.png.3b3332cc2256ad0edbc2fe9404feeef0.png)

tomkenet

-

Posts

94 -

Joined

-

Last visited

Content Type

Profiles

Forums

Downloads

Everything posted by tomkenet

-

Not only in the past, also income received this year, 2023 which will be the last year this loophole can be used.

-

Not according to: Ernst & Young: This provision aims to limit the scope of foreign-sourced income subject to Thai personal income tax and exempts income earned before 1 January 2024. As per Paw.162 instruction, only foreign-sourced income earned from 1 January 2024 onwards, and the individual having been a Thai tax resident in the year of earning, would be subject to Thai personal income tax in the year whenever it is brought into Thailand. Mazars: shall not apply to any foreign sourced income earned by Thai tax residents before 1 January 2024. Thai tax residents will not be required to include their foreign sourced income earned before 1 January 2024 in their personal income tax returns, even if such income will be brought into Thailand from 1 January 2024 onwards. Baker McKenzie: The new order does not apply to foreign sourced income received by a Thai tax resident before 1 January 2024.

-

I know it can be a problem to open an account in a new bank, but if you are an old customer from before you emigrated, and you have a TIN from Thailand it should not be a problem if you have maintained the relationship with your bank well.

-

Exactly my Strategy too

-

Thank you for a very interesting post. It seems like many people have not read or understood these important updates: Ernst & Young: This provision aims to limit the scope of foreign-sourced income subject to Thai personal income tax and exempts income earned before 1 January 2024. As per Paw.162 instruction, only foreign-sourced income earned from 1 January 2024 onwards, and the individual having been a Thai tax resident in the year of earning, would be subject to Thai personal income tax in the year whenever it is brought into Thailand. Mazars: shall not apply to any foreign sourced income earned by Thai tax residents before 1 January 2024. Thai tax residents will not be required to include their foreign sourced income earned before 1 January 2024 in their personal income tax returns, even if such income will be brought into Thailand from 1 January 2024 onwards. Baker McKenzie: The new order does not apply to foreign sourced income received by a Thai tax resident before 1 January 2024.

-

Illegal tax evasion but difficult to discover. RD might question his livelihood, does he work illegally in Thailand

-

Yes, and presumably this obvious for most people.

-

So far it is only the remittance of income to Thailand that is taxed.

-

NOT if you have unrealized, potential capital gains . If realized after 2023, they will be taxed if remitted. That's why it's recommended to realize them before 2024

-

I would keep those money on separate accounts only used for remittance to Thailand, trackable back to before 2024. No new deposits to these accounts except interests, which might be taxable. If and when Thailand introduces worldwide taxation in the future, new strategies must be obtained.

-

This article is from before Por.162/2566 would be much more interesting with an update after.

-

I thought departmental Instruction No. Paw.162 ("DI Paw. 162" ) was issued 20 November 2023.

-

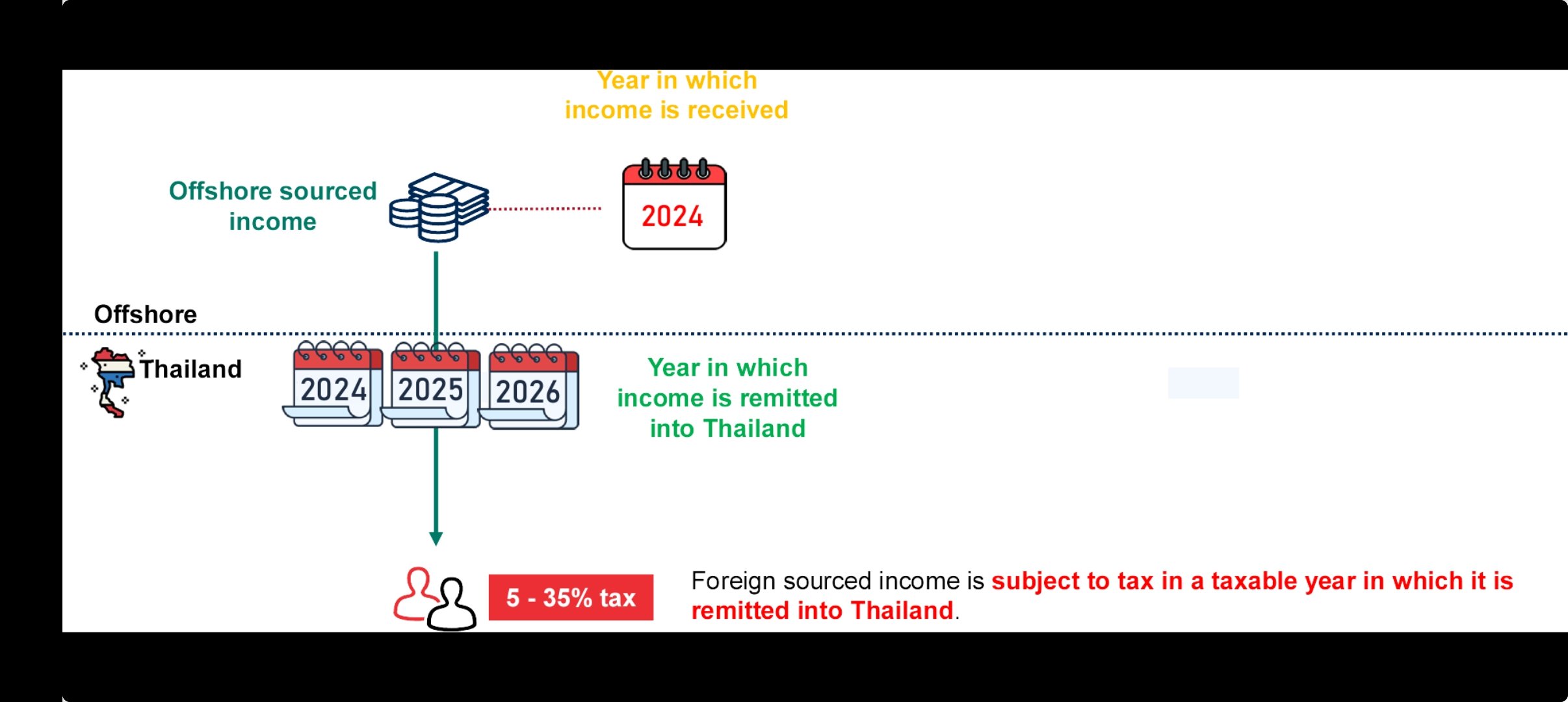

From the same Baker McKenzie report, "Foreign sourced income is subject to tax in a taxable year in which it is remitted into Thailand."

-

So how do you interpretate Baker MacKenzie clarification about the text "Tax residency status in the year of remittance is irrelevant." "Thai personal income tax is based on cash basis - receiving income. A year in which a person receives offshore income is relevant, saying that it must be a year that the person is a Thai tax resident. Whether that person is a Thai tax resident in a year in which he or she actually brings income into Thailand is not relevant."

-

Does this mean a person can be taxed on remittance even he is not a tax resident that year if the money is earned a previous year when he was a tax resident.

-

So what you're saying: A person who is not a tax resident (but was a previous year) will have to file a tax report showing the origin of the funds he remitted to Thailand the year he is not tax resident. Sounds unlikely.

-

Google "tax resident of nowhere"

-

I have to disagree, I have received a lot of useful information from this thread . We might not know what the government will finally do, the government probably don't know itself, but we know pretty well what will happen in the meantime.

-

That's exactly my point too, I believe Grumpy is wrong here.

-

Remittance in 2023 of income earned in 2023 is certainly taxable. It you wait until beginning of 2024 it will not be taxable. Thats at least my understanding.

-

What if Mr A has a savings account from before 2024 holding 16000 thb. The interest is 1000 thb a year, so in 2026 the account holds 18.000 thb. He remits this 16.000 thb from the savings account to Thailand in 2026. (Not from the account that holds the 16.000 capital gains from 2025) What is taxable income for the year 2026? 0 thb 2.000thb or 16.000 thb

-

I think the numbers Mazars uses are too low to make sense , but remember this are just examples to show the principle. Add a zero or to to the numbers to make them more realistic.

-

Not sure if this document has been posted here before. https://www.mazars.co.th/mazarspage/download/1175616/59807824/file/Technical-update-November-2023.pdf Quite interesting What if Mr A has a savings account from before 2024 holding 16000 thb. He remits this money, instead of capital gain money realised from selling 80 shares in 2025, to Thailand in 2026. Still taxable for the year 2026?

-

I believe there is no time limit to when you can transfer that money as long as you have documents showing them originating from prior 2024. Interest on the account might however be subject to tax.

-

If you have used the loophole, transferring overseas income the year after, to save tax, it will affect you.