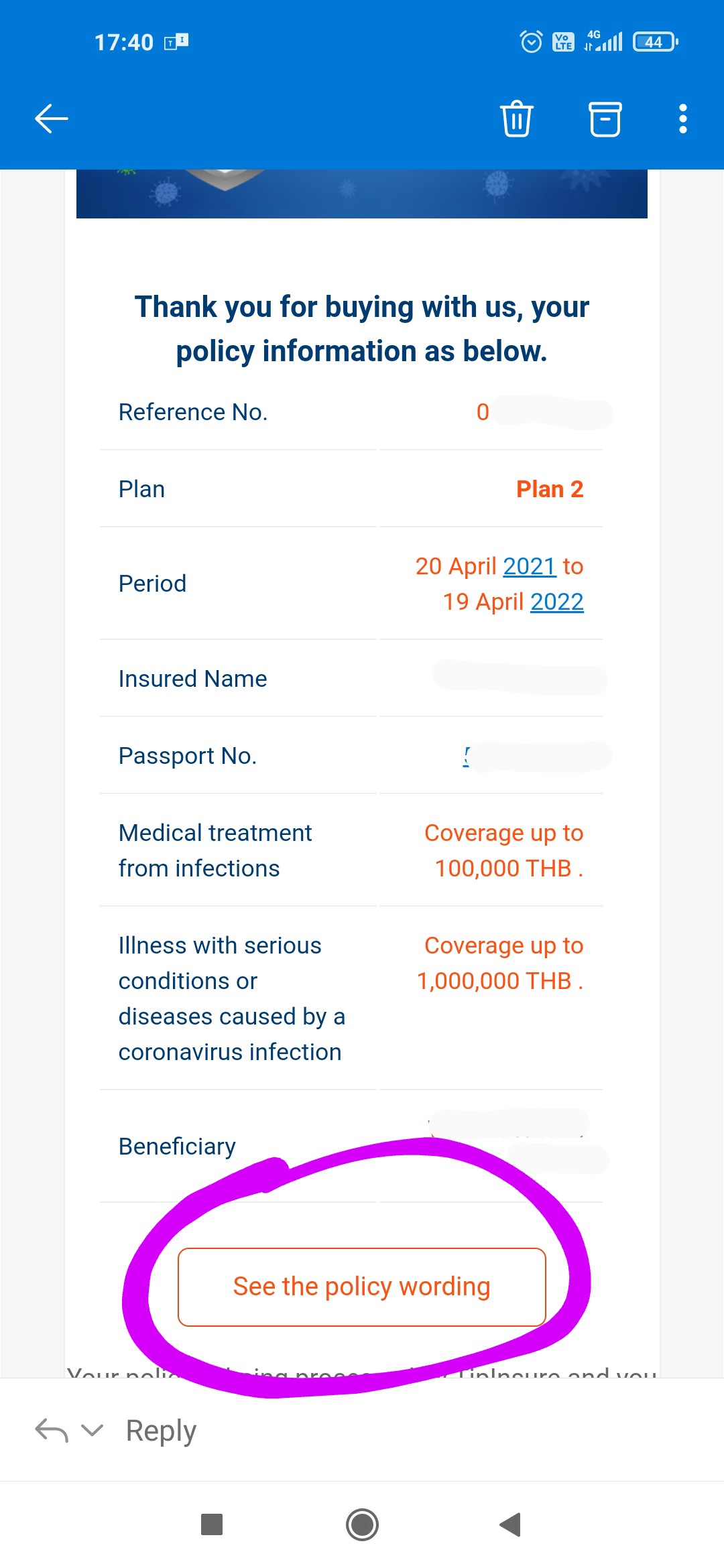

15 hours ago, scubascuba3 said:

Below is the email confirmation you get, if you click "see the policy wording" you can see the doc. Based on this email I'm assuming I'll get written confirmation in a few weeks (maybe). It doesn't give you much confidence in the potential claiming process.

But, i think this is a drop in the ocean anyway, I was chatting to someone yesterday whose farang father is in private hospital with Covid paying 30k a day, 14 days planned (420k), has to transfer 30k a day to get treated, so this insurance will last less than 4 days. No idea about costs of field hospitals and hospitels, no doubt falang will be fleeced.

Maybe @Roojaican give us an idea?

Hi scubascuba3,

Sorry, we don't get the question? Do you want us to clarify about the cost of medical care or about the claim process?

Regards,

The Roojai team

-

33 minutes ago, Phulublub said:

Roojai

Thank you for engaging with us. Can you give us a timeframe for when those of us who bought the Tipinsure policy will be receiving our documents? Will they be emailled, or hard copy?

PH

Hi Phulublub,

Unfortunately we cannot give a timeframe. We will send you a DM to get the policy details and follow up with Dhipaya.

The Roojai team

-

3 minutes ago, Nojohndoe said:

Roojai has responded appropriately in appreciation to your "heads up".

I have yet to receive my "official "policy but will be making a careful check on that detail regardless.

Dear Nojohndoe,

We are guessing you bought the Dhipaya product. We will send you a DM to ask your details to follow up with Dhipaya.

With the new product underwritten by KPI, we manage the entire process so we can assure speedy delivery.

-

- Popular Post

- Popular Post

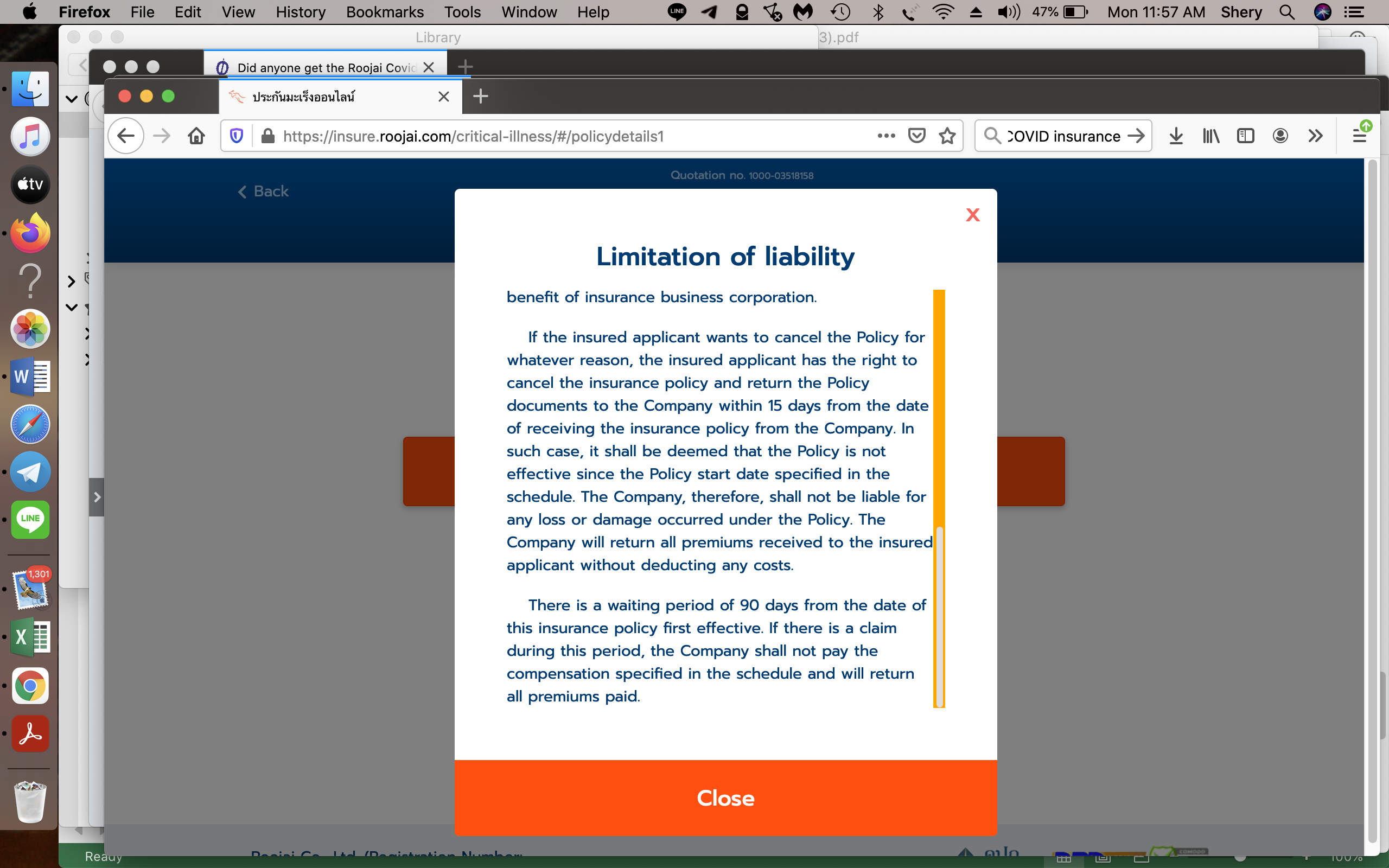

41 minutes ago, Sheryl said:It states this there but when you go through the application process online and get towards the end and click on Terms & Conditions it shows as I posted.

Hi Sheryl,

It's a website issue. The disclaimers are dynamic, based on the products and features selected. The 90-days waiting period should show only if cancer insurance is selected. We flagged it to the IT team to fix the error ASAP.

We can confirm that the waiting period for our covid insurance product is 14 days, as stated on the product page t&c and on the policy wording.

Apologies for the inconvenience and thanks again for flagging the issue.

Maybe we need to hire you for our QA(Quality Assurance) testing!

Regards,The Roojai team

-

3

-

2 hours ago, Sheryl said:

I attempted to buy online but policy seemed different than listed -- 90 day wait period.

???

Hi Sheryl,

Did you add cancer insurance, too? 90 days is the waiting period for cancer insurance and 14 days for Covid-19 insurance.

Regards,

The Roojai team -

3 minutes ago, Sheryl said:

Thank you. You might like to tell your staff this as calling your office to ask, they were unable to reply.

It's a new situation and many things are changing. We informed them after your feedback, and made sure they can respond to the customer's questions.

Thanks for your comment,

The Roojai team

-

2

-

-

On 4/24/2021 at 3:11 PM, Sheryl said:

Can you confirm if this policy will cover being sent to a field hospital or "hospitel" if one tests COVID policy? I called your office to ask and they did not know.

Hi Sheryl,

The customer will be covered in-patient when they are sent to a field hospital or Hospitel.

-

1

-

-

23 hours ago, bodga said:

Too late policy renewed elsewhere, your company wasted so much of my time, your representative the first time failed to give us a copy of the claim report in Bangkok, the second one in Hua Hin failed to show up at the dealership on time waited over an hour for them to finally arrive as agreed because a member of your staff didnt inform them of the meeting arranged 4 days previously despite me driving 40km to get to the dealership. and then wanted all the accident details again that id given your company in Bangkok already..

Dear bodga,

We will have to assume which is the case, but we are guessing it's the one we already discussed with your wife on Facebook.

The surveyor didn't gave your wife the claim document at the accident scene in Bangkok because the third-party already left the scene, and it wasn't possible to confirm that you were not at fault. Since your policy was purchased with a 5,000 THB excess, the surveyor suggested to get a police report for you to avoid paying the excess. The police report confirmed that you were not at fault and the claim handler called your wife to arrange a meeting to give you the document. Your wife requested to meet in Hua Hin and a location for the appointment was agreed. Unfortunately there seems to have been some miscommunication, and our staff and you were waiting at two different locations. We are sorry for the inconvenience.

Regarding the repair process timeline:- 12/11/2020 You drove to Ford Rungcharoen Bangkok to open the repair and on the same date we received the quotation from Ford Rungcharoen

- 13/11/2020 We approved the repair quotation and sent it back to Ford Rungcharoen- 25/11/2020 Ford Rungcharoen ordered 5 spare parts to Chevrolet Thailand

- 17/12/2020 All the parts were arrived Ford Rungcharoen. As you may be aware Chevrolet doesn't sale or manufacture in Thailand and searching for the parts may take longer than usual- 25/12/2020 Ford Rungcharoen notified you that the parts were arrived. You wanted to repair on 30/12/2020 but Ford said better to repair on 04/01/2021 because they were closed for New Year

- 04/01/2021 You drove the car for the bumper replacement and the repair should be done today or tomorrow.

We apologize if our service was not up to your expectations, but from this timeline it seems there was a miscommunication issue between your wife and our staff on the meeting for the documents delivery. The surveyor did everything correctly at the scene. He wanted to wait for the police report, for you to avoid paying the excess.

Regarding the long wait for the repair, we approved the repair one day after we received it. The problem is that Chevrolet doesn't manufacture in Thailand anymore. That's why many insurance companies stopped covering Chevrolet vehicles.

Apologies again and best wishes,

The Roojai.com team

-

1

-

-

19 hours ago, bodga said:

I insured both my chevvies with them then had an accident where someone drove into the back of me, they sent someone out to my condo to make a report, their agent didnt do soemthing correct so when I went to get it fixed at Hua Hin dealer they wanted to do the process all again, told em to eff off and wont insure with them again, they are the cheapest, they wasted so much of my time, accident happened 4 months ago and only tomorrow is FINALLY getting the work done, which is just a new bumper, a VERY simple job, they also give LOW maximum cover but you can increase it ie 550k total payout for total loss can be increased to 650k for a very small amount.

And YES they call and call and call and call, Wife told em to stop bluddy calling her.

Oh yes AND we have to pay the garage fixing it UP FRONT then claim it back off roojai...............krap

Dear bodga,

We will ask you privately for your insured name, to verify the case.

-

19 hours ago, samtab said:

I ❤️ Roojai !

But why this name ? ????

Thanks, samtab!

Roojai (รู้ใจ) in Thai means to know someone's mind/to know someone's needs ????

Roo(รู้)= to know

Jai (ใจ)= heart/mind

-

1

-

Roojai Insurance highly recommended

in Insurance in Thailand

Posted

Dear Scotsman,

We use Red Book for car valuations, which the most widely used car database in Asia. You can change the sum insured by requesting a call with one of our agents. There might some premium adjustments to your policy.

In our experience, less than 1% of all the car claims result in a total loss (full sum insured) of the vehicle. A much more important element to look at is actually the third-party liability, which covers for damages or injuries to third-party. These can result in very high costs at times.

Best regards,

The Roojai team