.png.3b3332cc2256ad0edbc2fe9404feeef0.png)

Gambles

-

Posts

710 -

Joined

-

Last visited

Content Type

Profiles

Forums

Downloads

Posts posted by Gambles

-

-

Thanks for taking the time to answer.

Glad I cleared that up by myself.

Actually onetwo, I should perhaps have also copied this (but actually it's sometimes better to do what you've done and figure the processes for yourself because that's always the best way to understand it) but here's a piece I put together in February -

The rate hike that never was…. by Paul Gambles & Stephen Tierney

The US Federal last month gained significant media mileage by hiking a virtually unused interest rate while keeping other rates at record lows. But to understand why there is something more sinister to this fiduciary sleight of hand than a simple desire to gain column inches, and to see how it could have a very real negative impact on export-dependent economies such as Thailand, one first needs to take a closer look at how the banking system works.

The modern banking system exploits fractional-reserve banking, meaning it only keeps a fraction of deposits in liquid reserves to maximise shareholder profits and depositor rates of interest. The remainder is lent out or otherwise put to work at higher interest rates than are paid to depositors. The difference, or spread, is how banking institutions make profits.

Fractional banking has dramatically increased credit supply over the past century. A fractional system that requires 10% of deposits to be held as reserves allows banks to initially lend $90 against every $100 of deposits held. The $90, once lent, goes into recipient bank accounts from where 90% can be lent out again. By the time 10 lending transactions have taken place the original $100 has created money in circulation of almost 7x the initial deposit.

This money multiplier has a major impact on economic growth rates, inflation, indebtedness and ultimately employment, prosperity and economic sustainability. Minimum reserve requirements set by central banks therefore have the combined effects of ensuring banks hold adequate reserves while also determining the magnitude of the money multiplier:

Banks generally hold reserves slightly above the statutory minimum requirement to cover daily cash flows and write-downs. But excessive withdrawals can result in a bank holding insufficient reserves while others consequently hold too much excess. Central banks typically oversee this by arranging ‘emergency’ funding, typically just overnight, while the bank implements actions to adjust its obligations and assets, such as raising additional funds by borrowing from money markets or calling in loans.

A systemic loss of confidence in 2008 caused banks to increase the rate at which they lent to each other. Following the Lehman Brothers’ collapse that September, interbank lending virtually stopped overnight.

Government responses to the crisis largely consisted of increasing guaranteed deposit amounts and ensuring that adequate liquidity was put in place.

In America, where the scale of problems was greatest, three main liquidity boosts were implemented: the Troubled Asset Relief Programme (TARP) injected a staggering $600 billion into the banking/finance sector within a matter of months; the Term Asset-backed securities Loan Facility (TALF) which allowed distressed assets, including defaulting residential mortgage backed securities, to be transferred from bank balance sheets to the Fed’s; and cutting the cost of emergency funding from 1.25% in October 2008 to 0.5% from December 2008 to this February.

The need to allay fears of banking system failure created an additional $435 billion of money supply, raising concerns of hyperinflation if the money made its way to Main Street.

To counter this concern, the Federal Reserve Act 1913 was amended to allow the Fed to pay banks interest on excess reserves deposited with it, allowing banks to profit from the Fed on funds that they had actually borrowed from it – the equivalent of your bank lending you money at 0.5% provided you deposited it back with them at 1.5%.

Effectively all American banks were in this situation in autumn 2008.

This unpublicised policy has two significant catches. Stimulus funds paid for by the US taxpayer were supposed to stimulate the economy, but instead of being circulated in the real economy where they could boost consumption and restore confidence – and you cannot have a recovery without confidence — banks were paid more interest to keep the funds in their vaults.

Imagine what a real surge in US consumption could mean for economies such as Thailand where exports account for about 65% of gross domestic product and 80% to 90% of locally produced electronic and electrical goods are sold abroad.

It gets better.

To allow unfettered remuneration to be paid, banks repaid these borrowings as quickly as possible, with TARP debt falling from $612 billion to $317 billion.

Simultaneously, borrowings through the traditional discount window plunged from a peak of $44 billion in 2008 to $14 billion currently. The Feb 18 interest rate hike 0.5% to 0.75% applies only to borrowings through that discount window, making it meaningless in real terms.

It has been suggested that the hike implies the worst economic conditions are over and that the Fed is prudently increasing rates to ward off inflation. But the impact of this move potentially goes beyond mere PR and financial spin.

Creating false hope in a global financial system that is largely based on sentiment is a dangerous game, and the policy of paying banks interest on excess reserves is so radical and untested that no one can be certain of how this policy is impacting the US economy now or what the future effect of reversing it would be.

Strange things are afoot in the ‘the land of the free (money)’ and things are definitely not what they seem. Has anyone seen the emperor’s, sorry Ben Bernanke’s new suit?

-

Now, although the fractional reserve banking effectively means that banks can create say up to a multiple of 10 times the deposit base, this does not happen in one fell bang. it is a reiterative process, the very first customer strolls into the bank and dumps 100 Baht on the counter, everybody shouts "whooppee!" and then the bank can lend out 90 Baht to customer B, who then spends it on stuff at customer C's shop. Customer C then deposits this 90 back in the bank and the bank can lend out 90% of this, ie 81 Baht, to D. And so on until the bank has lent out 1,000 Baht or 10,000 if they have been naughty.

But, what happens if the bank invests the 90 Baht deposit of customer C in a government bond? Surely that would stop the fractional reserve thingy in its tracks, because the cash has gone off to Tim, or, what's the name of that schoolboy, ahh, yes, Osborne. STOP! The light dawns and I can see this makes no difference whatsoever, because Osborne will have squandered the cash on some frivolity, such a new garden gnome for number 11, and the money heads off through the garden gnome seller back into the Magical Mystery Banking Machine, just ready to be fractionally exploded into even more debt.

Glad I cleared that up by myself.

Well done, one, two!

However, lending money via any triple A mechanism doesn't really count as lending money in a fractional reserve sense because the asset is such strong collateral that it doesn't require reserves, be it Greek, or Spanish debt (until recently), sub-prime mortgages, or anything else sliced, diced and lucky enough to receive the highest rating from the agencies

-

Oh no! It's another of those panic mode buy gold yesterday, the USD is about to become worthless overnight, hyperinflation will strike TONIGHT whilst you are asleep and tomorrow a loaf of bread will cost 6 trillion Dollars and an ounce of heavy yellow metal will cost a pile of Greenbacks which would require supplemental oxygen to count and cause a major hazard to international flights.

LOL - I think I've published more than a few of those myself!

But nowhere do I see a mechanism that would create hyperinflation. In countries where it has occurred there has been huge external debt in foreign currencies, with nobody wanting to hold the sovereign currency. This is what would be interesting if, for example, there was a decision to put Greece back onto the Drachma. Something which is, IMO, not easy. There is a bit of banter about it, but, in the second it looks serious, there would not be a single Euro left in the banks, because everyone would know that a return to the Drachma would mean a currency devaluation and inflation in terms of Drachmas. The Greeks would have to introduce strict price and currency controls to prevent prices racing upwards.

But back to the USD. Unless Bernanke does something incredible, like dropping a million into everybody's bank account, the Austerity Challenge 2010 seems to be taking hold. Debt is being paid off, cut backs are being made, and new productive jobs are not being created. All this means that there is less cash being spent on stuff and is more deflationary than hyperinflationary. The hyperinflationists seem to base their argument on the huge amount of QE, which they assume will, at some point tonight, find its way into the average Joe's pocket and all the Joe's and Jane's will collectively go out on a spending binge. But I believe most of that QE has been spent buying up Tim's UST's, which are propping up the banks' balance sheets, so it can't be relent anyway, leaving Ben with a load of rubbish on his balance sheet, which presumably he will want to sell of at some point, and that is also a chunk of deflation in the background, although I expect Ben will pick the moment and sell into any signs of another bubble, effectively subduing it, another reason why I can't see hyperinflation coming along tonight.

Spot on - for now

The Feds have clearly stated that they believe that they can control the flow of money - if they're right then we would have a period of re-adjustment with a long period of sustained but moderately high inflation to inflate away the debt burden.

I just don't think that things are so easy. The deflationary pressures are huge in the indebted western economies right now (although inflation is emerging in the surplus economies and Western deflation doesn't export to the East nearly as readily as Chinese deflation did to the west) and the problem is that there is so much of a reality gap on western balance sheets that controlling this is nigh on impossible - it's like a downpour on a parched field - the water just gets soaked up but eventually the field starts to flood. If the rain keeps coming then every extra drop that falls after that point is just pure floodwater. Do we trust the Feds and The Treasury to get it right? I don't.

At some point brutal deflation could quickly switch to hyperinflation but you're right - it won't be tonight and it's a 'could be' not a definite.

-

I have always had obsession with demographics and economies - in that I think that demographics essentially explain at least 50% of economic activity over the medium term. For instance Japan's two decades of lost growth is most easily explained by demographics.

There is a good blog about this.

Super-Economy: Japan's problem is supply, not demand (updated)

By a swedish blogster.

The salient points being....

The importance of the demographic transformation in Japan is even more clear if we include the entire 1990-2007 period.

In non-population adjusted figures, Japan's real GDP grew by 26% in total these years, the lowest in the OECD. In comparison the figures are 63% for the U.S and 44% for the EU.15.

But during this period the U.S saw it's potential labor force (the number of people between 15-65) increase by 23% and the EU.15 by 11%, while Japan had a decrease of 4%.

Between 1990-2007, GDP per working age adult increased by 31.8% in the United States, by 29.6% in EU.15 and by 31.0% in Japan. The figures are nearly identical!

Japan has simply not been growing slower than other advanced countries once we adjust for demographic change.

Actually the EU growth rate is understated in his figures because the inclusion of Germany (whereby the inclusion of E.Germany ranks it so low is something of an aberration.)

Anyway the point is this. Europe and the USA are going Japanese in demographic terms. And when I say 'going Japanese', I mean going Japanese squared in a lot of cases. In other words, Japan's economy has done fine but it has seemed a nightmare because the working population actually fell - by 4% - over 18 years.

Then you can do some back of the fag packed projections going forward and estimate that...

To the year 2050 on an optimistic scenario...

Europe's real growth rate will be 0.5% p.a.

And the USA's growth rate will average 1.7% p.a.

I call this optimistic because I assume the same real per annum GDP growth rate of the last 20 years per worker (namely 30%) combined with the UN demographic stats. Japan's economy has not been great with a 4% decline in working population - you cant expect much out of Europe with a 25% decline.

And the reason this is optimistic is there has been an enormous increase in leverage across the board over the last 20 years which is essentially spending today what you earn tomorrow. What would have been the US or UK's growth rate without the stimulus, how much has growth in the short term been boosted by mortgage equity withdrawals and the decline in savings rates.

I doubt economies will deleverage but they simply cant get a huge boost from increasing leverage. So throwing away the fag packet as being too sophisticated and simply making the assumption that increased leverage boosted growth by about 1.2% p.a. between 1990-2010 I can assume zero real growth per worker going forward and come up with a pessimistic forecast that...

EU growth will average -0.6% real over the next 40 years

While the US will grow real at about 0.4% p.a.

And in reality things could turn out worse. You see you can essentially increase debt forever without increasing leverage, so long as you assume growth in 'nominal' GDP. But it is a non-linear reality if growth is lower, your ability to accumulate debt is lower or negative which reduces your GDP. For instance the EU's 3% deficit limit is based on a growth assumption.

Demographics is both extremely important and also very misunderstood (at least by me) - but big picture trends tend to be unopposable

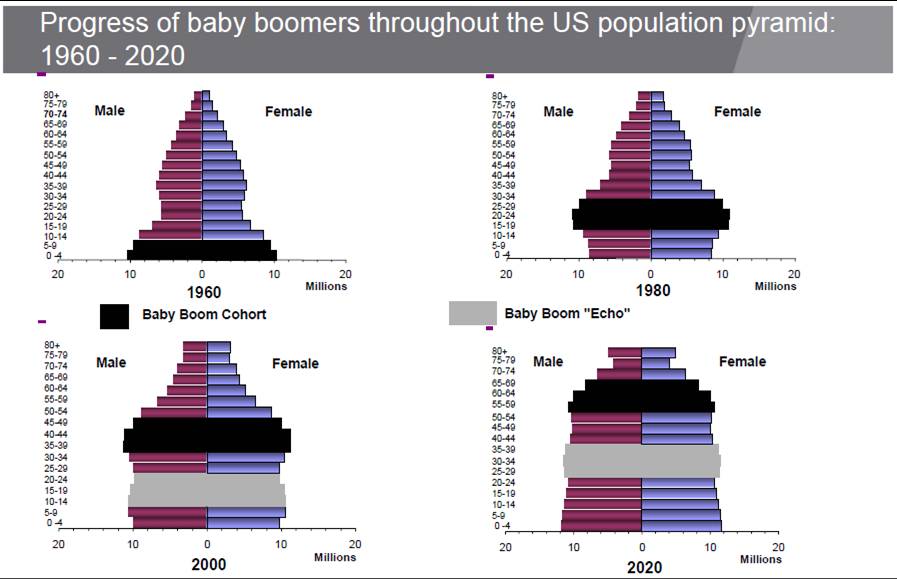

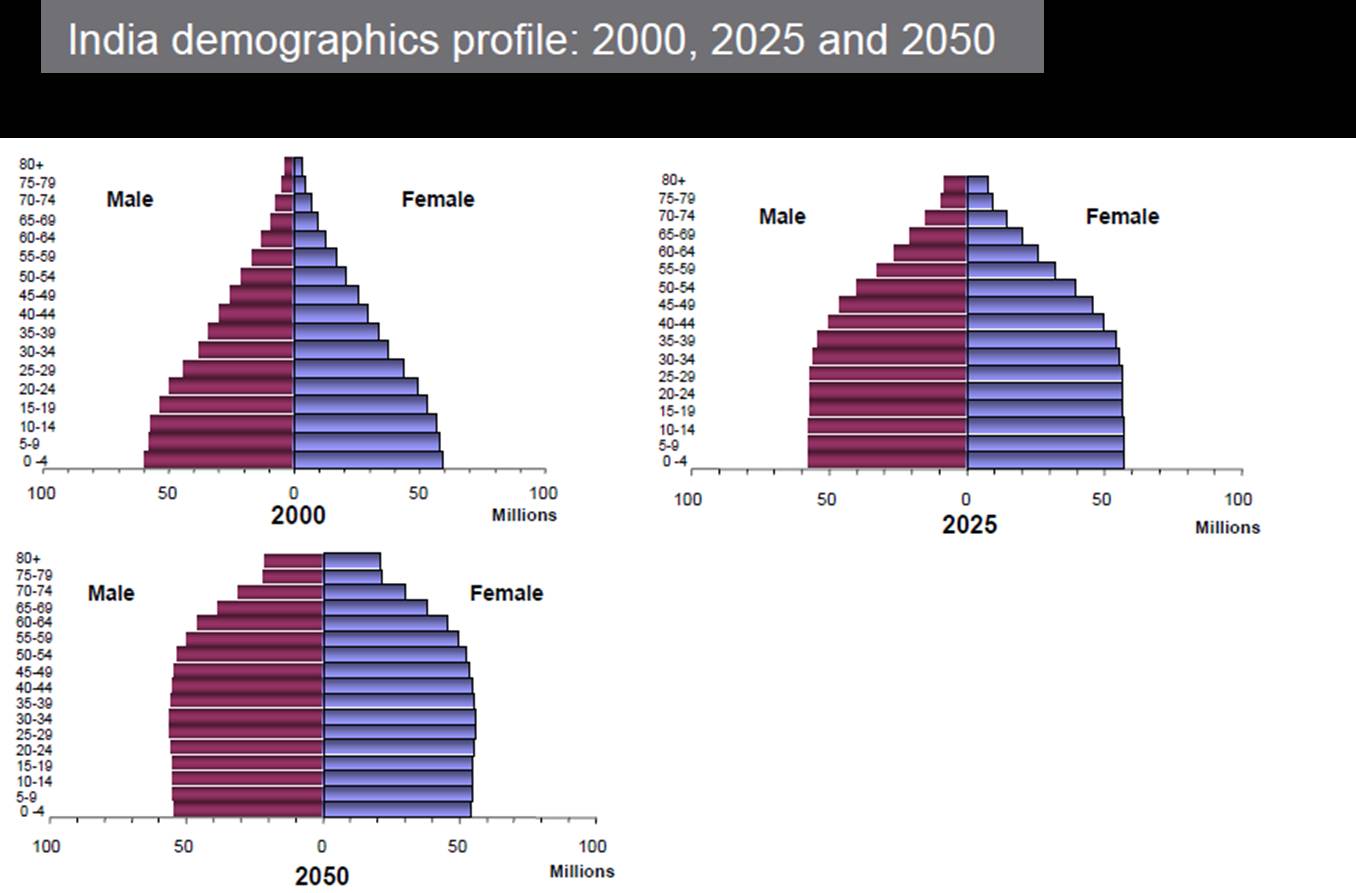

Shame that you missed Scott Campbell's recent Bangkok visit - he picked up the demographic theme -

Unfortunately I'm not very good at uploading graphics but basically US population from 1960-2020 (depicted at 20 year intervals) is from baby boom to elderly population

whereas Asia (depicted by India 2000/2025/2050) is poised to experience its own baby boom - yet another confirmation that this is Asia's century!

-

Funny money has been a political tool forever,

The Romans had precious metals as their currency and do you know the term "debase"? The Roman politicians had the brilliant idea that if a coin was 100% pure precious metal, they could slip a little base metal in and, over a couple of hundred years, they went from 100% pure precious metal to almost 0%. That's where the term "debase" comes from

Having said that some think gold is the solution.

Quotes, Investors and speculators have good reasons to turn to gold in the midst of unorthodox monetary policies and high fiscal deficits. As long as low interest rates and high volatility persist, the markets will expect the curse of inflation - and the continuing high gold price is the sure result. - Hossein Askari and Noureddine Krichene The world's economic expansion since Franklin D Roosevelt took the United States off gold in 1933 does not make it impossible for the world - or an individual country - to return to the gold standard. Just as honesty is practicable and constitutions should be followed, a return to the gold standard is both possible and necessary. - Antal E Fekete

Iwould like to note that the Thai seem to understand the value of gold better than most.

nice quotes but utter tosh really; fiscal indiscipline is the problem (since the start of the last century, by 1933 the gold standard was already dead and buried in most major economies) - I don't think that anyone has proposed a viable or serious modern gold-based solution to the problem. In terms of global monetary policy, it's a relic of a former age. That said its role as a store of value at an individual level is currently reemergent which is why we'd see gold running to at least $ 2000 per oz but a return to the gold standard is both impossible and a distraction from the need to create a modern solution to the economic problems that the indiscipline has caused and which still lie not very deep beneath the surface...

-

Funny money has been a political tool forever,

The Romans had precious metals as their currency and do you know the term "debase"? The Roman politicians had the brilliant idea that if a coin was 100% pure precious metal, they could slip a little base metal in and, over a couple of hundred years, they went from 100% pure precious metal to almost 0%. That's where the term "debase" comes from

true....and if we're getting all etymological then there's always clip joint - where primarily gold and silver coins were trimmed and clipped. Additional tangential apparent pertinence to this disucssion stemming from the fact that if I recall correctly in 13th century England this crime was seemingly primarily practised by Jews who were initially executed in large numbers for this capital offence and then ultimately banished en masse from the Kingdom (the mediaeval Exodus) although it was widely believed at the time that this was a very convenient way for the crown to default/restructure/obtain forgiveness on its heavy indebtedness to Jewish lenders...but, of course, that was just 13th century England.....

-

What would stop BP from just plugging the leak and getting out of the US ? It seems like nobody in the US is talking any sense. They are just making endless claims that will guarantee a bankruptcy.

They could just sell all their reserves in the area, pack up and leave and not answer the phone. What could anyone in the US do ?

What would stop them plugging the leak? Just the fact that they cannot

If they could they would have one less problem. Yes they can try & duck out on their responsibilities same as anyone including Haliburton.

What could the US do? What could the world do ? This leak is affecting the US today..None know who it may effect tomorrow.

PS: Seems today BP has in fact decided to defer their dividends to share holders decision till July. Now that I think may be a dumb move as that may drive their stock down quite a bit faster.

Also think it was wrong for the US Prez to pressure them in that direction of no dividends as he also implies by that action that they are short...Which can only increase a lack of faith

POTUS dictating BP's dividend policy

I smell international interference, protectionism, NIMBYism, currency speculation and the rise of every-man-for-himself international tensions.....

-

Duplicate post deleted

-

edit: Forgot to advise the currency whingers. It's scientifically proven that a currency's strength is directly proportional to it's participants' mastubatory behaviours. Thais have been masturbating well, hence the strength in the THB. Brits and members of the Euro have not been masturbating enough, clearly. Increase masturbation and soon enough you can get to 75THB per GBP. Then you can move on from the wet dream and come to Thailand where those GBPs will pay for somebody else to masturbate you. Rinse, repeat. It's scientific fact. I promise, as I read it on the internet.

Sounds like something Naam would post. But that's just an observation, nothing more...

In the odd moments when my overworked cranium starts wondering about stuff, I sometimes come across questions that I do not know the answer to. Well, in fact, quite often. Mostly with a bit of effort and the internet I can find an answer. But today I was meandering around and have a couple of questions that maybe somebody around here can shed some light onto?

1. When I transfer Squibs across to Thailand, say GBP 1,000 then these appear in my account at the SCB as THB 40,000 if I am lucky. Now how is this all balanced out? The GBP 1,000 disappears out of the UK with a flooop, whooshes down some electronic channel with a fizzzz and then PLOP in go the THB's at the SCB. So the UK is minus 1,000 eQuids and Thailand has conjured up 40,000 eBahts in my account. So what happened to the eGBP's? Have they simply fizzled out of existence? Surely there must be some means of balancing out the eGBP's and the eTHB's across nations? Are there are whole bunch of eCurrency accounts at the BoT which then head off to the BIS in Basel?

2. What was the second question? <deleted>, gone straight out of my head. No matter, we are still resourceful and the beer level has not reached to the eyebrows yet. So, the USD is the reserve currency. The closest competitor, the EUR, seems for now to be well out of favour. And the Squib? Well, after Brown's term in power it looks like the Squib is going to compete with the EUR in round after round of mutual devaluations.

As an aside I wonder what those other guys in Basel, the IMF crowd, will do to the SDR basket this year. The Chinese want to have the Yuan included, but if the Yuan is simply a proxy for the the USD, then maybe they should just kick out the GBP, JPY and EUR and have 1 SDR=1 USD? Might lessen the confusion. But anyway, whether the SDR is really worth discussing I don't know. Maybe it's just another of those academic concepts that enables a bunch of guys to feel important and earn massive salaries and have lots of free trips, or rather expense remunerated tax payer paid trips.

Where was I going? Right, there is some considerable talk about the USD tanking. I do not understand how this could happen. Mr Triffin has already stated the case, so how could the US single sidedly devalue? The world's trade is conducted in USD's, the majority of the World's currencies are pegged to it in some way or another. Surely the USD is the baseline? Try and change it and everything moves in step, so the status quo remains. And, in spite of Timmy rushing around asking the Chinese to let the Yuan appreciate, maybe the current situation is just hunky dory for the Great US of A? With the assistance of the rating agencies and the actions of GS&Co the EUR has been demoted, so the US has surely secured buyers for its UST's for the next few years? Which, in the midst of this crisis, when all Western countries are trying to compete for funding, is surely the goal?

3. Ah yes, back to the original question 2. Now when the French and German banks lend money to the profligate southerners by buying worthless government bonds, are they able to fractionally reserve these loans or must they have the readies on hand and in the vaults? So it is real money that is being used and not thin air type stuff?

1. I've never actually studied this so this is totally off the cuff/off the record and involves a great deal of hearsay; it could be complete tosh and hopefully there are technical experts out there who actually do know a great deal more about this and can confirm or deny - I recently found myself doing a presentation to a room of people about the Baht including an analysis of BoT handling of the '97 crisis and it turned out that one of the audience was a former leading BoT banker from that period - luckily he confirmed that what I was saying was actually correct and potential embarrassment was avoided!

I believe that there is an historic arrangement whereby supposedly BBL operate a mass clearing and settlement facility for all inbound outbound transfers - it would I guess make make sense that there is some kind of gateway because Baht isn't anything like freely convertible and there are limits to the extent of offshore Baht holdings by commercial banks and the Bot Would have to have some process for regulating this. So sending GBP means that at the gateway point the notional conversion takes place and the sterilisation process means that when settlements are completed the BoT ends up absorbing net surpluses onto its own account in its own preferred currency allocations. This would allow the relative illiquidity of Baht to be managed. It also would help to explain why inbound/outbound electronic transfers to/from Thailand are so slow.

2. The history of SDRs is interesting - basically manufactured IMF liquidity that had to be somehow denominated and obviously with the economic effects of 2 world wars weighing heavily on Europe, Dollar had become the primary global currency in the period since 1944. One interesting historic aside (I'll do a piece on this sometime) is that China didn't suffer recession/depression during the 1920s/30s because it was happy to depress the value of its currency (via the silver standard). This may be completely meaningless today but my experience is that Chinese economist are generally much better at knowing and understanding their history than some of their western counterparts.....

3. Bank loans are a part of the liquidity creation process - banks' liabilities that are a multiple of their assets (or as you say whose reserves are a fraction of their loans) are creating liquidity almost from thin air. That is as true for the French and German banks who lend to GIPSIs as it is for domestic mortgage lenders etc - possibly even more so depending on the categorization of these loans - sovereign loans presumably requiring far lower capital set-aside than consumer loans in most jurisdictions.

Don't forget also that AAA sovereign debt is an acceptable balance sheet asset equivalent to cash so, for instance, a couple of years ago a pre-bankrupt GIPSI walks into a German bank that has Eur 275 Mn cash sitting in the vaults and says "I need Eur 275 Million please"..German bank transfers Eur 275 Mn cash and ends up with say Eur 25 Mn of Greek bonds and a Eur 250 Mn term loan on its balance sheet...it then funds the Eur 250 Mn through the markets and it now has that 250 Mn sitting in the vaults to repeat the process with.........One story doing the rounds is that there are German banks who now find themselves over 100X leveraged...bearing in mind their expsoures to GIPSIs and also that I don't believe that German banks have ever properly written down their exposures to US sub-prime, I'd be very nervous about any European banking expsoure right now.If things move quickly against them do we have faith that the EU could quickly rally round to save its banks the way that the Fed/Treasury did? Maybe, unlike America, Europe will be saved from itself by its own bureaucracy?

-

The clock is ticking, western economies with crash along with there money, its just a matter of time. Europe in bankrupt and so is the US. The US has been bankrupt since the civil war and then again in 1932. Enjoy your funny money while it lasts.

From memory, US repaid its entire national debt on more than on occasion in the 19th century including post civil war. Its sovereign finances were actually strong until the creation of The Fed.......it's been a roller-coaster ride ever since. Not that I'm claiming 100% causality between those facts.....

-

Though I'm not a Zionist, I'm not a jew hater like you seem to be. I'm aware of the victimhood ploy and how it has been used by just about every interest group at one time or another. The day the US sinks so low as to invoke the "victim card", will be the day I revoke my citizenship. Hey, speaking of Jews, Arabs, money and bought politicians and national security interests, why do you think Citigroup got such a sweet bailout package? That's all I have to say on this matter.

That is not fair Lanna !

I have never used the word hate and this is nowhere near the same as perpetually expressing my frustration that

a lot of innocent people are suffering because of a small group of people - and yes as well as Gaza i include

the bankers who own the Fed that have caused so much misery in USA as well.

i have the right to question and shout enough is enough !

See now that is a very good example of this.........LB I respect your posts & you seem very level headed... Yet why would you call Midas basically a Jew Hater?

I grew up in a real melting pot of an area & never knew racial problems.

In fact while growing up when we were already teens is the first time we actually heard a black slur & had to ask my dad what it was.

Why cant Midas be upset with something that is obviously lopsided/ wrong in his opinion? How does that make him a Jew Hater?

Is anyone who views Palestine in teh wrong automatically some other religion hater?

Why does Jew hater enter any conversation about the transgressions of the country Israel?

I really dont get that at all.

Wrong is wrong regardless of race/color/religion

Thanks flying. As a huge animal lover, I don't hate any living being.

What I do hate is injustice and cruelty.

Like you I greatly respect Lanna and his postings – particularly the less obvious articles he provided in the early part of this thread.

And you are right- this response is a " case in point " as to how simple questions ( it doesn't even have to be an argument !

) are turned into something else ? And it ALWAYS happens to me when I raise the question of ownership of THE FED !! Because of this I have been convinced for a long time that if we keep firing enough of these questions which do have a " common thread " – we would ultimately discover the "Mother lode " of information that would answer many of our questions

regarding the real cause of this Financial Crisis.

The minute that people, for whatever reason, cease to speak out against injustice and cruelty then we're finished as a race.

It's a very emotive topic and personally I feel the attitude that if you're not 100% for me then you're against me seems to be a dominant factor in deep-rooted conflicts like the Middle East and until/unless we find a way to get away from that then I think that it becomes much harder to achieve any kind of peaceful reconciliation. Wrong is indeed wrong and I believe that Midas was rightly motivated purely by a sense of injustice and was not simply using that as an excuse to couch justifications - I don't actually detect any hatred whatsoever in his postings.

-

The cost of the clean up has been estimated at between 10 and 20 Billion Pounds.

BP's market value has dropped by 50 Billion

It's starting to look a bit oversold and maybe worth a punt, but it could be a long time before the price recovers. The US government wants to force BP to cease dividend payments and with all the other hysterical rantings, who knows how much lower it can go.

BP's price now depends on so many imponderables that are more political than financial that it remains impossible to attempt to define value. Speculators may look and decide that the risk (further falls extending to the entire value of BP if it's out out of business and there is no residual equity left on the closure of the business) is outweighted by whatever the upside is from here.

I suspect that there are smarter ways to play the opportunity though based on the fact that market assumptions may be flawed - option pricing could well be making false assumptions about the stochastic volatility of BP's price -

1) I see that the structured product providers are rushing out BP-based products. The retail ones that I've seen so far are wildly over simplified but I believe that it's possible to exploit these to generate a premium today for taking a 12 month position that sees you 100% positively exposed to share price movement of -20%to+15% from today's pricing neutral on falls of 20%+ and 15-30% and leaving yourself -100% exposed on gains of 30% plus. If you felt confortable that you could trigger-buy into a rising BP in a way that mitigates the cost of that risk and assuming that BP pay some dividends, this would appear to be free money but it then hinges on BP vol in that +15to+30% range over the next 12 months

2) You could buy a basket of stocks of the participants in the well problem - it's not just BP that have been marked down so badly - but will the blame be shared equally - will BP/Transocean/Halliburton take an equal caning here - if so is 50% excessive? or will the blame largely devolve to BP in which case the others are the buy here? buy an equal basket of the related stocks and as long as the final outcome is overall positive for the basket, you're doing OK

3) The entire sector seems to be suffering (not to the extent of the participants admittedly) but is it reasonable to have a 25% markdown in the price of oil service companies that have no exposure to this situation?

There's an opportunity here for sure - it's too speculative for my taste and I'm happy to not participate as for my requirements the risks here outweight the upsides. As I pointed out sarcastically to Sokal a few days and several dozens of points of price action ago, I think that you need something more scientific than a previous pricing chart to define BP's value right now.

-

As recently promised, the latest thoughts of the excellent Tim Price (repoduced with the author's permission) - interesting that he quotes from Lords of Finance; with the Sovereign crisis coming up, there'll be a series of MBMG Updates over the summer months about that extremely illuminating publication. Enjoy...

7th June 2010 Not inspirational

“The announcement of the rescue package failed to stabilize the situation, perhaps because more people knew how deep the problems went than the government realized.. None of the central bankers had faced an international financial crisis before; they therefore had to make things up as they went along.”

- From „Lords of Finance: 1929, the Great Depression, and the bankers who broke the world‟ by Liaquat Ahamed (Windmill Books, 2010).

Communiqués from government conferences tend to recall the words of Ralph Waldo Emerson:

“The louder he talked of his honour, the faster we counted our spoons.”

The latest official statement from the G-20 in Busan, South Korea, does not disappoint fans of irony expressed on a magnificent scale. Among the highlights from this vapid exercise in giving voice to messianic delusions of relevance, international finance ministers and central bank governors agreed to:

“firmly secure the global recovery”;

“put in place credible, growth-friendly measures..”

rather wonderfully, ensure that “Monetary policy will continue to be appropriate to achieve price stability” and “reduce moral hazard associated with systemically important financial institutions”;

hysterically, to “accelerate the implementation of strong measures to improve transparency, regulation and supervision of hedge funds, credit rating agencies, compensation practices and OTC derivatives in an internationally consistent and non-discriminatory way” [emphasis ours].

There was no commitment to deliver world peace or universal wealth and health, but that may just have been an oversight. The problem with these sorts of statements was well expressed in a letter to the editor of the Financial Times last week from a Mr Nigel Collin, referring to a piece, “solutions for a crisis in its sovereign stage”, written by Nouriel Roubini and Arnab Das. While acknowledging that the original article was “both illuminating and practical”, Mr Collin went on to point out that

“.. a closer examination reveals that the verb “must” is used in three of the five solutions advocated. Without an explanation of how a sovereign state must be compelled to adopt a solution, the solutions are rendered aspirational rather than inspirational.”

Where to begin with the G-20‟s marvellous aspirational announcement ? One does not necessarily expect politicians to declare their own redundancy, but wealth creation and, in a more general sense, “recovery” are the products of private action rather than government direction. Governments take capital from their own people but they are functionally incapable of producing it. The best thing for government to do would be to get out of the way. Instead we have governments that have squandered billions in private capital (not just current billions but claims against future billions from taxpayers not even born) in supporting fundamentally bad banks. A free market has a magically effective way of discriminating between good and bad businesses. Bad businesses fail and are purged from the system and good businesses prosper, begetting more wealth in the process. Not content with their malign achievements to date, governments have now tasked the banks with mutually contradictory objectives: strengthening their balance sheets whilst simultaneously maintaining the provision of credit to the broader economy. You cannot drive a car well by concurrently slamming on both the brake and the accelerator.

There is a similar contradiction in the pursuit of credible attempts to bring sovereign finances back toward balance. In part it constitutes what economists call the fallacy of composition and the paradox of thrift. What may make sense for individual governments to do (turn off the spending taps) could be hugely detrimental for the broader international community. Politicians may not acknowledge the fact, but the world is even more closely interlinked than it was in the crisis of the 1930s, and the economic and financial interactions are undoubtedly faster. What is certain is that beyond a certain point, which Greece has now probably reached, slamming on the fiscal brakes transforms a heavily indebted government from muddle-through financing into insolvency, as the ailing economy, bereft of government spending to which it has become addicted, is unable to provide even sufficient tax revenues to allow that government to service its debts. Default follows.

While it is clear that just as in the 1930s, today‟s politicians and central bankers, having no route map, are making it up as they go along, it is equally apparent to any objective observer that there is precious little of the coordination to which the G-20 communiqué so pompously aspires. Recent policy announcements do not augur well. The German Chancellor unilaterally declares a jihad against speculators in her now infamous tirade promising to beat the markets. The Australians break ranks and run the risk of killing the golden goose by unilaterally hiking taxes on the mining sector. Since world currencies are not, as they were in the 1930s, backed by the solidity and stability of gold, everyone seeks solace in currency devaluation. But by definition not every currency can depreciate against its peers. The balance of probabilities is that as this long emergency continues, the depth and breadth of the US dollar pool wins out against most of the rest of the world‟s paper money, despite its own underlying fiscal precariousness.

The G-20‟s reference to regulation in a consistent and non-discriminatory way is a triumph of absurdity and bare-faced contradiction. How else to describe a regime in which badly run banks are extended indefinite and unlimited financial support, while institutional investors not fortunate enough to be deposit-takers are targeted for daring to point out the nudity of the Emperor ? And this last point gets to the real challenge for investors today. Navigating markets fundamentally distorted by government manipulation, wholesale currency debauchery and fiscal incontinence is bad enough, but we are now tasked with trying to anticipate seemingly random and often unilateral political action.

Some of the rational investor‟s strategy response should by now be obvious. Avoid the debt and currency markets of the most egregiously undisciplined administrations. Buy precious metals as the ultimate in portfolio and currency insurance – their upside potential in price terms is widely understated and misunderstood. In other respects, exposure to equity markets should reflect individual risk appetite and any requirement for albeit irregular income rather than a slavish allegiance to an always volatile asset class.

The G-20 communiqué suggests that recovery is on its way, though characteristically it cites no evidence for the declaration. The evidence from, even by recent standards, unusually nervous financial markets would suggest otherwise.

Tim Price

-

QUOTE (Gambles @ 2010-06-05 18:21:51) QUOTE (Naam @ 2010-06-04 08:13:34) QUOTE (Gambles @ 2010-06-04 07:16:00) So the recent happenings in Gaza may or may not be a colossal global political, economic or societal event but we won't know that just yet and undoubtedly they're significant in their own right anyway.

in a couple of months hardly anybody will remember or talk about it. on that claim i bet my [not so] sweet àss

OK, I stand corrected - nobody except Naam knows.....

the list of much more severe atrocities is long. who (besides al-Jazeera) talks about e.g. the "War on Gaza"? by the way, it is my understanding that a "claim" does not denote "knowledge". native english speakers please correct me if i am wrong.

Fair point, Naam

In the interests of terminologoical exactitude, what I should have said is that nobody knows for certain but Naam feels sufficiently confident of his claims to wager the substantial value of his somewhat acrid backside on them....

-

Ok, so I was wrong

The RBA held interest rates on Tuesday. Some analysts thought the dollar would shit itself if the RBA announced a hold.

So far so good and look at the bright side...I'd rather be drawing Aussie $ than UK Pounds

that's a bit like saying I'd rather be dying than dead!

Today I'd rather have US$ than either...looking forwards I'd rather have Asian currency

-

The story with the Euro is that like many high fliers it just wanted to go up without building support. That breakout in 2002 really should have been retested sooner rather than later. Gold same story of course, but it is the bubble dejour so it could run a bit more before it comes all the way back. Euro currently showing positive divergances in IT time frame while Gold showing negative.

I just dont see gold as a bubble. I am not saying that because I hold some either.

It does not exhibit bubble qualities...You do not hear taxi drivers & everyone in between talking gold.

You do not hear everyday folks saying ...I have to get some gold before TSHTF

In fact remember that deal where a guy tries to sell a gold coin to the public? It is similar....Non interest for the most part.

What we see is gold no longer acting like a commodity but instead acting like a traded currency/monetary instrument.

As for building support & destined to go all the way back.....

I have an interest in charts & cycles but I also tend to think some things like economic catastrophe is not limited by patterns nor destined to follow previous *pictures*

That said I would not be surprised to see the common low June come in

I do not think the Euro failed for that same reason....Instead the Euro was an experiment. It failed...How could it not?

It can never be equally supported & why should the strong carry the weak/lazy/non contributors?

how bubble behaves in a liquidity shortage remains unanswered

Personally I like gold and hold gold and expect it to go up

but I also think it could fall significantly before it does, which is when I would buy more....

-

So the recent happenings in Gaza may or may not be a colossal global political, economic or societal event but we won't know that just yet and undoubtedly they're significant in their own right anyway.

in a couple of months hardly anybody will remember or talk about it. on that claim i bet my [not so] sweet àss

OK, I stand corrected - nobody except Naam knows.....

-

Still Israel, Gaza etc. is an exceedingly boring topic and I am sure has nothing to do with the 'Financial Crisis' - well until such time as they decide to nuke someone.

If oil were to hit $300 a barrel that would have a lot to do with the 'Financial Crisis' and the fat lady is still clearing her throat

Israel Worried Turkey May Send Navy Ships With Next Flotilla

http://www.huliq.com/1/93847/israel-worrie...s-next-flotilla

Well fair point.

But given a massive oil spill near the Mississippi, that drillers have been told to stop drilling, that Israel is playing politics and the price of oil has gone absolutely nowhere - we should assume that Israel, Gaza etc is an exceedingly boring topic that has next to no impact on the oil price or the Financial Crisis - rather than it is fundamental to the underlying global economy.

I would perfectly accept that if the oil price had risen US$30/bbl we should be glued to the possible outcome but that doesnt really seem to be the case.

I thought you used to be an analyst Abrak and I thought analysts were forward looking ?

A number of factors could be keeping oil prices down right now . Maybe it just highlights a supply glut in the open market and a strengthening American dollar is maybe putting downward pressure on all commodity prices not just oil?

But surely you can't seriously compare this to the " psychology " of what would happen in the oil market if the fireworks started in the Middle East and as some suspect Iran could get involved ?. It is a world apart from an oil spill in Mississippi to having the potential for the bulk of world oil supplies seriously interrupted? Forr that reason I don't consider Israel, Gaza etc to be an exceedingly boring topic at all and on the contrary I think it highlights what could make the Crisis even worse. ( of course I do remember you said not so long ago " what financial crisis "

) ?The events in Gaza are anything but boring and may have a global financial impact (I still think that rightly or wrongly a lot of things will be brushed under that uge bulging carpet where they have been before in the interests of trying to maintain a Middle East peace at almost any price). To me there are 2 key aspects:

1) This is an issue where in the absence of facts, the effect of any comments tends to be polarisation based on existing beliefs and prejudices. I don't know enough facts. I can't think of anything insightful to say so best I don't say anything - but that makes me even more determined that I really would like to know everything that there is to know about this major event

2) With many major occurences in history, they don't always have an obvious root cause; people react about all sorts of things that in isolation rationally shouldn't cause the consequences that they do. Whatever may have pushed the Cumbrian taxi driver over the edge was almost certainly of itself no real cause for the awful chain of events that occurred there on Wednesday BUT people aren't rational and have breaking points - even if viewed from outside the breaking point may seem to be very trivial.

So the recent happenings in Gaza may or may not be a colossal global political, economic or societal event but we won't know that just yet and undoubtedly they're significant in their own right anyway.

-

Perhaps Im not paranoid enough?

Been an Economist subscriber for years. I do have a soft spot for British tory papers though

I stopped my Economist subscription when I realized that I could write much better articles about Thailand myself and that Asia Times, FEER etc wrote much, muc, much better articles about Thailand. FT seems to be the only place where data isn't too tarnished with propaganda...

Ah, this is perhaps where we differ; I dont read it for its articles on Thailand.

That wasn't so much the disaease as the most obvious symptom to me of a general and deep-rooted malaise...

-

Good observation Paul. Both Stratfor and the Economist read like mouthpieces for various "think tanks", all with an agenda.

Yet again, I find myself saying "I wish I'd said that, Oscar..."

-

Israel's vicitim status may be the only constant.

Your falling for a propaganda stunt. The Israelis let tons of aid into Gaza all the time.

I believe that the international agencies say that only around 25% of the neccessary aid is allowed to reach Gaza but the most valid point on this thread is that none of us really know the full facts. Making outlandish definitive statements in support or criticism of one side or another from our keyboards at this stage probably just highlights our own gullibility or our own prejudices and therefore is as much a waste of time (just like some of the threads on here during the recent Bkk troubles when pro-reds posted pro-red posts and anti-reds posted anti-red posts).

This is a very serious issue and one on which everyone's obviously entitled to express an opinion and a strong opinion at that but as in most things if you assume that it's all black or all white you might well be missing some of the story and if you post your opinion as though it's fact then you're misleading everyone including yourself. We're all guilty, myself included and the tendency is greater the more emotive the issue.....

-

Perhaps Im not paranoid enough?

Been an Economist subscriber for years. I do have a soft spot for British tory papers though

I stopped my Economist subscription when I realized that I could write much better articles about Thailand myself and that Asia Times, FEER etc wrote much, muc, much better articles about Thailand. FT seems to be the only place where data isn't too tarnished with propaganda...

-

I have decided to wait because the stock is not below its March 9/2008 low. If it goes below that then Im in.

I see - what about the positions of the sun, moon & stars? Would they also impact the decision?

or maybe what colour socks you're wearing?

Generally, Sokal, except for your 'G' habit, you make a lot of sense but this time, my friend, I think you've lost it.......

-

Well Naam what do you think about today's events ? " Those who cannot be named " have really shown their true

colours today........ not that i needed convincing otherwise anyway

But i can't believe the silly buggers chose to attack the Turkish boat

You know I did not quite understand what you meant midas by " those that cannot be named"

Now I know what you mean & find it very surprising........... I also didn't realize this all took place in International waters.

Turkey is preparing to send another flotilla with a serious Navy escort.

The bigger problem is that Turkey and Israel are the closest US allies in the region and the US is faced with having to choose between right and wrong, not between Israel and Turkey. The US will waffle as they already have and insist the Israelis are capable of conducting their own investigation into this matter. How rediculous is it to expect an unbiased investigation from the perpetrator.

Israel insists they are the victims here. They are always the victims so no surprise. No matter the facts, they are the victims and it is this position that encourages anti-semetism around the world.

Big problem with this also is, Turkey has a very powerful conventional military and one that will likely steam roll Israel into using nuclear weapons that they claim they do not have. We could see WW3 on this one and we are all affected to a huge degree.

Maybe this could be the powderkeg? I still don't think so yet - While Israel's subsequent actions remain provocative, Turkey alone seems propelled by righteous indignation to act. Cool heads seem still likely to prevail but I don't rule out the tension ratcheting up either but as Badge said, we keyboard diplomats have no idea what's going on behind the scenes but hopefully it's all leading to a peaceful solution that also results in a softening of hard line stances, more aid to Gaza and a greater all round respect for human life.

Financial Crisis

in Jobs, Economy, Banking, Business, Investments

Posted

Gold miners look interesting value right now but they're a ahem mine field - in my experience, this is a highly specialised and very under-researched area well exploited by Evy Hambro and the team at BlackRock

Gold on a structural basis makes sense to $ 2000 - sentiment could then drive it on anywhere from there - but the further above $ 2000 it goes, the more we're getting into nosebleed territory when it all goes wrong......