tomkenet

-

Posts

134 -

Joined

-

Last visited

Content Type

Events

Forums

Downloads

Quizzes

Gallery

Blogs

Everything posted by tomkenet

-

This article is from before Por.162/2566 would be much more interesting with an update after.

-

I thought departmental Instruction No. Paw.162 ("DI Paw. 162" ) was issued 20 November 2023.

-

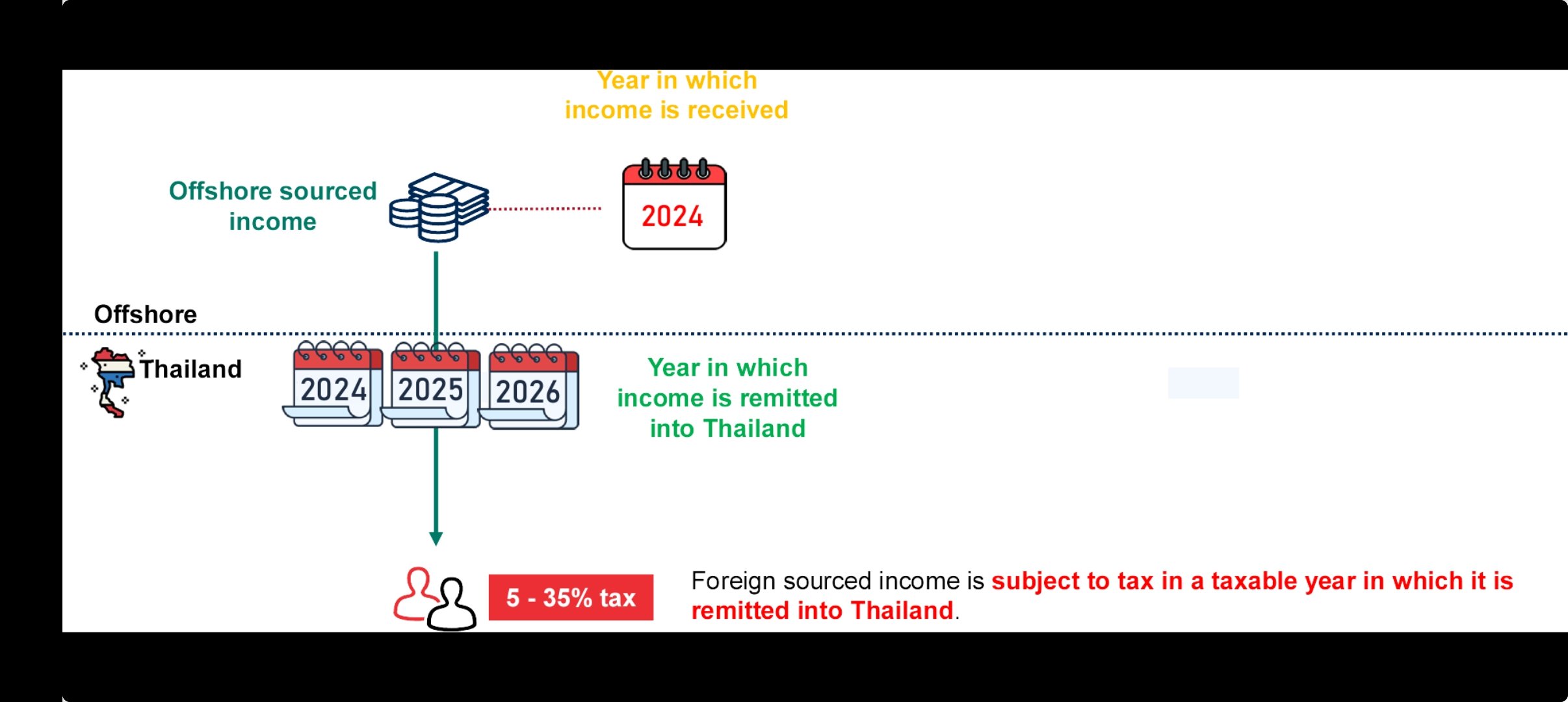

From the same Baker McKenzie report, "Foreign sourced income is subject to tax in a taxable year in which it is remitted into Thailand."

-

So how do you interpretate Baker MacKenzie clarification about the text "Tax residency status in the year of remittance is irrelevant." "Thai personal income tax is based on cash basis - receiving income. A year in which a person receives offshore income is relevant, saying that it must be a year that the person is a Thai tax resident. Whether that person is a Thai tax resident in a year in which he or she actually brings income into Thailand is not relevant."

-

Does this mean a person can be taxed on remittance even he is not a tax resident that year if the money is earned a previous year when he was a tax resident.

-

So what you're saying: A person who is not a tax resident (but was a previous year) will have to file a tax report showing the origin of the funds he remitted to Thailand the year he is not tax resident. Sounds unlikely.

-

Google "tax resident of nowhere"

-

I have to disagree, I have received a lot of useful information from this thread . We might not know what the government will finally do, the government probably don't know itself, but we know pretty well what will happen in the meantime.

-

That's exactly my point too, I believe Grumpy is wrong here.

-

Remittance in 2023 of income earned in 2023 is certainly taxable. It you wait until beginning of 2024 it will not be taxable. Thats at least my understanding.

-

What if Mr A has a savings account from before 2024 holding 16000 thb. The interest is 1000 thb a year, so in 2026 the account holds 18.000 thb. He remits this 16.000 thb from the savings account to Thailand in 2026. (Not from the account that holds the 16.000 capital gains from 2025) What is taxable income for the year 2026? 0 thb 2.000thb or 16.000 thb

-

I think the numbers Mazars uses are too low to make sense , but remember this are just examples to show the principle. Add a zero or to to the numbers to make them more realistic.

-

Not sure if this document has been posted here before. https://www.mazars.co.th/mazarspage/download/1175616/59807824/file/Technical-update-November-2023.pdf Quite interesting What if Mr A has a savings account from before 2024 holding 16000 thb. He remits this money, instead of capital gain money realised from selling 80 shares in 2025, to Thailand in 2026. Still taxable for the year 2026?

-

I believe there is no time limit to when you can transfer that money as long as you have documents showing them originating from prior 2024. Interest on the account might however be subject to tax.

-

If you have used the loophole, transferring overseas income the year after, to save tax, it will affect you.

-

More from Mazars "Taxpayers with foreign-sourced income, which has yet to be realised, should consider realising income or gains before the end of this year so that such foreign-sourced income will not be taxable if remitted into Thailand on or after 1 January 2024." I guess these money have to be kept in separate accounts for them traceable back to 2023 when remitted , not to be mixed with income after 2023.

-

How would any other interpretation make sense.

-

How would any other interpretation make sense.

-

The text from sherring is a bit confusing, but if you compare to this link that was posted earlier it makes more sense. https://www.prachachat.net/finance/news-1432180 However, recently there was a report from the Revenue Department that It has been concluded that In the first phase, there will be relief in the case of income generated abroad before 2024, if it is not imported within the same tax year as the year in which the income was generated. It will not have to be checked.

-

För stocks the best way might be to sell in 23, then buy them back. The profit will then be tax-free in addition to the principal.

-

The capital gain is normally booked when the asset is sold. I do not think you can claim profit prior to 2024 if the asset is sold later.

-

Can it now be concluded that LTR visa holders are tax exempt for foreign capital income like interests, capital gains and dividends remitted to Thailand the same year they are earned? What happens next year is of course another question.

-

Will there be a problem moving out of Thailand for 7 months, remit to Thailand that year necessary funds for several years forward. Then live tax free for those years.

-

For us married guys. What about the wife gets an overseas bank account. You both remit half of your needs. Should reduce the tax significantly to share the income 50/50

-

Malaysia sounds much better than Laos and Cambodia, but mm2h visa has become expensive. It might change I've heard. Do you know how overseas income (not taxed at source) is taxed in Malaysia.