Mike Teavee

-

Posts

4,306 -

Joined

-

Last visited

Content Type

Events

Forums

Downloads

Quizzes

Gallery

Blogs

Everything posted by Mike Teavee

-

Not a misunderstanding more of a divergence in what the Sherrings statement is saying, to me it is only referring to the way the Gain is calculated & makes no reference to how the proceeds are remitted which I believe is pro-rata. Time will tell but in the meantime I won't be remitting any Capital Gains to Thailand until the position is crystal clear, same with Rental & Dividend income. I wonder if Thailand has any idea how much money isn't being remitted because of the lack of clarity around this (I'm only remitting 235K for me & 210K for the GF this year & next, when normally it would be 4X that pa) or how many people are putting of large purchases (which is ironic given the very recent push to increase foreign ownership of condos / leased land).

-

That simply means it's up to you to decide whether income you're remitting is assessable or not. In the context of the CGT debate you may assess that the money you're bringing over is the original income so is not assessable, I believe you're wrong & part of it is assessable but it would only matter if TRD ever audited you.

-

No it wouldn't, FIFO would mean the oldest assets I own are sold first & then I'm taxed on the gain on those... E.g. £20,000 made up of:- 5,000 shares at £1 2,500 shares at £2 1,250 shares at £4 Lets say those shares are now worth £5.... FIFO means I sell 2,000 of the 1st tranche at £5 = £10,000 for a gain (excluding costs / taper relief etc...) of £8,000 LIFO means I sell 1,250 from the 3rd Tranche at £5 (realising £6,250 for a profit of £1,250) & 750 from my 2nd tranche (realising £3,750 for a net profit £2,250) Total profit = £3,500. Edit: Apologies if any of the maths is off but the GF is nagging to go out for dinner, hopefully people will understand the point I'm trying to make.

-

I’ve replied to that point above, Sherrings/TRD have made no comment about the remittance of Capital Gains. Here’s the 2nd video (CGT is around the 16 minute mark)

-

As mentioned it featured in 2 Expat Tax Video Q&A sessions, Mike L has linked to one of them above.

-

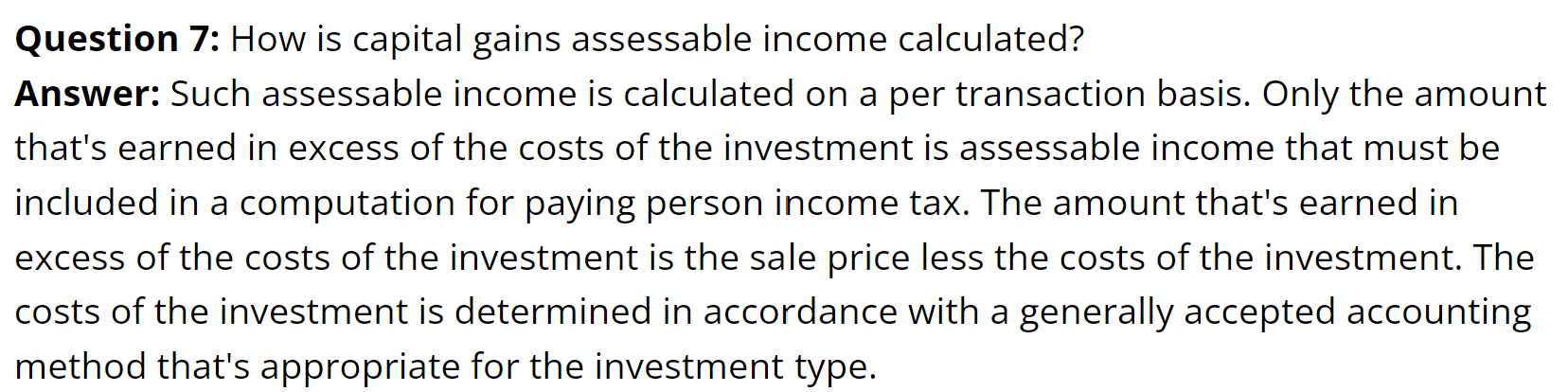

Thanks but.... ... Does not say anything about LIFO/FIFO accounting methods used when remitting the money, it just says "The cost of the Investment is determined in accordance with a generally accepted accounting method that's appropriate for the Investment Type" which only impacts the Capital Gain calculation, not what happens when that money is remitted. E.g. I buy some stock for a total of £20,000 & using FIFO rules, sell £10,000 of it making £2,500 profit on that tranche so my Investment to Gain ratio is 80:20, I remit £5,000 to Thailand and £4000 is investment, £1,000 is Gain. However, if I'm told to use LIFO I might only make £1,000 profit so my Investment to Gain ratio is approx. 90:10, I remit £5,000 to Thailand and £4,500 is Investment, £500 is Gain. Neither of those examples lets me remit £5,000 and claim it all came out of the original investments pool.

-

I haven't seen a statement from Sherrings saying that so would appreciate a link to it. The Expat Tax Video Q&A sessions (freely available on YouTube & posted already on this thread) clearly stated their opinion that any remittances which included a Capital Gains element would be pro-rated based on the ratio of Investment to Gain. If they are correct then repeating the example from earlier, an investment of £10,000 realising a £2,500 gain, would give a ratio of 80:20 Investment:Gain so remit £5000, £4000 would be Investment & £1,000 would be gain.

-

LIFO = "Last In First Out" which surely means the principle comes out last as the "Last In" would be Gains/Interest

-

I take it a "CD" is a "Certificate of Deposit" & not a "Contract for Difference" (Which is what we call CDs, in the finance sense, in the UK), isn't that just a Fixed Term Deposit account & so the original capital invested (and any interest earned) in 2023 is free from Thai Tax whereas any interest earned after 1/1/2024 could be liable to Thai Tax assuming it wasn't covered by a DTA (And in the case of US I'm pretty sure it will be covered, your DTA is much more comprehensive than other countries DTAs).

-

Can you point to anything (even an unofficial source) that agrees with you when it comes to Capital Gains being re-baselined as at 31/12/2023. I asked this question more or less when this whole thing started & whilst we've not had a definitive statement from TRD, the view of most people on the board (& the Expat Tax consultants) was that the Gain is calculated based on the original cost of purchasing the asset as it is in the majority of countries/cases. I also asked the question what would happen if instead of remitting the Capital Gain, you used it to purchase a new asset & sold it soon after which (given dealing costs/spread) would probably result in a small Capital loss. Again no definitive answer from TRD but consensus seemed to be you might be pushing your luck with them on large transfers & if they choose to dig deeper into you finances could decide the money used to purchase the last asset included the Capital Gains.

-

The root domain has a .TH (Thailand) Suffix, I don't know what the "IN" indicates but you would expect an official Government website to have a ".GO.TH" suffix. Sites like this can be useful for keeping an eye out for updates as they tend to be updated very quickly when new information comes out, but shouldn't be used to make any concrete plans from until you see it on an official site. Edit: The .in.th is the internet country code top-level domain (ccTLD) for Thailand. It's typically used by individuals, businesses, and organizations that are based in Thailand or linked with the country. To register a .in.th domain, the registrant must either be a Thai resident or have a legally registered business in Thailand. The domain provides a geographical connection to the region, making it a significant tool for those wanting to establish an online presence in the Thai market. https://tld-list.com/tld/in.th#:~:text=in.th is the internet,or linked with the country.

-

Apologies, got my maths completely messed up when I calculated the remittance percentages (in my defence is was before 6am, 1st coffee & 1st shower). The percentage remitted would be 80% (£10,000 of £12,500) Original Investment & 20% (£2,500 of £12,500) Gain so if you were to remit £5,000 £4,000 of it would be Original Investment & £1,000 capital gain.

-

Any unrealised gain is only a paper gain until you sell the asset at which point it becomes the actual Gain and that's what counts for Tax (In the UK anyway excluding the re-baselining of Property Values so they can stiff Expats for CGT when we come to sell our homes there). I do agree there is very little chance of being caught (but we're trying to discuss the rules not enforcement) & even less chance of them being able to understand capital gains position on stock you've held for many years but they always have the "Well I think you owe this" card to play and tax you accordingly.

-

Again, I can only go of what I have read/watched online but you use a percentage basis to determine what part of your remittance is original investment & what part is gain. E.g. I buy some shares for £10,000 and make a £2,500 profit on it making a 25% gain then anything I remit is considered 75% original investment & 25% gain. Q9 on the Sherrings link refers to you deciding whether you're remitting assessable income (essentially anything that isn't designated as non-assessable in a DTA) it does not say you can choose which part from the sale of assets your remitting is original income / gain.

-

Have to say the examples I've seen from the likes of Expat Tax say very clearly that the Capital Gain is based on the initial costs of the assets & not the value as at 31/12/2023.

-

Reform UK Overtakes Tories in Polls for the First Time

Mike Teavee replied to Social Media's topic in World News

And I think you were absolutely spot on... Can you imagine how much you could have made on that "Bet"! -

Reform UK Overtakes Tories in Polls for the First Time

Mike Teavee replied to Social Media's topic in World News

For me the worst part about Brexit was that Camaronon had no plan if the vote turned out to be leave except to walk (run) away & this is the guy who is probably going to be the next face of the Conservative party. How sad is it to be British & an army of Lions ruled by Sheep ... {Edit I am British, raised on a council estate in Warrington, NW England so no slur against my fellow Brits) In my career we presented a plan to management about what we thought was the right way to go but always had to have a "Plan B" for what we would do if they didn't agree... Camaroron's plan was to "Run Away"... -

I have a TIN, never worked in Thailand & my only basis of being here is Visa Exempt or Non-IMM O ("Retirement")... So can confirm, you do not need to work in Thailand to have a TIN One of my UK Banks asked me for my TIN (Before I had one) & I told them I couldn't be bothered to jump through all the hoops to get one for the paltry <£2 in interest (already declared to UK Tax Authority) they pay me so close my account if they like (I keep 6 figure UK in there as it's my "Current Account" Mortgage), never got back to me. MY other UK Bank accounts have no interest in my TIN but would close down my account if they found out I lived in Thailand Permanently (Which obviously I don't as I'm on a Non-Immigrant Visa - QED I don't live in Thailand).

-

Big Thailand visa changes from June 1

Mike Teavee replied to snoop1130's topic in Thai Visas, Residency, and Work Permits

Meanwhile Philippines is offering Immigrant (PR) Status to people married to a Filipino/a... -

Seem to recall that the UK DTA has a 6 month notice period in it so if Thailand were to decide to withdraw then as long as it gave the 6 months notice before doing so there would be absolutely no fall out from it, UK just wouldn't care* as on balance there's nothing in that agreement for them. *If you want to know how much the UK cares about it's pensioners living in Thailand, read up on "Frozen Pensions"

-

Trying/Planning hard to ensure it does & the ultimate plan is to join you lucky sods on the LTR Visa in 2026 😄 Here's hoping things don't change too much between now & then, TBH the talk of Global Taxation is making me think twice about investing >$250K into a Condo, if it's not been squashed by 2026 I'll probably lean more towards Thai Bonds (or some other asset that can be easily liquidated) than property.

-

How am I Avoiding/Evading tax when All of my income arises in the UK & I (well my accountant) files a tax return to report it. Any income I've brought into Thailand thus far has been non-assessable for Tax either because I was non-Tax resident (for most of the time I've been bringing money into Thailand to set me up for retirement I was working in SG) or was from previous year's income (E.g. When I left Singapore my final salary payment was in Dec 2019 & I transferred over more of less what was in my Singapore bank accounts in Feb 2020 - None of it Tax Assessable). It is only this (well technically next) year when the possibility arises that some income I've earned in the UK might be tax assessable but as I'm only remitting up to my allowance + 150K it doesn't matter as there will be no tax to pay. Now if Thailand were to move to a Global Taxation model then I would agree that I could be avoiding/evading Tax by not reporting to Thailand income from my UK Banks, but if that ever happened I'll be Non-Tax Resident so it wouldn't apply to me. You cannot Avoid or Evade Tax if you do not owe any Tax in the 1st place.

-

Filing a Thai Tax Return Online

Mike Teavee replied to Mike Teavee's topic in Jobs, Economy, Banking, Business, Investments

It all depends on your allowances... E.g. Not a complete list but of the top of my hear... 60K - Everybody get it... Additional 60K - If you're married & your wife doesn't file a return 30K if you have any children... Additional 30K for any additional children born after 2018 25K if you buy Health Insurance 100K if you have life insurance 100K if you're receiving a pension 190K if you're over 65 Then add in the 1st 150K is tax free & take the total away from your 400K that is assessable... E.g. A Single person < 65 with no additional allowances would have 60K + 150K = 210K take this away from the 400K & you would pay tax on 190K (which would work out as 8,000B) - NB This assumes the income isn't covered by a DTA A 65 year old with no pension would have 60K + 190K + 150K = 400K - No tax to pay A Married 65 year old with a pension, 2 kids, Health Insurance & Life Insurance would have allowances of 615K, more if they had additional allowances that I didn't list above. -

I believe so, highly unlikely they would retroactively tax Global Income as laws tend to apply from a certain point forward.

-

Filing a Thai Tax Return Online

Mike Teavee replied to Mike Teavee's topic in Jobs, Economy, Banking, Business, Investments

No, I'm excited to get back >8K in withheld tax... I know I won't owe any tax as I'm managing my remittances to the level of my allowances+150K so there is no possibility of me owing tax 🙂