lkn

-

Posts

1,747 -

Joined

-

Last visited

Content Type

Events

Forums

Downloads

Quizzes

Gallery

Blogs

Everything posted by lkn

-

And? I don’t get your point at all. Banks often add 1-2% to the VISA/MasterCard exchange rate when used abroad, and for cards issued within the EU, they are not limited by EU’s cap on interchange fees when used outside the EU. So regardless of credit or debit card, banks often make an extra cut of the spending when used abroad, and it makes no sense to me why a bank would want to freeze a card for other reasons than suspected fraud.

-

That’s just crazy — I have heard of cards being frozen because the bank thought it was fraud, but they shouldn’t deny their customers to use the card abroad, on the contrary, many banks will make extra fees from this. As for Revolut and Wise, they are basically designed to be used away from home.

-

Thai Airways: 10 kg extra checked baggage for silver members?

lkn replied to lkn's topic in Thailand Travel Forum

OK, think the log in is the issue, there is a profile icon “top left”, but it is partly in the status bar and does not register my clicks. Apple changed the screen metrics some years ago, and apps that hasn’t been updated tend to have things end up in non-clickable areas of the status bar 😞 Amazing that the app has a 4.0 rating on the iOS app store, because it is practically useless, with many buttons not working, I even got into a screen where I had to force quit because the “back” button was inaccessible. This, and half the screens are just taking you to a web page, not even remembering my cookie consent choice from last time, or suppressing the “install the app” banner at the top. -

Thai Airways: 10 kg extra checked baggage for silver members?

lkn replied to lkn's topic in Thailand Travel Forum

Are you talking about this app (iOS)? I can click “More” and then ROP, but that just opens a web browser. The app seems extremely limited, most things just open web pages that each have cookie consent forms and a banner at the top about downloading the Thai Airways app, and it seems the app has not been updated for the dynamic island, so controls (like back) is often un-clickable. Couldn’t find a way to really “log in” in the app, nor show my member card or anything like that. -

Thai Airways: 10 kg extra checked baggage for silver members?

lkn replied to lkn's topic in Thailand Travel Forum

Someone else is migrating to Thailand and I offered to help carry their stuff. -

Crappy rate and foreign exchange fee is not really solved by opening a bank account. I believe most people use Wise for exchanging money to get the best rate, they have a debit card which you can use in Thailand. So it really boils down to the ATM fee. I’m surprised though that no-one has brought up PromptPay, I think that is actually a better reason; if you want t go cashless in Thailand, you need a bank account that support QR payments, as VISA/MasterCard is normally not accepted by smaller/street vendors.

-

I hate fees as much as the next guy, but on a vacation budget, 220 baht a few times is really not that much, and it is not like Thailand is an outlier, pretty much all countries put in place hurdles for foreigners to open a bank account. They do this not only because there are actually expenses for the bank to open an account, but also because of AML/KYC. Having tourists walk in from the street with nothing but a passport and allow them to open a bank account is definitely going to be abused. Many of the operations scamming U.S. and Canadian citizens (romance scams, fake tech support, etc.) actually use Thai bank accounts (in addition to gift cards, bitcoins, and local money mules). I imagine it’s a headache for the bank each time such an account gets flagged, and that is probably why they want you to show a work permit, one year lease, or similar, as just a very basic KYC check.

-

I have been a Thai Airways Silver Member for the last 10 or so years, so today I decided to look up if there is actually any benefits. Lo and behold Royal Orchid Plus Silver Members can check in extra 10 kg of baggage. I am flying in from Europe on Royal Silk on Monday and I actually could use 50 kg of checked baggage, but unfortunately my country’s Thai Airways office is closed during the weekend, so I can’t call them for confirmation. So before I pack 50 kg of baggage I just wanted to ask here, if someone has taken advantage of this benefit? Because my ticket only says 40 kg even though it includes my frequent flyer/ROP number, but presumably that is just because they are using archaic ticketing systems. I also remember I got a Thai Airways member card long ago, but I have since thrown it out, as I am quite sure it was expired. I wonder if the clerk needs to see some sort of documentation for my silver member status when checking in? Again, with their archaic ticketing systems, that information might not be accessible to them from the check-in counter.

-

A purchase agreement was among the documents listed as valid reason for a bank account.

-

The alternative to a Thai bank is just your own bank or Wise, no need to withdraw your entire net worth and put in the hotel safe. Yes, the ATM fee does suck, but if you’re in Thailand for 1-2 months, how many times do you really need to go to the ATM? Consider OTOH the expenses the bank will have when opening your free basic savings account that you only plan to use for a few months without buying any of their add-on products or services. I recently spent two months in Japan myself, it never occurred to me that I should open a local bank account to avoid the 220 JPY ATM fee.

-

I’ve long tried to get my ex to build a brick mansion in her hometown, I think it would be hilarious, but she is not convinced. Though if you are serious, consider what you actually need. For most people, a mansion is impractical, but you can still do cool stuff, I am personally into spa-style ensuite/open bathrooms connected with the master bedroom, think about your “flow” in the house and optimize the layout for that, do specialized built-in furniture for the things you need, e.g. you probably have bottled water that needs to be stored somewhere, etc. But also remember that construction quality here is poor, so anything out of the ordinary, and your workers may do a crappy job unless you get top talent. Though it is unclear if your goal is to build your dream house, or your idea of a rich man’s dream house.

-

This is a combination of lousy interface and implementation, for example just opening the KTB app can take upwards of 10 seconds, and then you often have to click through a splash screen before you can activate the scanner. Look instead at how contactless/NFC payments work, this is much much easier and faster. Although here it may also depend on the store, for example in Europe you can mostly just tap the terminal with your phone/watch/fitness tracker the instant the total amount shows on the cash register, and the reader is near instant, but in some supermarkets in Thailand you have to explain you want to pay by card and it takes them a minute or so to “prepare the reader”.

-

I did this myself by writing my bank. It’s a standard product that every bank offers here. It was then the buyer’s agent who informed my bank that they could release the funds.

-

In the case of a wallet app (e.g. Apple or Google Pay), what kind of hacking are you talking about? I.e. is this a case of “someone can see your unlock code, steel your phone, and then spend money via your phone’s wallet app”? In which case, cash has a similar problem (someone can steel it). Or are you talking about an attack against the actual contactless payment protocol? If so, are you aware of any proof-of-concept demonstrations?

-

I sold my condo back home while in Thailand. The process was as follows: My bank created an escrow account in my name Buyer transferred amount to this escrow account I signed over the title deed to the buyer using our digital signature system Buyer got keys from real estate agent and after a few days gave the OK to my bank to release the money I think the delay in the last step was mainly for the new owner to get utilities and such transferred into their name, and making sure there weren’t unpaid bills. Though during this step, the money in escrow was visible to me (through internet banking), I just couldn’t withdraw from that account before buyer gave the green light.

-

Looking here https://www.ddproperty.com/en/agent-directory/chiang-mai I see 183 agents for Chiang Mai, and that’s only those who have an affiliation with DDProperty.

-

I am considering selling my penthouse and wondering what agency to go with. It seems the system in Thailand is that the agent gets 3% so one unit might be listed at many different sites, as the incentive is for the agent to just try to get commission on whatever is for sale in the area — similar to the mall where there will always be a sales person watching you like a hawk, and interjecting themselves into the sale, to get their commission, but I digress… So my question is: Is there any agency in Chiang Mai that stands out? I guess what this means is having the broadest reach and getting the unit listed on all those aggregation sites. My unit is in the higher end of the price range (~95K per sq.m.) so I am probably looking for an agent that mainly targets foreigners. For this, Expat Homes would, based on the name, sound like the obvious choice, but I see they only list two units in Chiang Mai (city), that makes me wonder if they are still active? I also found Lazudi which have a lot of high-end properties for sale, but it seems to be more of a listing site with agents signing up for different areas, so their focus is probably on having the largest database, but do they actually have the corresponding traffic to their site to make it worth listing with them? Curious to hear your experience (selling) a condo in Chiang Mai. And no need to informing me how hard it is to sell real estate in Thailand, that information has already been given to me.

-

Pretty much all jobs I can find for unskilled workers in Thailand pay 9-13,000 baht/month, where the higher end of that range is with overtime. Trying to help a friend, what would be your advice? More education has sort of been ruled out, so I am thinking maybe work where you learn on the job, so at least there is a path to higher pay, even if the starting salary is still low. In my own country, construction would be a good candidate, but from what I have seen in Thailand, there seems to be little interest in specialized construction workers, rather, many of the construction workers I have met was underpaid migrant workers.

-

How do I pay my electricity bill online?

lkn replied to mrjohn's topic in Jobs, Economy, Banking, Business, Investments

I don’t think 7-Eleven accepts Rabbit Pay. As per the image below, they accept TrueWallet because both 7-Eleven and TrueMoney are subsidiaries of the Charoen Pokphand Group. This also seems to be why they do not accept Thai debit cards, even though they do take international cards, and I believe there is one bank in Thailand which cards you can use, because it is also a subsidiary or partner of the CP Group. I personally use my Wise VISA card via ApplePay in 7-Eleven for cashless and contactless payments. It’s a bit ridiculous though, that they do not accept PromptPay or Thai debit cards…

-

How do I pay my electricity bill online?

lkn replied to mrjohn's topic in Jobs, Economy, Banking, Business, Investments

Your bank should have this form, so just go to your bank with your latest bill and they will fill out the form for you, and you then deliver it to your nearest PEA office. At least that is what I did, once with Krungthai and once with Kasikorn. -

By remote work, I assume you’re sitting in your condo in front of a computer? I don’t see how anyone in the immigration or labour department would find out about this. Even if you have a bad breakup, what sort of actionable intel can your ex really give the authorities? I know of plenty of people who work online here, but it would be near impossible for me to prove it, even searching their laptops would not necessarily make it clear that work was done while they were in Thailand.

-

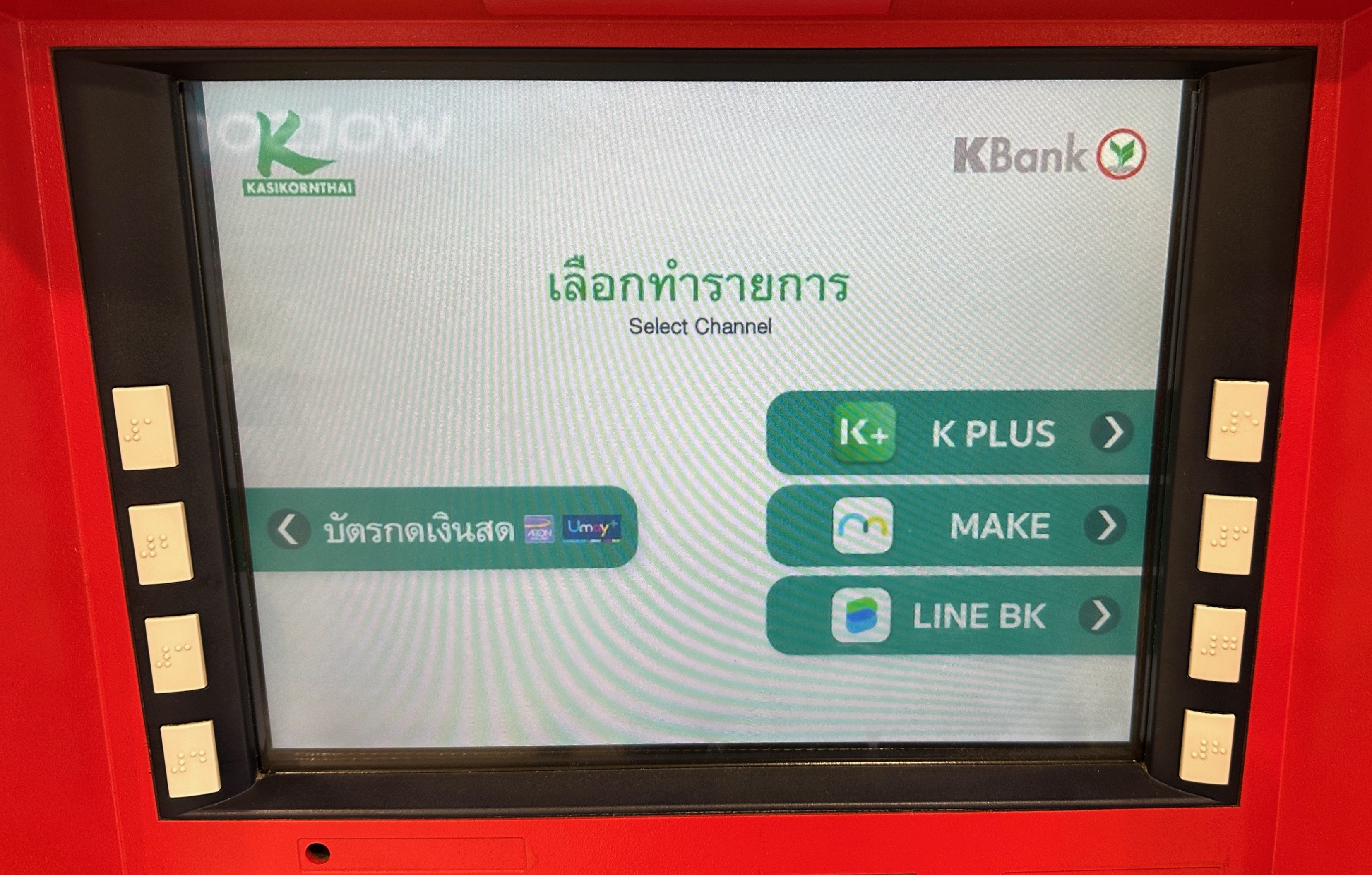

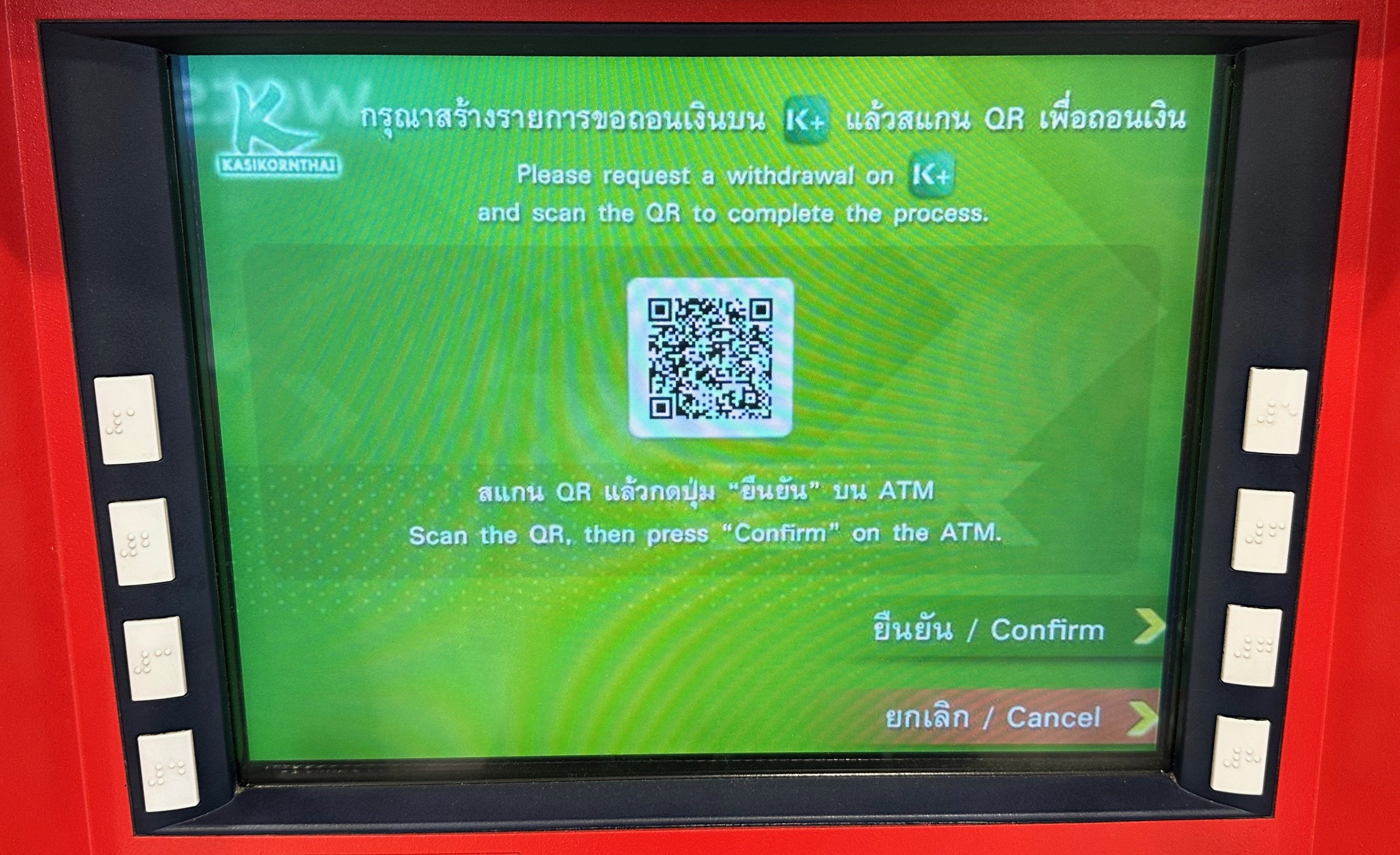

On the ATM screen there is a button to select “Cardless withdrawal” after which you are asked to select channel and then to scan the QR code (using K+), coincidentally I have photos of the two screens:

-

[…] bank reserve right to charge full card fee of THB 380 for another 3 years card usage. So it is 380 baht every 3rd year (as long as the card is valid), and 100 baht issue fee. Presumably you are on an older scheme, though on their pricing page they do actually show some cards that are no longer issued (one with no fee), but not any with payment only every 5th year. How much do you pay every 5th year?

-

No issue fee, and no fee the first year. After that, 150 baht/year. As I just wrote above, I do wonder if one can just cancel after 11 months and then create a new card, should work with their current pricing scheme.

-

The 300 baht probably includes first year issue fee. Though for your card, the cheapest card I see for Krungsri is ~127 baht/year (380 baht every 3rd year) plus issue fee: https://www.krungsri.com/en/personal/card/krungsri-debit-card/all-atms Personally though, I’ve switched to virtual cards, it’s cheaper, but also more convenient, as I don’t need to go to a branch, when they expire. Though I see Kasikorn will start to charge 150 baht/year after first year. I do wonder if I can just cancel the card, and then create a new one, to get another year’s worth of free usage…