Mike Lister

-

Posts

6,717 -

Joined

-

Last visited

-

Days Won

1

Content Type

Events

Forums

Downloads

Quizzes

Gallery

Blogs

Everything posted by Mike Lister

-

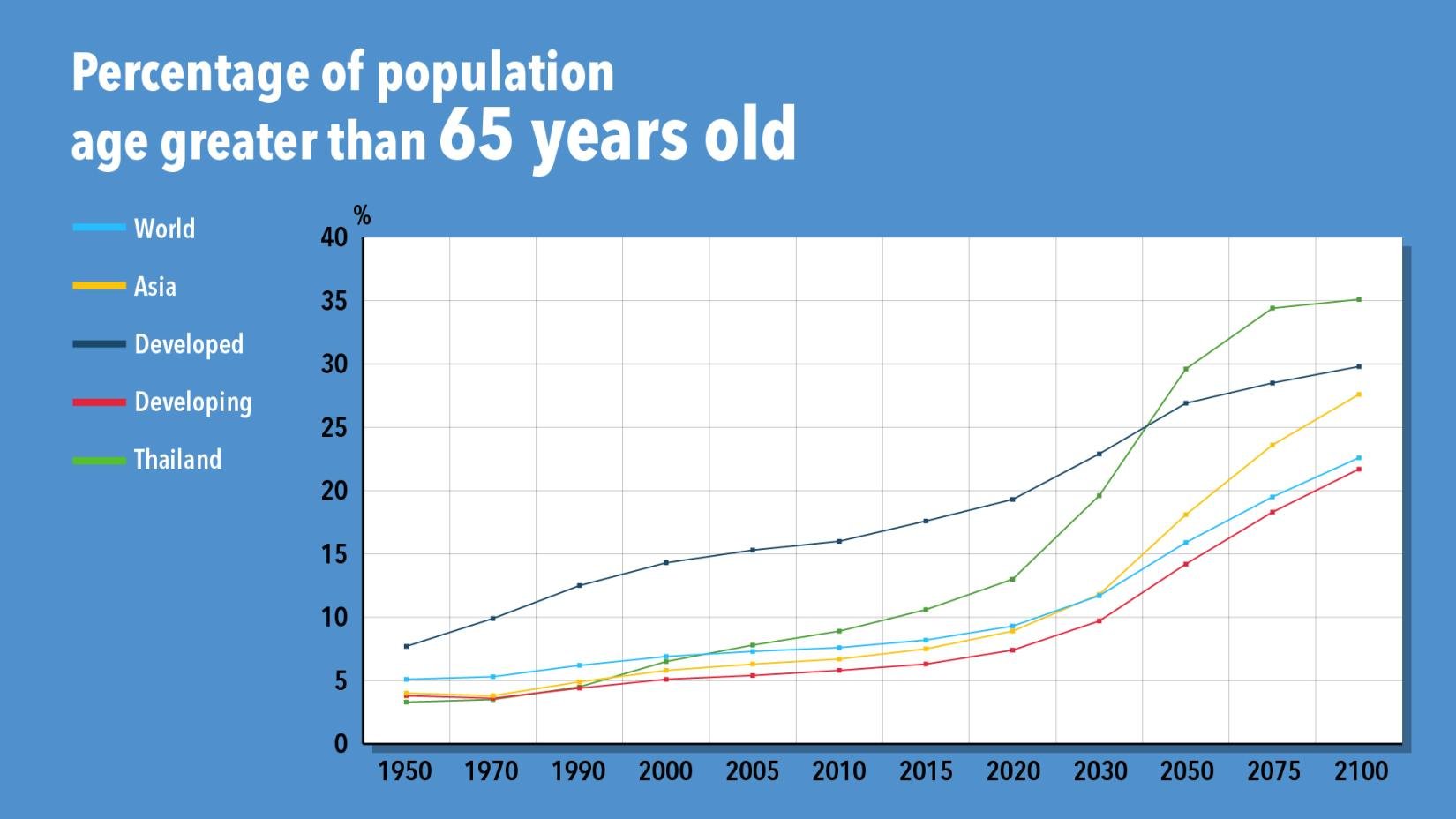

Believe it! https://thailand.un.org/en/96303-thailand-economic-focus-demographic-change-thailand-how-planners-can-prepare-future

-

I have incorporated all the changes that have been suggested into Version 5 of the Tax Guide (below) and asked the Moderators to pin it in a locked thread, within the Finance section. If anyone wishes to suggest further changes, you can either post them here and hope that I spot them, or, you can PM me with the suggestion which I will ensure is discussed by a wider audience. If there is agreement that further changes should be made, and/or as new developments occur, I will attempt to update the document to keep it current. A SIMPLE GUIDE TO PERSONAL INCOME TAX IN THAILAND 8 January, 2024 Version 5 1. This guide has been compiled in an attempt to provide readers with the simplest possible over view of Personal Income Tax (PIT) in Thailand. The scope of this document is limited to PIT. 2. You may have heard that new tax laws came into effect on 1 January this year, in fact, that is not true! The old tax rules still exist and remain valid, albeit just one minor change to them was made in November last year. Previously, anyone who earned money overseas and remitted it to Thailand in a different tax year, received that money free of Thai tax. That loop hole in the Revenue Department (RD) tax code has been extensively exploited by wealthy Thai’s and is now closed, hence, any money earned overseas and remitted to Thailand in any year, is now liable to Thai tax. The purpose of the new rule is to reduce tax avoidance. Unfortunately, it now means that overseas funds transfers by foreigners living in Thailand, also have an increased risk of being taxed. 3. This guide is an overview of the core parts of the PIT system. It is not designed to be exhaustive and it doesn’t cover all aspects of PIT, nor is it intended to override anything produced by the Thai Revenue or specialist tax companies such as Sherrings or Mazzars. This guide also does not address all types of income or the rules relevant to people from every country. What this guide will provide is a starting point for readers to manage their own tax affairs and it will also provide most of the answers for those with simple tax affairs, especially the average pensioner. 4. There are also certain types of visa that fall outside of the RD tax code. The LTR visa for example received its tax exempt status by royal decree hence visa holders will not to be assessed for Thai tax and they are specifically excluded from this explanation. 5. Terminology: this document uses the word “assessable” often. Assessable in the context of this document means income that is liable to tax and must be included on a Thai tax return. Not all income is assessable, some is excluded from tax assessment by its very nature or because of the terms of a specific tax agreement. 6. Dual Tax Agreement/Double Tax Agreement (DTA): is an agreement between two countries that sets out which of the two countries has the right to tax specific types of income and all the associated rules. It’s purpose, in part, is to ensure that the same funds are not taxed twice and provides a means by which tax that is paid twice, can be recovered, how and from where. Note: If the taxpayer income is sourced in one country but the tax payer is resident in a second country, use of a DTA can result in increased tax being paid, if the second country has a higher rate of tax on the type of income in question, than the other. 7. If you stay in Thailand for more than a cumulative 180 days, between 1 January and 31 December each year, you will be considered to be Tax Resident in Thailand during that year, regardless of the type of visa you have. It doesn’t matter that you may be Tax Resident in your home country or elsewhere or that you pay tax in those countries, Thailand will still regard you as Tax Resident. Tax Residency and Immigration status (and the visa you hold) are different things. Tax residency is based solely on the number of days you spend in Thailand and where you are at midnight on each day. 8. Because you are Tax Resident, YOU must review your income each year to determine if it is regarded as assessable to tax in Thailand, nobody else will do this for you. If your income does not exceed 120,000 baht per year, you do not need to file a tax return (60,000 baht if your only income is bank interest paid to you by a bank in Thailand). If your income is over 120,000 baht per year, you must file a Thai tax return between 1 January and 31 March. 9. Your income in Thailand is defined as any money paid to you inside Thailand, as well as, any money you receive from overseas, both types are potentially assessable income for Tax Residents. There are many types of income that can be classed as assessable, the Thai RD lists some of them and is linked below, however, the list is not exhaustive: https://sherrings.com/personal-income-tax-in-thailand.html#:~:text=Section%2040%20of%20Thailand's%20Revenue,Pensions%3B%20and 10. There are also classes or types of income that the RD does not regard as assessable and these are also linked below: https://www.rd.go.th/english/37749.html 11. Income that is derived from within Thailand is fairly clear, if you work and have a job and you are a Tax Resident, your income is assessable for tax. Interest that is paid to you on Thai bank accounts is regarded as income, as is income from investments such as stocks and bonds within Thailand. You should note that if you are generating income by working while staying in Thailand, it is (and has always been) irrelevant where that money is paid and whether you bring the money into the country or keep it offshore. That money arises in Thailand hence it is taxable here. 12. It is not possible to give the same blanket rule to everyone to determine whether income is assessable or not because of the variable factors involved. Overseas income has to pass several tests to determine if it is assessable to Thai tax or not. It is still early days and all the rules are not yet clear. It has been said that tax residents who import funds from countries that have a DTA with Thailand, will not be effected. Exactly how that will work leaves many questions unanswered hence this document attempts to look at only the most popular types of income based on what is known at present. This document does not speculate as to what may happen in the future, other than in the segment at the end concerning likely future Immigration rules. 13. If we take the simplest type of income and say that you transfer personal savings from overseas to Thailand and those savings were earned before 1 January 2024, those funds are not assessable. But savings earned after that date are, hence the date when the income is earned is extremely important. A word of caution, you may be asked to provide proof that savings were earned before 1 January 2024. 14. Another common type of income is pensions, which can be complicated, depending on the type of pension and the country that it comes from. The country of origin is important because there are over 60 different types of Dual Tax Agreements, sometimes called Double Taxation Agreements (DTA’s), between Thailand and those 60+ countries and each one is different. As a general rule, most private or company pensions from most countries appear to be assessable here but YOU will need to confirm that yours is or is not. If that is true, private and company pension income IS assessable income in Thailand. 15. US Social Security payments, a form of pension paid to some older people, can only be taxed by the US under DTA rules and Thailand is forbidden from taxing them, this means those payments are NOT assessable income. UK State pension on the other hand is not covered by a DTA so it is assessable income in Thailand whilst UK Government or Civil Service pensions are not! 16. The proceeds from the sale of a capital item such as overseas property, where funds are remitted to Thailand, is one popular source of funds, the sale of some investment products such as stocks, shares and bonds is another. Those proceeds typically comprise two parts, capital and profit. If the capital was acquired before 1 January 2024, it is free of Thai tax. One way to separate capital and profit may bee to have an official valuation or statement that is dated 1 January 2024 since anything earned before that date, is not assessable. Also, if the profit has been the subject of a Capital Gains return in the home country, that also may be free of Thai tax but this cannot be guaranteed at this time, until things are made more clear and are once again subject to the terms of any DTA. YOU will need to review the DTA between Thailand and your home country to fully understand what particular clauses affect you. 17. It appears as though most property rental income that is remitted to Thailand is considered to be assessable income and is taxable here, unless of course it has been taxed in the home country and/or the DTA prohibits its taxation (which seems unlikely). 18. YOU are responsible for determining if your assessable income in Thailand exceeds the threshold and means you must file a tax return. That assessable income might comprise, pension payments, investment income, rental income or any of the other types of income listed in the link above. If you have assessable income of over 120,000 baht per year, you must file a tax return (60,000 baht if your sole source of assessable income is bank interest paid in Thailand). 19. Before you can file a tax return in Thailand, you need to acquire a Tax Identification Number or TIN from the RD offices in your area. You will need your passport, a valid and current visa or extension and in many areas, a Certificate of Residency from the Immigration Department. 20. Completing a tax return is a simple affair for most people, if you have difficulty, the Revenue Department staff are extremely helpful. Tax returns must be filed between 1 January and 30 March each year, if you file later than that, penalties will apply. 21. Thai tax is layered in bands and is payable based on the amount of assessable income that falls within each band and are shown and linked below: Taxable Income per year(Baht) Tax rate 0 – 150,000 Exempt 150,000 – 300,000 5% 300,000 – 500,000 10% 500,000 – 750,000 15% 750,000 – 1,000,000 20% 1,000,000 – 2,000,000 25% 2,000,000 – 4,000,000 30% Over 4,000,000 35% https://www.mazars.co.th/Home/Insights/Doing-Business-in-Thailand/Payroll/Personal-Income-Tax 22. The Thai tax system contains a series of Allowances, Deductions and Exemptions that will help you reduce your tax bill and they are very generous. It is easily possible for the average expat foreign retiree to reduce their taxable income by 500,000 baht or more each year. For example, a retiree aged 65 years of age, married and living here full time, supporting a Thai wife who has no income and doesn’t file tax return, is allowed the following: a. Personal Allowance for self - 60,000 b. Personal Allowance for wife - 60,000 c. Over age 65 years exemption - 190,000 d. 50% of pension income received, up to 100k - 100,000 e. In addition, the first 150,000 of assessable income is zero rated and free of tax 23. Additional deductions and allowances exist for health or life insurance premiums paid in Thailand. A complete list of deductions, allowances and exemptions can be found here https://www.rd.go.th/english/6045.html or from Sherrings below. https://sherrings.com/personal-tax-deductions-allowances-thailand.html 24. The Thai Revenue tax filing system is online but is only available in Thai language at present. The tax forms are however available in English and they can be downloaded from the link below. CAUTION, the forms are updated every year and the 2023/24 forms for full year PIT are NOT yet available: https://www.rd.go.th/english/63902.html 25. A simple sample completed tax form for a person aged over 65 years is shown below as a guide. 26. https://aseannow.com/topic/1312534-taxation-of-ex-pats-pensions-etc/?do=findComment&comment=18532562 27. Tax filing in Thailand is based on the honour system, it relies on you declaring all the right information every year and there are severe penalties for evading Thai tax. It would be foolish and a gross under estimation of RD capabilities to think that doing nothing and keeping a low profile means you should ignore Thai taxation. Very few sane people in the US and UK ignore the tax authorities who tend to have a long reach. It cannot be ruled out that at some point, a link may be established between tax filings and visa extensions. A law already exists that requires foreigners to apply for Tax Clearance Certificates before being allowed to depart the country but it is not being enforced currently. These things are possible because similar things have been adopted in several countries in the past, including the US. 28. There are several sources of detailed tax information and these web sites are linked below: https://www.rd.go.th/english/6045.html https://sherrings.com/personal-income-tax-in-thailand.html https://www.mazars.co.th/Home/Insights/Doing-Business-in-Thailand/Payroll/Personal-Income-Tax *** END ***

-

Oh well, right there is the prime reason then, the expats weren't consulted first

-

Soooo, wanna call it a draw and go for a beer. :))

-

Ah, too bad LL, my link from BOT beats your link from the Thai Embassy in Singapore, sorry. But nice try though.

-

I feel it may snow tomorrow. :)

-

You're most welcome. Did you notice that I also posted a supporting quote and link as proof, is that quality or what. :))

-

Somebody's confused, how sad: Clause 1. Any person who exports or takes out from Thailand of the following currency or foreign currencies, such person shall declare details of such currency, foreign currencies or negotiable monetary instruments to Customs Officer while passing the customs as prescribed in the annex of this notification; (1) Currency which is currency notes or coins which their aggregate value exceeding 450,000 Baht (2) Foreign currencies which are foreign currency notes or coins which their aggregate value exceeding US$15,000 or its equivalent at market rate https://www.bot.or.th/content/dam/bot/documents/en/our-roles/financial-markets/foreign-exchange-regulations/laws-and-regulations/E_MOFControl6.pdf https://www.bot.or.th/en/our-roles/financial-markets/foreign-exchange-regulations/exchange-control-regulation.html

-

And the same rules apply for the export of foreign currency, USD15k or more, or other currencies in excess of THB 450k in value.

-

I'm not a lawyer, I suspect you aren't either.

-

You appear not to even understand how tax systems work, why even bother adding more drivel to an already drivel rich thread!

-

Once again, a new law vs an operational interpretation, I think people are grasping at straws by trying to argue this point.

-

Yes, over $20k.

-

Ah...."should be"! I'm not a lawyer and I haven't studied the issue so I can't comment with any certainty. But it does seem to me that the Director of the Revenue can issue operational instructions to his staff which is what he seems to have done. He hasn't changed the law or tried to make a new one, he's merely sought a legal view and offered a new interpretation, which he now wishes to operationalize. We might wish for things to be done in a certain way but should not be surprised when in Thailand that they are not.

-

The Investing Year Ahead

Mike Lister replied to Mike Lister's topic in Jobs, Economy, Banking, Business, Investments

I agree with Blackrock's logic that short term investment grade bonds with a duration of under 3 years is a better alternative than money markets as a place to park cash. Meanwhile. the long term agg index fund still looks like a good bet, even if some think rates could go either way. Also, the iShares Japan fund has done good things so far, up 13.4% thus far. -

Yet another page of drivel, just because the same poster makes it so, endlessly driving around the roundabout, looking for the very thing they're driving around.

-

The English usage is poor, I'll reword it. It intends to say that the tax filer is responsible for determining if the threshold has been reached.

-

Sherrings very clearly reports that as an instruction, effective 1 January 2024, not a proposal. https://sherrings.com/foreign-source-income-personal-tax-thailand.html

-

Facts are facts,other posters recommended ot earlier

-

Depends on the year the savings were earned

-

Not true

-

I did you should read the latest version

-

Others mileage may vary but I don't want to live my retirement years in a foreign country, looking over my shoulder and/or waiting for the hammer to fall.