tomkenet

-

Posts

134 -

Joined

-

Last visited

Content Type

Events

Forums

Downloads

Quizzes

Gallery

Blogs

Everything posted by tomkenet

-

Hope you earned this before 2023. If earned in 2023 it is taxable. If earned in 2023 and remitted in 2024 it would be tax-free, just like it has always been when remitted the year after earned. This however changes for money earned in 2024.

-

2024 will be just like previous years. Last years earnings will not be taxable when remitted. 2025 will be the first year with the new rules. Last year earnings will be taxable when remitted.

-

paw 162 is logical, it is just previous loophole continued for the rest of current year. Not applying Paw 162 would be for Paw 161 to be retroactive from 1 January 2023.

-

I wonder if this deduction also can be used for foreign sourced dividends or capital gains remitted to Thailand

-

I am in the same prosess. My guess, you'll have to show documentation if they ask, which they probably will not.

-

2024 will be just like previous years. Last years earnings will not be taxable when remitted. 2025 will be the first year with the new rules. Last year earnings will be taxable when remitted.

-

Is there any doubt Paw 162 will not be applied? It is actually quite logical, it is just previous loophole continued for the rest of current year. Not applying Paw 162 would be for Paw 161 to be retroactive from 1 January 2023.

-

What I need is a certificate of residency for tax purposes. R.O.22. I think it is not the same thing

-

That is right and a good idea. I will try to do that, however, if it is not possible, with deductions it will end up in a very low tax bracket. I have to file tax report anyway to get the certificate of residency.

-

My plan is prior to 2024 deposit in a savings account back home money to last for 3-4 years in Thailand. Let's call this money X which can be remitted taxfree. My other investments will after 2023 continue to generate income that is not taxed. Let's call this money Y. As far as i understand I will be developing a sort of tax debt on this money, generating tax when later remitted. In 3-4 years, when X is depleted I will have a big incentive to move to another country where Y will be considered taxfree savings. I wonder how long I would have to stay away from Thailand for this taxdebt to go away. Another outcome is by that time Thailand has changed to Worldwide taxation (not remittance) , what would then happen to Y.

-

I am very curious how Thai RD is going to make this system work A tax resident foreigner holding a foreign account with income and savings from before 2024, proceeds with capital gains, dividends and pension etc. from after 2023, and proceeds with capital losses from after 2023. All mixed together in 1 account. Can the taxpayer choose which money he remits to Thailand or is it FiFo. And how to sort out what money has already been remitted and what money is not yet remitted the following years. This system might work for Thai citizens with limited economic activity outside Thailand, but for a foreigner with most of his economic activity outside Thailand this is very messy

-

Sounds like a good plan. I will do something similar,but with a overweight of transferring money to a Ring fenced account before new year.

-

Looks like this one is from before. Paw. 162/2566 They have also issued a report after, which is more useful.

-

It's from the Baker McKenzie report. It has been referred to several times on this thread, surprised you haven't seen it . Mazars and Ernst & Young reports the same interpretation

-

Not only in the past, also income received this year, 2023 which will be the last year this loophole can be used.

-

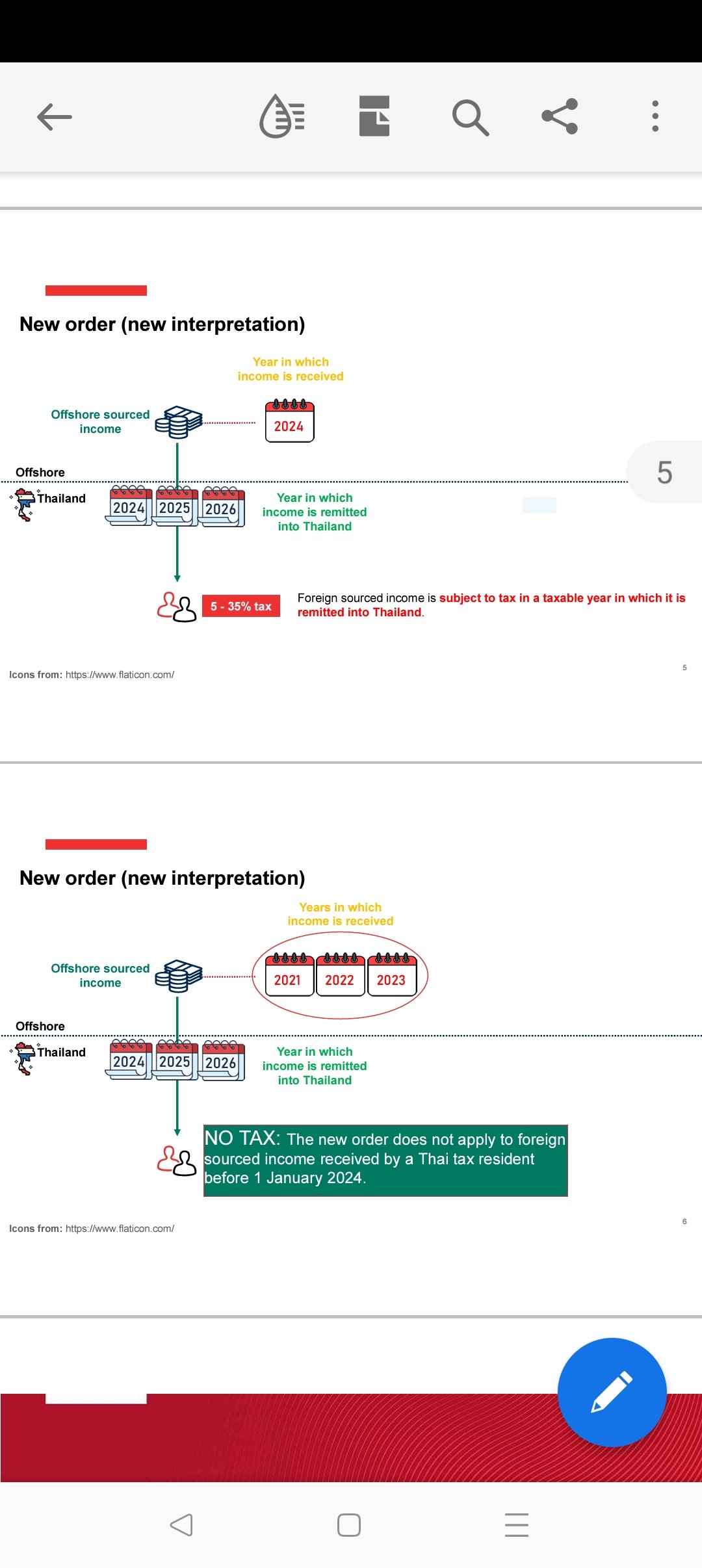

Not according to: Ernst & Young: This provision aims to limit the scope of foreign-sourced income subject to Thai personal income tax and exempts income earned before 1 January 2024. As per Paw.162 instruction, only foreign-sourced income earned from 1 January 2024 onwards, and the individual having been a Thai tax resident in the year of earning, would be subject to Thai personal income tax in the year whenever it is brought into Thailand. Mazars: shall not apply to any foreign sourced income earned by Thai tax residents before 1 January 2024. Thai tax residents will not be required to include their foreign sourced income earned before 1 January 2024 in their personal income tax returns, even if such income will be brought into Thailand from 1 January 2024 onwards. Baker McKenzie: The new order does not apply to foreign sourced income received by a Thai tax resident before 1 January 2024.

-

I know it can be a problem to open an account in a new bank, but if you are an old customer from before you emigrated, and you have a TIN from Thailand it should not be a problem if you have maintained the relationship with your bank well.

-

Exactly my Strategy too

-

Thank you for a very interesting post. It seems like many people have not read or understood these important updates: Ernst & Young: This provision aims to limit the scope of foreign-sourced income subject to Thai personal income tax and exempts income earned before 1 January 2024. As per Paw.162 instruction, only foreign-sourced income earned from 1 January 2024 onwards, and the individual having been a Thai tax resident in the year of earning, would be subject to Thai personal income tax in the year whenever it is brought into Thailand. Mazars: shall not apply to any foreign sourced income earned by Thai tax residents before 1 January 2024. Thai tax residents will not be required to include their foreign sourced income earned before 1 January 2024 in their personal income tax returns, even if such income will be brought into Thailand from 1 January 2024 onwards. Baker McKenzie: The new order does not apply to foreign sourced income received by a Thai tax resident before 1 January 2024.

-

Illegal tax evasion but difficult to discover. RD might question his livelihood, does he work illegally in Thailand

-

Yes, and presumably this obvious for most people.

-

So far it is only the remittance of income to Thailand that is taxed.

-

NOT if you have unrealized, potential capital gains . If realized after 2023, they will be taxed if remitted. That's why it's recommended to realize them before 2024

-

I would keep those money on separate accounts only used for remittance to Thailand, trackable back to before 2024. No new deposits to these accounts except interests, which might be taxable. If and when Thailand introduces worldwide taxation in the future, new strategies must be obtained.