Posts posted by Gaccha

-

-

1 hour ago, RupertIII said: Each year I pay my medical insurance annual premium by transferring GBP from an offshore investment a/c to Wise using BACS (no charge). This transfer can only be made to an a/c in my name.

I then transfer the GBP to the UK insurer's UK GBP a/c, once again using BACS. As the funds do not enter Thailand there is no tax liability.

So, does this mean that I will now have to transfer GBP from my offshore a/c to Wise Thailand, presumably by SWIFT with charges. Have the GBP converted to THB, at cost, convert back to GBP, at cost, and then transfer to the UK using SWIFT, at more cost. And then, to add insult to injury, pay Thai tax on the premium of several thousands of GBP?

As I live in Thailand with no other address, UK or otherwise, does anyone know of an alternative to Wise? Thanks.

In addition just noticed on the Expat Tax web site that non-THB balances can not be sent directly to overseas bank accounts. Effectively meaning I can not even pay the premium using Wise!

In all those various ways you just described you are exactly the kind of person who needs to act before the May date arrives. You don't have much time. You'll find that moving the money around and trying to liquidate assets and filling in all the paperwork will take a good solid month.

You might determine that simply taking the tax hit as well as the various conversion charges is the best way ahead.

From checking around I simply could not find a truly equal alternative to Wise among Fintech alternatives. There are certainly other companies that will send your money at cheap cost direct from your offshore account to a non-Thai location, but I think you'll find they do not offer the same auto transfer option or an option to sit the money with them. You would lose a lot of your flexibility and a lot of time.

An option that you might consider is opening a high-value or elite bank account in the third country to act as a new bridge between your various financial locations. Unfortunately this requires quite a large sum to be in the account for the bank to be willing to open it (banks typically do not want to open accounts for people not resident in a country) but they will open it for free and in fact they will throw money at you to open it.

Examples are Standard Chartered Priority, HSBC Premier, Citigold etc. the absolute cheapest that I can think of would be HSBC Premier in Malaysia which is probably only around $100, 000 of funds needed for them to open it. This option is very popular among wealthy Thais.

They all have pluses and minuses. HSBC will automatically upgrade all your accounts across the whole world to premier level and link the accounts. So if you opened the Malaysia one on the cheap then you would also get your UK account upgraded to Premier level as well. Suddenly you would find free transfer across the globe between the accounts.

By contrast the Citigold is exceptionally good for travellers with a great deal of perks, and has a very deep well of wealth fund options.

The details are really what will make them the right place for you and only you can decide that. But you must act.

I started looking around almost the instant I heard about this and it has taken me until this week to get it all done.

-

1

1

-

-

17 hours ago, Jingthing said: But based on age and health conditions not to mention cost, that isn't always possible.

Yes it is always possible. There are specific insurance policies designed to overcome visa conditions. For example, Insurte.

Inthe alternative very large insurance companies, such as Cigna Global, will offer you insurance no matter what your age and no matter what conditions. Of course they will exclude all the conditions but obviously you don't care since you are only getting the health insurance in order to get the visa. Once you've got the visa in the EU you can get state health access.

-

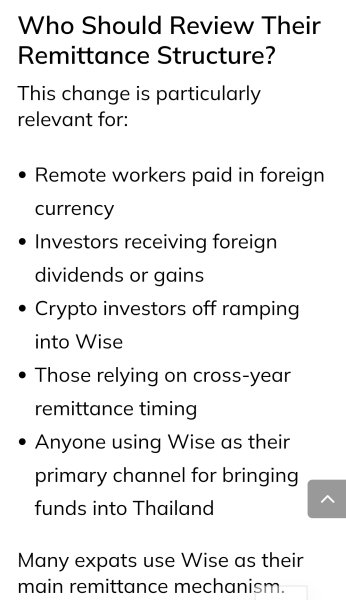

A tax expert website has offered a rather nice list of those people who will be especially affected in these upcoming May changes.

The key point is the issue of "remittance" in Thai tax law. Thailand has a remittance tax system unlike many other countries (the UK, by contrast, has for its tax residents a global tax regime). So controlling and timing or avoiding remittances is extremely important to minimise tax levels.

If like clockwork you simply move money month by month through Wise from a specific income source then probably nothing needs to be done.

But if you use Wise in a more sophisticated manner then this website will be worth reading:

https://www.expattaxthailand.com/wise-thailand-tax-update-2026/?hl=en-GB

I can think of a couple of crucial problem areas where the Wise account is used as a bridging mechanism:

-If you move money between two countries, neither of which are Thailand.

-You use the Wise virtual accounts for local transfers within a country between your own accounts. (If you have no idea what Wise virtual accounts are then you have nothing to worry about)

This website also makes similar points although not getting to the issue of tax:

https://neobanque.ch/blog/wise-bank-of-thailand-regulated-money-transfer-app/?hl=en-GB

-

1

1

-

-

On 3/21/2026 at 1:34 PM, Jim Waldron said: Keeping someone for over three months feels excessive to the point of being punitive.

She refused to buy a ticket because she feared her son would be taken off her by British social services (the SS) on arrival.

-

1

-

1

1

-

-

This is obviously a technical question that requires an answer from KBank.

Give them a ring. Within the app there is a way to ring a helpline through the internet, but since you cannot access it now you will simply have to ring their number the normal way: 02-8888888.

-

2

-

-

This is hilarious. They want to be rewarded for their attempt to avoid taxes, whilst their new neighbours, who didn't strategize to avoid taxes, have to pay the taxes. It should be the other way around.

-

2

2

-

-

1 hour ago, chang50 said: couldn't find "international transaction" is it the same as "enable online transactio

Don't worry. As long as you've set up the max limit to accept the transaction and everything is turned on then you have the best chance of success.

The modern bank security algorithm is far more sophisticated than 15 years ago. It will consider your payment is to a government body, know that it is your government etc. It is very likely to work.

-

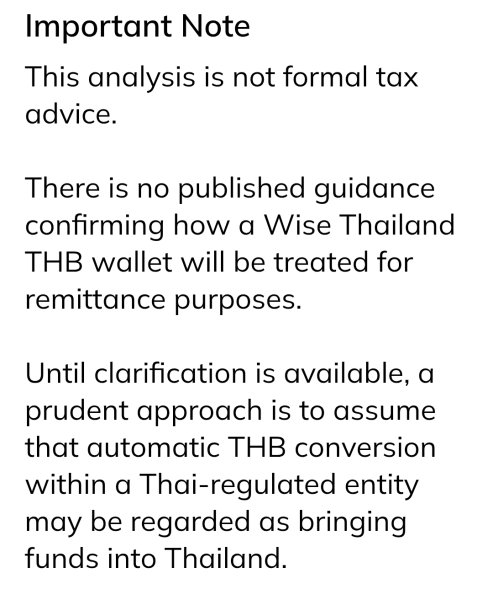

1 hour ago, oldcpu said: Taxation: Reference concerns re:Thailand tax ... IMHO it has always been a risk that money remitted to Thailand via an institution such as Wise could be tracked (for Thai taxation purposes) - - so has this really changed ?? IMHO only changed for those who considered there was no past risk for remitting such funds.

The issue is not a question of whether funds are tracked if remitted to Thailand. Obviously that will be the case. Indeed, it is tax evasion (a crime) to attempt otherwise.

The issue is the situation where you are counted as a having a Thai account. I appreciate that you are not. But I'm going to explain it anyway because your two question marks suggest you are bewildered by this.

The issue is that any movement of money from anywhere to anywhere will result in an autoconversion to Thai baht if your account is Thai based. The autoconversion will almost certainly count as a remittance in Thai tax law (experts are currently seeking clarification from Thailand's tax offices). And that means every satang will count towards your taxable income of that year.

For example, you put Euros from Germany into Wise in order to send them to your Hong Kong account. This is then instantly autoconverted. You convert it to Hong Kong dollars and send it on to Hong Kong. Despite this transaction having an appearance and the feel of having nothing to do with Thailand it is likely to count as a taxable remittance under Thai tax law under the new regulations of Wise.

Let's provide an example. You earn 30,000 euros in Thailand. You send 400,000 euros to Hong Kong from Germany. It goes nowhere near Thailand. It provides not a single extra satang for your life in Thailand. Your taxable income that year in Thailand will be at least 430,000. That would be an increase of tax payable from roughly 1 million baht to 12 million baht, without you earning even 1 satang more in your office job.

These changes then are extremely significant, indeed they are existentially significant, if you are Thai based and if you use Wise as a global linkage mechanism for tax avoidance (not to be confused with tax evasion) and other sensible measures.

-

1

1

-

1

-

-

I definitely used it (Kasikorn) successfully and my card at that time (2024) had "privileged member" on it.

Make sure in the App that you have high limits set for the card. Make sure that international transaction is set to on. And you have to hope that the security algorithm of Kasikorn that analyses your account's usage will not block the transaction.

-

15 minutes ago, Somrak said: if you are to lazzy to make the 90 day report it will cost you, when you make your next extension 2 k Bath.

The way to avoid the 2,000 baht fine is to arrive back within 90 days of an extension end date. If you time your travels right, you can skip 90 day reports with no consequence.

-

- Popular Post

39 minutes ago, SoCal1990 said: You can argue about it forever and still feel like you are doing something important while actually achieving nothing at all.

Political scientists describe this as political hobbyism. The function of the discussion is to fulfil the emotional needs of the spectator of politics rather than to actually do politics.

American politics is particularly satisfying as a spectator sport (especially so for non-Americans), because it is unusually divisive because it is multicultural. This multiculturalism ensures that since there are only limited shared foundations, the politics takes on a religious flavour.

Real politics, as the book above outlines, is extremely tedious. To the extent that even politicians and political journalists tend to avoid it and spend their time watching the structure of it (watching it like watching a horse race: who will win, who is getting promoted, who is losing) rather than the contents.

-

3

-

3

-

2 hours ago, wil iam not said: How will this be affected please, anyone

Your situation is the least complicated and the least affected by all this, but you are still affected.

The British Pound will immediately be converted to Thai baht. You are then free to immediately convert them back to pounds within Wise or you may keep them as Thai Baht.

For tax purposes, the moment of auto conversion to Thai baht will count as a "remittance" to Thailand (this is not yet certain but appears to be the likely situation). In other words, you cannot tactically wait for the Thai baht to weaken.

You cannot store the Thai baht away from the tax authorities for the reason below.

If you are a Thai tax resident then any money remitted into Thailand counts as taxable. However, as a pension, and for many other reasons, it is possible that the sum "remitted" is not taxable. In other words, the normal rules apply.

-

2 hours ago, JohnOFphon said: I'm not sure that I can maintain a balance in Wise NYC.. and transfer when I want.

I have a direct deposit going into that bank every month.

It sounds like, as soon as they receive my deposit, they will convert and transfer here

That's not going to happen. Below is the likely but not certain situation that will arise:

The money you move into Wise will be converted automatically to Thai baht. You can then convert it back to US dollars and sit it in your US dollar account. You will still have a US dollar currency account. If, however, you have a US dollar virtual account-- a very different thing-- that will probably vanish.

When it is auto converted to Thai baht it will be regarded as a 'remittance' in Thai tax law. So for example if you transfer $10,000 then your income in Thailand that year will increase by $10,000, even if that $10,000 you put into Wise you actually proceed to transfer to Germany or anywhere else in the World.

-

1

-

-

1 hour ago, SamSpade said: Can you please post the link

You're right. It seems the link function is inoperative. Here it is pasted out: https://www.expattaxthailand.com/wise-thailand-tax-update-2026/

-

1

-

-

On 2/27/2026 at 1:23 PM, Gaccha said: any money placed into Wise will count as a remittance under Thai income tax laws. Frustratingly, the linked page does not clearly state this but it is implied with everything else they write.

Now that a few days have gone by, advisory groups are starting to write their opinions. And it's not good news.

The opinion linked here by a tax specialist amplifies my fear that any money put into Wise in any currency in any part of the world will count as a remittance to Thailand. They are currently seeking clarification from Thailand's tax offices.

Of course if you were simply planning on using Wise to send money to Thailand then except for timing issues (to maximise currency conversion advantages) this does not change too much. But if you are using it as a global bridging mechanism then this is a huge issue.

For example, if you withdraw money from a financial institution in Hong Kong and transfer it to a Wise Hong Kong Virtual Account this will count instantly as a tax remittance in Thai law and count towards your income tax of that year.

Right now it behaves like a local transaction within Hong Kong. You use the standard local transfer mechanism and pay the local transfer mechanism rate and stay within the local currency. But with new rules you will withdraw and instantly become a target of Thailand's tax system and presumably pay an international rate of transfer.

Let me give you another example. You send a cheeky $200 to your American online brokerage from your French bank account to bet on some oil commodities. Right now it would cost almost peanuts to send it. But in the future that $200 will be converted to tire currency and then count as part of your Thai income and then be sent to the American account.

From linked site:

-

1

-

-

3 hours ago, Everyman said: I never saw the point of the Wise card anyway,

We've gone from a situation of famine of 15 years ago where there really was a lack of choices for expats who wanted a Visa or MasterCard (to pay online purchases like Agoda etc) unless they were prepared to pay for premium credit cards, to the situation today, where we are absolutely saturated with debit cards using Visa, MasterCard etc.

Any standard debit card now issued from a Thai bank is always linked to Visa, Mastercard or UnionPay etc.

15 years ago I only had the famous Kasikorn "web shopping card" as the way to make Visa or MasterCard payments. Now I have everything from a crypto card to a global money/journey card to a UnionPay card.

-

7 hours ago, Everyman said: Please don’t use AI for things like this.

I only used the AI for the tax revenue modeling. I had it present the calculations so I could check.

Obviously AI cannot be reliably used for researching these changes, but in the last year, certain AI models have massively improved with pure maths calculations.

The only factor that matters to show huge cost implications are the assumption that there is a tax remittance when a conversion to Thai baht is made in the Wise system. This is my assumption. It is unconnected with AI.

Obviously, Wise will not provide tax advice so they will not say if there is a tax implication, and I'm sure the Thai tax revenue lawyers are now licking their lips to argue about this.

The entire spirit of my original post remains valid. You are free to do the calculations yourself, even using an old-fashioned Excel spreadsheet if you want.

-

- Popular Post

This is absolutely terrible news. I'm making two reasonable assumptions: Wise users will no longer be allowed to directly transfer into and out of multiple currency accounts, and any money placed into Wise will count as a remittance under Thai income tax laws. Frustratingly, the linked page does not clearly state this but it is implied with everything else they write.

None of this will be relevant to pensioners simply transferring income to Thailand or people with simple lifestyles occasionally transferring money outside of Thailand. I'm talking to people who have global financial interests.

Most expats with serious funds will follow the standard practice of A to B to C: citizenship of A, bank savings/investments in B, living in C. This minimises tax implications.

One of the major functions of Wise is to act as a global bridging mechanism. That is, to move money from A to B or from B to A using local access accounts. But with these changes it appears that Wise will force the money to go via C (since the auto-conversion to Thai baht is likely to count as a remittance in law), creating a huge tax liability and creating a double conversion charge.

You might suggest that the expat should simply use a competitor to Wise such as TorFX. But that will not work because most financial institutions require that your money is withdrawn to an account in your name. And for whatever reason only the "virtual" accounts of Wise are accepted (e.g. it is currently remarkably easy to set up a Singapore bank account with Wise, which is widely recognised by financial institutions). Other competitors do have virtual accounts which you can open various countries but they are simply not recognised by the financial institutions.

Running various scenarios through Gemini AI, I found the cost implications to this Wise change to be unbelievable. I strongly recommend others in this position take a look. Not only will you be charged for a double conversion of the money but you will also be hit with an income tax bill on it (30%+ of the sum transferred?).

There are no viable FinTech alternatives to Wise for these global bridging mechanisms. I think the only choice is to open a premier/priority bank account such as with HSBC or Standard Chartered or Citibank etc.

I'm interested to hear how other people are handling this.

(I think for the basic user of Thai resident Wise the access to a wise card and being able to transfer out of Thailand will be mostly beneficial.)

-

1

-

1

-

1

-

Just here to report that Chaeng Wattana (Bangkok) continues to not allow reporting online for the first 90 days report after returning from abroad.

-

1

-

-

I strongly suspected that radiologists would be the first specialist doctors to lose their jobs to AI. It is just a matter of time before AI hits the 97/98% mark in detection. At first there will be resistance, but the economic case is absolutely overwhelming.

The annihilation of middle-class jobs has just begun.

-

-

-

12 hours ago, youreavinalaff said: There most certainly was

There most certainly wasn't.

I suspect in your case, the parent was not a British citizen by descent but a British citizen born within the UK, or fully naturalized etc. "By descent" has a meaning not obvious and requires a reading of the law.

I strongly suspect you don't understand this key point and because of that on three occasions now you have failed to grasp the legal position pre-2006.

-

Upcoming changes to Wise operations in Thailand

in Jobs, Economy, Banking, Business, Investments

In fact that is not the case. They will encourage you to invest into shares or mutual funds or ETFs or bonds on their platform since they will want the commission.

And if you don't want to invest, they typically offer multiple currency accounts (normally around 15 currencies are automatically opened for you) so you can simply tactically slot your money into a high interest currency.

You might also want to leave a bit of money to be "frozen" (around $10,000) so that you can be given a free, extremely desirable credit card with infinite lounge access etc. That's not my thing but I know it is on offer.

They don't actually require money to sit in the account but simply require that you have in total enough across their various products. They will add that all together every three or four months to make sure you have enough. They will provide some leeway if it goes a bit below for a time. If it does go a bit below they typically charge about 10 or $15 a month. There could be a problem if there is a major share collapse etc.

Make sure when you open it you mention the freebies offer (just check on their websites for their latest cash giveaways etc). Free money is free money after all.