.png.3b3332cc2256ad0edbc2fe9404feeef0.png)

- Popular Post

Guavaman

-

Posts

140 -

Joined

-

Last visited

Content Type

Profiles

Forums

Downloads

Posts posted by Guavaman

-

-

- Popular Post

- Popular Post

Assessable Income in Thailand

Source: Tilleke & Gibbins Thailand Tax Guide:

2. Taxable Base

The taxable base is determined by deducting certain allowances from the total assessable income. The total assessable income is determined by aggregating the amounts under the different categories of income after deducting certain permitted expenses from assessable income of each category.

In general, all types of income are assessable unless expressly exempt by law.

https://www.tilleke.com/wp-content/uploads/2011/05/Thailand-Tax-Guide.pdf

Source: MoneyMgmnt

Assessable & taxable income

All types of income are generally assessable unless expressly exempt by law (see the exemptions below).

You can read the Revenue Code (Section 40) for more details about each type.

While assessable income represents a total of income that counts towards your tax liability, taxable income/base is the actual amount on which you pay tax. You can calculate it by subtracting deductions & allowances from your assessable income:

Taxable income = Assessable income (excl. exempt income) - Deductions - Allowance

Tax-exempt income

Currently, there are 29 income categories exempt from personal income tax. Below is a summary of some of those most likely to apply to foreigners living in Thailand (courtesy of the Revenue Code):

You can find the full list in the Revenue Code (Section 42).

https://www.moneymgmnt.com/tax/personal-income-tax-thailand/

-

1

1

-

2

2

-

3 hours ago, TroubleandGrumpy said:

I am very/extremely doubtful that the definition of assessable income used by some people on this forum is correct. My read of the Thai RD tax guide is that assessable income means taxable income. I am certain that the Thai RD does require Expats to report all the money they remitted into Thailand from their own personal saving - or from other non-taxable sources such as inheritences or property sales made overseas (that was bought with their owen money from overseas). However rental payments received from property overseas is taxable income.

Source: Tilleke & Gibbins Thailand Tax Guide:

2. Taxable Base

The taxable base is determined by deducting certain allowances from the total assessable income. The total assessable income is determined by aggregating the amounts under the different categories of income after deducting certain permitted expenses from assessable income of each category.

In general, all types of income are assessable unless expressly exempt by law.

https://www.tilleke.com/wp-content/uploads/2011/05/Thailand-Tax-Guide.pdf

Source: MoneyMgmnt

Assessable & taxable income

All types of income are generally assessable unless expressly exempt by law (see the exemptions below).

You can read the Revenue Code (Section 40) for more details about each type.

While assessable income represents a total of income that counts towards your tax liability, taxable income/base is the actual amount on which you pay tax. You can calculate it by subtracting deductions & allowances from your assessable income:

Taxable income = Assessable income (excl. exempt income) - Deductions - Allowance

Tax-exempt income

Currently, there are 29 income categories exempt from personal income tax. Below is a summary of some of those most likely to apply to foreigners living in Thailand (courtesy of the Revenue Code):

You can find the full list in the Revenue Code (Section 42).

https://www.moneymgmnt.com/tax/personal-income-tax-thailand/

-

1

-

1

-

-

46 minutes ago, Mike Lister said:

I see nothing that states that a retired/married Expat who does not earn income from employment must lodge a tax return in any Thai RD document or Thai Govt websites that relates to Expats not erarning income from employment. The document you quote from is not relevent to Expats, unless they are earning an income from employment.

Stating that something is 'understood to mean assessable income' as a fact, when it is your opinion, is not right. If the Thai RD has stated that as a fact in a document that is relevent to non-working Expats, then please provide it.

Under the Revenue Code, income from a pension is assessable income.

https://www.rd.go.th/english/37749.html

Revenue Code

Chapter 3 Income Tax

Section 40 Assessable income is income of the following categories including any amount of tax paid by the payer of income or by any other person on behalf of a taxpayer.

(1) Income derived from employment, whether in the form of salary, wage, per diem, bonus, bounty, gratuity, pension, house rent allowance, monetary value of rent-free residence provided by an employer, payment of debt liability of an employee made by an employer, or any money, property or benefit derived from employment.

Section 56 Every taxpayer except a minor or a person adjudged incompetent or quasi-incompetent shall, on or before the last day of March every year, file to the official appointed by the Minister a tax return reporting the assessable income received in the preceding tax year in the form prescribed by the Director-General, if such person -

(1) has no spouse and has the assessable income of the preceding tax year exceeds 60,000 baht,

(2) has no spouse and has the assessable income of the preceding tax year under only Section 40 (1) exceeds 120,000 baht,

(3) has a spouse and the assessable income of the preceding tax year exceeds 120,000 baht, or

(4) has a spouse and the assessable income of the preceding tax year under only Section 40 (1) exceeds 220,000 baht.

Thai Tax 2022/23 Booklet - PricewaterhouseCoopers Legal & Tax Consultants Limited

https://www.pwc.com/th/en/tax/assets/thai-tax/thai-tax-2022-23-booklet.pdf

Tax administration

Thailand applies a self-assessment system in collecting taxes. Taxpayers are required to declare their tax liabilities in the prescribed tax returns and pay the tax due at the time of filing.

The following individuals are required to file income tax returns for income earned in the preceding tax year irrespective of whether there is any tax due:

• A person who has no spouse and earns income of more than Baht 60,000

• A person who has no spouse and earns income under category (1) (salaries and wages) of more than Baht 120,000

• A person who has a spouse and earns income of more than Baht 120,000

• A person who has a spouse and earns income under category (1) (salaries and wages) of more than Baht 220,000.

-

1

-

-

2 hours ago, Mike Lister said:

Para 23 of the document currently reads:

Who must file a tax return? The English language translation of the RD rule says that, "You have to file a return on the income that you received if you meet one of the following conditions:

(1) Your total income exceeded 120,000 baht in the tax year.

(2) You were married and your income combined with that of your spouse exceeded 220,000 baht in the tax year."

This is understood to mean assessable income.

(Note: you had this debate with Sheryl to the point of exhaustion, in the long thread)

https://www.rd.go.th/fileadmin/download/english_form/030265guide91.pdf

As I have pointed out before, it is unfortunate that the RD website unofficial English translations contain inaccuracies and outdated information. The Guide to tax return form PND 91 is an example: Where the guide states "total income", the Revenue Code states "assessable income", which is an accurate translation of เงินได้พึงประเมิน: ngoen dai (income) + pheung (must) + pramoen (assess).

I suggest replacing the reference document to the RD Revenue Code as follows:

https://www.rd.go.th/english/37749.html

Revenue Code - Chapter 3 Income Tax

Section 56 Every taxpayer except a minor or a person adjudged incompetent or quasi-incompetent shall, on or before the last day of March every year, file to the official appointed by the Minister a tax return reporting the assessable income received in the preceding tax year in the form prescribed by the Director-General, if such person -

(1) has no spouse and has the assessable income of the preceding tax year exceeds 60,000 baht,

(2) has no spouse and has the assessable income of the preceding tax year under only Section 40 (1) exceeds 120,000 baht,

(3) has a spouse and the assessable income of the preceding tax year exceeds 120,000 baht, or

(4) has a spouse and the assessable income of the preceding tax year under only Section 40 (1) exceeds 220,000 baht.

Note these requirements apply to "Every taxpayer".

Regarding offshore income, the issue of earned vs. remitted, or received vs. brought into Thailand, here is a summary by Baker McKenzie:

Order No. 161 and Order No. 162 collectively reveal the Revenue Department's position on Thai personal income taxation on offshore-sourced income, summarized as follows:

Offshore-sourced income

Applicable interpretation

Thai personal income tax consideration

Offshore-sourced income received by Thai tax resident individuals before 1 January 2024

- Not subject to the new interpretation under Order No. 161

- Offshore-sourced income that is brought into Thailand after the calendar year of receipt is not subject to Thai personal income tax.

Offshore-sourced income received before 1 January 2024 can be brought into Thailand on or after 1 January 2024 without being subject to Thai personal income tax.

Offshore-sourced income received by Thai tax resident individuals from 1 January 2024

- Subject to the new interpretation under Order No. 161

- Offshore-sourced income that is brought into Thailand from 1 January 2024 onward is subject to Thai personal income tax.

Offshore-sourced income received from 1 January 2024 and brought into Thailand on or after 1 January 2024 will be subject to Thai personal income tax.

-

1

-

1 hour ago, TroubleandGrumpy said:

Technicality BUT it should read - "taxable income over 120K".

It should read: "assessable income over 120k".

Who must file Form PND 91?

A person must file a PND 91 if they have income as set out in Section 40(1) of the Revenue Code and meet one of the following conditions:

1. Single Person

Assessable income exceeding 120,000 baht in the tax year.

2. Married Person

Assessable income, combined with that of your spouse, exceeding 220,000 baht in the tax year.

-

1

1

-

1

1

-

-

Good Mike - As we know, most Thais are not into hair-splitting on conceptual issues, but that is the domain of the tax lawyers and accountants who are the priests of the tax world.

-

1

-

-

4 minutes ago, Mike Lister said:

Assessable Income means income that is taxable, i.e applied to the tax tables to determine the amount of tax due, which may be from 0% to 35%.

Correction:

According to the RD instructions for computation of personal income tax:

Taxable income = Assessable income minus exemptions, deductions, allowances.

-

1

-

-

12 minutes ago, Mike Lister said:

I was surprised to see you post this. I think it was @JimGant who posted the precise wording from teh DTA that set this out. I will try to see if I can find it amongst the 200+ pages, or perhaps JG can do so?

NOTE: I did not mean to imply that US Social Security benefit payments are taxable by the RD. Again, the issue is about assessable income. We understand that US Social Security benefit payments should be EXEMPT from taxation by the RD, even though that income is ASSESSABLE, since it "may be computed into a monetary value".

.

Section 39 In this Chapter, unless the context otherwise requires:

Assessable income means income that is taxable under this Chapter. Such income also includes a property or any other benefit received which may be computed into a monetary value.

-

1

-

1

-

-

3 minutes ago, ChasingTheSun said:

So the GREAT NEWS is now xonfirmed that the monetary value of all assets(stocks, bonds, cash, homes etc) held as of December 31 2023 overseas will NOT be taxed if ever remitted to Thailand at a later date?

Yes, according to Revenue Department Order 162, those assets are exempt from Thai income tax when remitted. The challenge is in providing evidence that is acceptable to "Somchai the local tax assessor" to prove that these assets were in your possession prior to 1 January 2024.

-

1

-

-

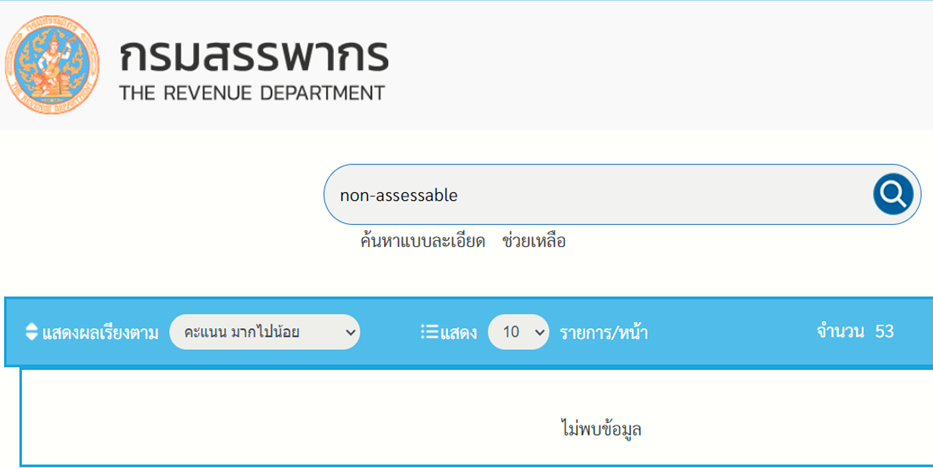

It appears that there is no reference in the Thai Tax Code that states that any type of income is non-assessable. If anyone can find such a reference, please inform us.

-

1

-

-

1 hour ago, chickenslegs said:

My question to the experts is: If I pay for goods and services directly from my UK bank/credit union/building society (for school fees, household goods, wine, groceries, etc) will that be classed as assessable income?

For example, I recently paid about 6000THB online for half a case of wine. The payment was made using Wise transfer from my UK account. Would this be classed as assessable income ?

According to the Thai Tax Code:

Section 39 In this Chapter, unless the context otherwise requires:

Assessable income means income that is taxable under this Chapter. Such income also includes a property or any other benefit received which may be computed into a monetary value.

Since the Thai Tax Code regarding foreign source income is based upon remittance into Thailand, such remittances of assessable income are subject to personal income tax in Thailand.

-

1

-

-

1 hour ago, JimGant said:

I just need to know if I have a legal obligation to file a Thai Tax return if I have no assessable income

The only way to answer this question is for a Thai RD tax assessor to consider your submission of a tax filing to determine whether or not you have assessable income.

-

33 minutes ago, LikeItHot said:

They know exactly where I am. They have my email address and phone number. I just did a 90 report and provided both as I always do even though not required just in case they want to give me a call. They made me sign a very specific form confirming I cannot work here. They never said anything about taxes. If they do I'll deal with it then from that day forward and not retroactively.

I have never received any direct communication from the tax authority in my native country informing me that I was subject to tax laws, or any other laws.

As they say, ignorance of the law is no excuse.

-

1

-

-

21 minutes ago, LikeItHot said:

Everyone is saying the single personal allowance deduction is 60000 but the link to deductions say 30000. Which is correct?

It appears that you have accessed this (outdated) regarding information about Personal Income Tax (PIT) here:

https://www.rd.go.th/english/6045.html

All of the amounts in all of the tables are OUTDATED.

The first & most important point to learn about the Thai tax system is this:

NEVER trust any information in an unofficial translation on the Revenue Department website.

For example, the webpage referenced = Last updated: 23.11.2020

A seeker will find other outdated references and amounts stated on the RD webpages.

This is Thailand: What you see is only the tip of an enormous iceberg.

Suggestion: Find 3 "reliable sources" (not including the Revenue Department) that all match, then you might be getting close to what the experts in Bangkok agree upon. Regarding what Somchai in the local district Revenue Office understands --- Welcome to Wonderland!

-

3 hours ago, Sheryl said:

If the only income coming into Thailand is from SS, there is 0 assessable income...and therefore no need to file a tax return or pay tax in Thailand.

Please provide your sources of authority on stating that:

1) Social security benefit payments are NOT assessable income according to Thai RD

2) No need to file a tax return, if no tax payable.

Then we can jointly consider the implications for us taxpayers.

This could be good news for many of us.

-

1

-

-

2 hours ago, Sheryl said:

If the only income coming into Thailand is from SS, there is 0 assessable income.

We -- the inhabitants of this forum/thread -- have still not understood the most fundamental term/meaning upon which the entire Thai income taxation system is based: Assessable Income.

Section 39 In this Chapter, unless the context otherwise requires:

Assessable income means income that is taxable under this Chapter. Such income also includes a property or any other benefit received which may be computed into a monetary value.

"Assessable" income that is taxable may be computed into a monetary value.

* The unstated implication is that income that may NOT be computed into a monetary value is NOT assessable. The Thai Tax Code does not address the concept of non-assessable income.

How the RD deals with US Social Security under the DTA as policy implemented at local levels remains to be seen.

-

1

-

-

- Popular Post

- Popular Post

1 hour ago, Sheryl said:No tax owed in Thailand, and no need to file a tax return in Thailand.

If true, this is a very important assertion, for which clarification is lacking to date.

I have been studying the Thai Tax Code for 3 months, but I have not yet come across this concept: filing a nil return, with no tax payable, meaning (in Thailand):

Taxable income = assessable income minus: exemptions, deductions, allowances = 0 Baht.

Please provide a reference link to a Revenue Department webpage or a legal/tax firm webpage that provides advice that Thai tax residents are not required to file tax returns if the taxpayer self-determines that they "owe no tax".

TIT caveat: This is Thailand (TIT). As we have learned, a primary loveable aspect of Thai people is their radical empiricism -- responding to events in the most practical way for that particular person, muddling through in uncertainty, which underlies everything, everywhere, everytime.

-

2

-

1

-

1 hour ago, Mike Lister said:

There are two tax forms, PND 90 and 91. PND 90 is for people with income from Thai bank savings only, PND 91 is fo0r those with bank savings and other income. The threshold for PND 90 is 60k Baht, and for PND 91, 120k Baht.

Unfortunately, it is not that simple. The decision point is whether or not the tax resident has income from only category 1 (employment including pensions) or from category 1 plus any other of the 8 categories of assessable income. See NOTE regarding Thai bank withholding tax on interest below.

REFERENCE: https://www.rsm.global/thailand/insights/rsm-focus/filing-pnd90-and-pnd91

PND.90 return is the personal income tax return to report the assessable income under Section 40(1) to (8)

[Assessable income under Section 40 of the Revenue Code:

1. Employment (including pensions)

2. Independent personal services

3. Goodwill, copyright and other (intangible) rights

4. Interest income, dividends and capital gains

5. Rental from property

6. Professional services

7. Hire of work (i.e., services contracts) ]

8. Business, commerce, agriculture, industry, transport, etc.]

PND.91 return is the personal income tax return to report the assessable income under Section 40(1) obtained from employment [category 1 only]

[(40(1) Income derived from employment, whether in the form of salary, wage, per diem, bonus, bounty, gratuity, pension, house rent allowance, monetary value of rent-free residence provided by an employer, payment of debt liability of an employee made by an employer, or any money, property or benefit derived from employment.]

Who is liable to pay personal income tax?

Filing of PND.90/91 returns are summarized below:

PND.90 return [income under Section 40(1) to (8)]

PND.91 return [income under Section 40(1) derived from employment only]

Single status and assessable income exceeding 60,000 baht.

Single status and assessable income exceeding 120,000 baht.

Marriage status and assessable income together exceeding 120,000 baht

Marriage status and assessable income together exceeding 220,000 baht

[Note Regarding Thai bank withholding tax on interest : If a taxpayer chooses to file PND. 91, it means that the taxpayer accepts the default 15% withholding tax on interest on deposits in Thai bank accounts. If the taxpayer chooses to claim any refund of that withholding tax, the taxpayer must file the more comprehensive PND. 90 filing form.]

-

1

-

-

- Popular Post

- Popular Post

34 minutes ago, jerrymahoney said:3. Thai RD is NOT interested in non assessable income

Same problem -- nothing personal. Many posters have used the term "non-assessable" according to their personal idiosyncratic definition of the term. What is assessable is up to the RD tax code and the tax assessor, not up to the opinion of the taxpayer.

The problem has arisen due to so many posters using the term according to their own individual definition of the term, most often confusing the concept of exemption to mean non-assessment. With so many pages of posts with misuse of the term, it has taken on its' own meaning in this thread as defined by the crowd, rather than by the RD.

-

1

-

1

-

3

-

10 minutes ago, jerrymahoney said:

If you do a search for 'non-assessable' you will find plenty have also used that term

Yes, that is a problem: we don't have the luxury of defining Thai tax law terms as we wish. The RD sets the rules and definitions. We can't just say: "My social security benefit payment is non-assessable income, so it doesn't count for the income threshold for filing a tax return", or "I already paid tax on my pension in my home country, so it is non-assessable income in Thailand".

It is ALL assessable income when remitted, although some of it may be EXEMPTED from taxation by the RD.

-

1

-

-

19 hours ago, jerrymahoney said:

nd this is for non-Assessable income:

Section 42 The assessable income of the following categories shall be exempt for the purpose of income tax calculation:

https://www.rd.go.th/english/37749.html (scroll down)

Regarding "non-assessable" income:

ASSESSABLE VS TAXABLE INCOME

All personal income tax (PIT) in Thailand is collected upon the basis of ASSESSABLE INCOME.

https://www.rd.go.th/english/37749.html

Section 38 Income tax is an assessment tax. An assessment official shall make assessment on tax under this Chapter.

This means that the taxpayer must compile their income-related information and use that information to prepare and submit a tax return to the RD summarizing the amount of their income that meets the characteristics as assessable income. The taxpayer, after calculating according to the characteristics, methods, conditions, rates set, and the burden of paying taxes, gives it to the tax assessor to determine the correctness of the taxable amount and the practice of duties of the taxpayer.

Section 39 In this Chapter, unless the context otherwise requires:

Assessable income means income that is taxable under this Chapter. Such income also includes an asset [property] or any other benefit received which may be computed into a monetary value, any amount of tax paid by the payer of income or by any other person on behalf of a taxpayer and tax credit under Section 47 Bis.

https://www.rd.go.th/english/37749.html

So what is non-assessable income?

This does not appear in the Thai tax code. One could imagine that it would be an asset [property] or any other benefit received which may NOT be computed into a monetary value; however, that would only be an imagination, because the concept of non-assessable income is absent from the tax code.

A search of the The Thai Revenue Department website results in 0 results for “non-assessable”.

The “non-assessable income” Straw Man does not exist.

What does this mean for expat Thai tax residents?

The RD defines 8 categories of assessable income. All of your “assessable income” falls within one of these 8 categories.

ASSESSABLE INCOME EXEMPT FROM INCOME TAX CALCULATION

Under Section 42, The assessable income of some categories are exempt for the purpose of income tax calculation; however, the tax code has no references to income derived under DTAs , although the content of DTAs specifically state that some categories of income are exempt from taxation in Thailand.

Section 42 The assessable income of the following categories shall be exempt for the purpose of income tax calculation:

(1) Per diem or transport expenses (2) Transport expenses and traveling per diem at the rates prescribed by the Government in the Royal Decree governing the rates of transport expenses and traveling per diem.

(3) The part of traveling expenses paid by the employer to the employee which the employee spent wholly and necessarily in traveling …

(4) Where a contract of employment which was bona fide entered into before the entry into force of the Royal Act on Income Tax B.E. 2475 …

(5) Special post allowance, house rent allowance and rent free residence granted to an official of a Thai embassy or consulate abroad.

(6) Income from a sale or discount received from purchase stamp duties or government postage stamps.

(7) Board or committee meeting allowance and teaching and examination fees paid by the government or public educational institutions.

(8) The following interest:

(a) Interest from Government savings lotteries, or interest on demand deposit with the Government Savings Bank;

(b) Interest on savings deposit with a cooperative;

(c) Interest on savings deposit with a bank in Thailand which is repayable on demand;

(9) Sale of a movable property acquired from inheritance …

(10) Income derived from an inheritance.11

(11) Award for the purpose of education or technical research, government lottery and government savings prize, prize given by government authority in contest or competition to a person other than a professional contestant or competitor, or reward paid by government authority for the purpose of prevention of wrongdoing.

(12) Special pension, special gratuity, inherited pension or inherited gratuity.

(13) Compensation against wrongful acts, amount derived from insurance or from funeral assistance scheme.

(15) Income of a farmer from sale of rice cultivated by the farmer and/or his family.

(16) Income derived from an undivided estate liable to tax under Section 57 Bis.

(17) Income prescribed for exemption by Ministerial Regulations.12

(18) Red Cross lottery prize, income from a sale or discount received from purchase of Red Cross lotteries.

(19) Interest received under Section 4 Decem.13

(23) Income from sale of investment units in a mutual fund.

(24) Income of a mutual fund.

(25) Compensatory benefit received by the taxpayer from the social security fund under the law governing social security.

(26) Income derived from the transfer of ownership or possessory right in an immovable property without any consideration to a legitimate child …

(27) Income derived from maintenance and support or gifts from ascendants, descendants or spouse, but only for the portion not exceeding twenty million Baht throughout the tax year.

(28) Income derived from maintenances and support under moral purposes or gifts received in a ceremony or on occasions in accordance with custom and tradition from persons who are not ascendants, descendants or spouse, but only for the portion not exceeding ten million baht throughout the tax year.

(29) Income derived from gifts whereby a donor has expressed his or her intention or appeared to have an intention of using the gifts for religious, educational or public benefit activities in accordance with the rules and conditions as prescribed by a Ministerial Regulation.

So there is assessable income that is taxable and assessable income that is exempt from tax, but "non-assessable" income is not a "thing".

You can stop thinking and claiming that that some of your income is non-assessable.

-

52 minutes ago, Thailand J said:

Open your eyes, non of us here who stay in Thailand ever paid Thai tax on our IRA distributions.

You are speaking on behalf of all American tax residents in Thailand when you say: "None of us."

The future might not look like the past.

The RD is providing hints about what the future may look like. It remains to be experienced.

-

13 minutes ago, Guavaman said:7 minutes ago, Thailand J said:

Please lets stay with Thai-US tax can we?

US- THAILAND CONVENTION

The Treasury Department's 1996 Technical Explanation ("TE") to Article 20 explains, in relevant part:

Paragraph 1 provides that private pensions and other similar remuneration paid in consideration of past employment are generally taxable only in the residence State of the recipient.

-

40 minutes ago, Thailand J said:

Does Swits has the exact same DTA with US as Thai?

US- SWITZERLAND CONVENTION

US-THAILAND CONVENTION

The Treasury Department's 1997 Technical Explanation ("TE") to Article 18 explains, in relevant part:

Paragraph 1 provides that private pensions and other similar remuneration derived and beneficially owned by a resident of a Contracting State in consideration of past employment are taxable only in the State of residence of the recipient.

The Treasury Department's 1996 Technical Explanation ("TE") to Article 20 explains, in relevant part:

Paragraph 1 provides that private pensions and other similar remuneration paid in

consideration of past employment are generally taxable only in the residence State of the recipient.

Thai government to tax (remitted) income from abroad for tax residents starting 2024

in Jobs, Economy, Banking, Business, Investments

Posted

ISSUE: Online source of tax information contradicts US-Thailand DTA and US Department of the Treasury Technical Explanation https://home.treasury.gov/system/files/131/Treaty-Thailand-TE-11-26-1996.pdf

This quoted statement from an online legal source is misleading – it is only partially correct; that is:

- Government pensions, social security benefits, alimony & child support benefits are taxable only in the state where they arise. (US) – Paragraphs 2, 4 & 5 of Article 20, and Paragraph 2 of Article 21 (Government Service)

- Private pensions and annuities are taxable only in the residence State of the recipient (Thailand for tax residents) – Paragraphs 1 & 3 of Article 20

The lesson here is that one cannot simply accept a single source of tax information from non-Revenue Department sources.

ARTICLE 20

Pensions and Social Security Payments

1. Subject to the provisions of paragraph 2 of Article 21 (Government Service), pensions and other similar remuneration paid to a resident of a Contracting State in consideration of past employment shall be taxable only in that State.

TECHNICAL EXPLANATION:

Paragraph 1

Paragraph 1 provides that private pensions and other similar remuneration paid in consideration of past employment are generally taxable only in the residence State of the recipient.

2. Notwithstanding the provisions of paragraph 1, social security benefits and other similar public pensions paid by a Contracting State to a resident of the other Contracting State or a citizen of the United States shall be taxable only in the first-mentioned State.

TECHNICAL EXPLANATION:

Paragraph 2

The treatment of social security benefits is dealt with in paragraph 2. This paragraph provides that, notwithstanding the provision of paragraph 1 under which private pensions are taxable exclusively in the State of residence of the beneficial owner, payments made by one of the Contracting States as a social security benefit or similar public pension to a resident of the other Contracting State or to a citizen of the United States will be taxable only in the Contracting State making the payment.

3. Annuities derived and beneficially owned by a resident of a Contracting State shall be taxable only in that State.

TECHNICAL EXPLANATION:

Paragraph 3

Under paragraph 3, annuities that are derived and beneficially owned by a resident of a Contracting State are taxable only in that State.

4. Alimony paid to a resident of a Contracting State shall be taxable only in that State.

5. Periodic payments, not dealt with in paragraph 4, for the support of a child made pursuant to a written separation agreement or a decree of divorce, separate maintenance, or compulsory support, paid by a resident of a Contracting State to a resident of the other Contracting State, shall be taxable only in the first-mentioned State.

TECHNICAL EXPLANATION:

Paragraphs 4 and 5

Paragraphs 4 and 5 deal with alimony and child support payments. Both alimony, under paragraph 4, and child support payments, under paragraph 5, are defined as periodic payments made pursuant to a written separation agreement or a decree of divorce, separate maintenance, or compulsory support. Paragraph 4, however, deals only with payments of that type that are taxable to the payee. Under that paragraph, alimony paid by a resident of a Contracting State to a resident of the other Contracting State is taxable under the Convention only in the State of residence of the recipient. Paragraph 5 deals with those periodic payments that are for the support of a child and that are not covered by paragraph 4 (i.e., those payments that are not taxable to the payee). These types of payments by a resident of a Contracting State to a resident of the other Contracting State are taxable only in the first-mentioned Contracting State.

ARTICLE 21

Government Service

2. a) Any pension paid by, or out of funds created by, a Contracting State or political subdivision or a local authority thereof to an individual in respect of services rendered to that State or subdivision or authority shall be taxable only in that State.

TECHNICAL EXPLANATION:

Paragraph 2

Paragraph 2 deals with the taxation of a pension paid by, or out of funds created by, one of the States or a political subdivision or a local authority thereof to an individual in respect of services rendered to that State or subdivision or authority. Pensions paid to retired civilian and military employees of a Government of either State are intended to be covered under paragraph 2.