Everything posted by mudcat

-

The renewal and housekeeping presentation is up on their website: https://ltr.boi.go.th/page/news.html The Tax discussion is not up yet, but fyi the presenter from TRD was: Mr. Kasapon Singprasert, Senior Tax Economist from the Revenue Department steve

-

As far as I can tell from earlier comments above the BoI is simply following the wording of the Royal Decree (No. 743) B.E. 2565 (2022): Section 5 Income tax under Part 2 of Chapter 3 in Title 2 of the Revenue Code shall be exempted for a foreigner categorised as Wealthy Global Citizen, Wealthy Pensioner, or Work-from-Thailand Professional who is granted a Long-Term Resident Visa under immigration law for assessable income under section 40 of the Revenue Code derived in the previous tax year from an employment, or from business carried on abroad, or from a property situated abroad, and brought into Thailand. This will certainly exempt from taxes for all but current income - simply waiting to the next calendar year would effectively exempt even income from employment, business, or gains from property. I see this as akin to the 2023 asset exemption from 2024 taxation - keeping good records should suffice while remitting current year income will be taxable. Try to think of this as grandfathering in the 'previous year income exemption' that went away a few years ago.

-

I did answer the BoI survey with my priorities and issues. I took this as an effort to expand the feedback from existing visa holders beyond those attending the community meeting. For the open ended comment I asked them to consider allowing current holders to re-qualify and renew at the end of the initial 10-year term. I mentioned that for Wealthy Pensioners at least some of us will be in our eighties by the time the initial Visa expires.

-

BoI's reply This event is for in-person attendance only. There will be no online session, and no materials or details will be shared after the event.

-

I have requested that BoI-LTR provide presentations and any handouts on line.

-

I live upcountry so responded to the invite with a question if there would be video streaming. No plans for it was the response. Should anyone attend a report would be appreciated.

-

There is no trusts here so you should research and consider "controller of property". As we do not trust the inlaws with what we would leave our granddaughter we appointed a nephew who did a good job raising his son

-

Been carrying the same model Eagle Creek shoulder bag for more than twenty-years. Can carry most of what I need, currently I usually carry phone, glasses case, paper wipes, etc. but there is room for more if need be. If I am traveling out of province I add my passport in a Eagle Creek passport bag which has its stitching needing attention. Buy good quality and it should last for years, style be damned. Still on EBay for $20. https://www.ebay.com/itm/157630400631

-

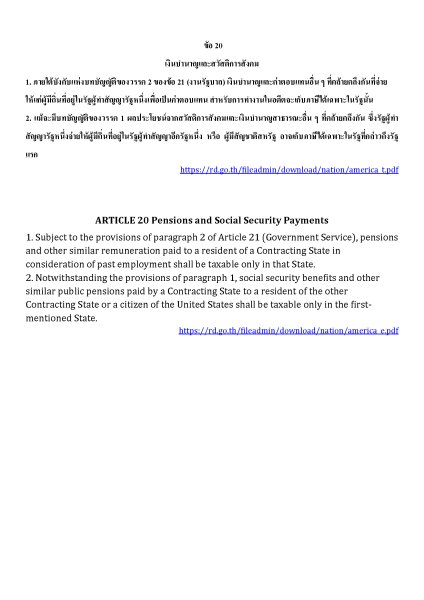

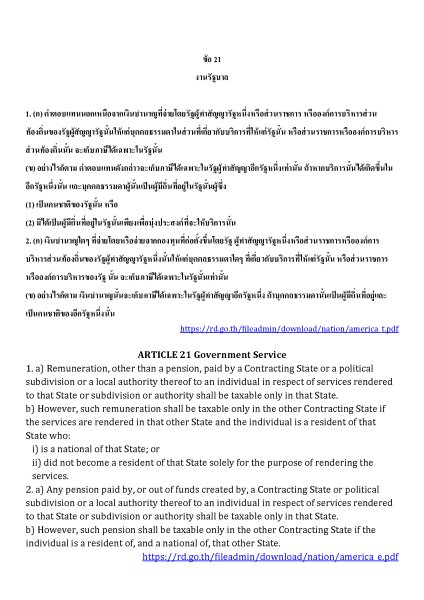

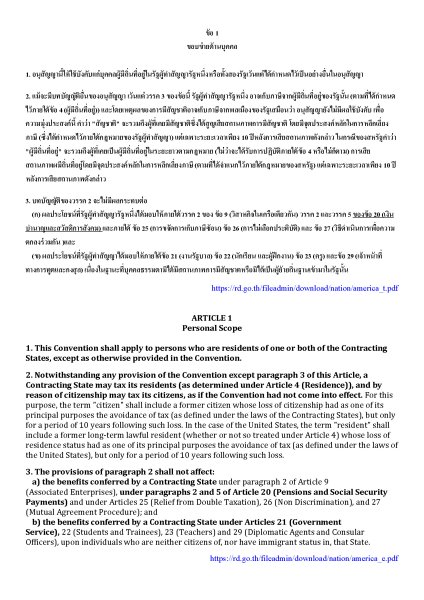

I find that presenting a questioning TRD officer with their own version of the DTA in both Thai and English to be helpful. Here is are jpg converted from from a Word document via Acrobat of Article 20 covering Social Security. You might find the next article (21) which covers non-government pensions, including company pensions and retirement accounts helpful in arranging your finances. Article 1 Paragraph 3 exempts your SSA benefit from the savings clause.

-

Remember it is not five days on holiday but the need for retraining

-

A few notes about my current situation here. I carry Pacific Cross health insurance, continue to pay Medicare Part B, and have a long term insurance policy - why so much insurance? I don't want to live here without my wife. should she go before me or we divorce so can easily return to my home country. Our living expenses are covered mostly by my US Social security benefit ~65k ThB paid into my BBK account. My wife will collect a similar amount as a survivor after I die so I don't need to worry about what I leave her. Main US assets are a Roth IRA and a brokerage account, both of which have her as sole primary beneficiary which removes them the need for probate.

-

My comeback to anyone who asked or noted I had lost weight was to ask in return if they had found the aforementioned pounds. Dirty looks followed.

-

We very much like our Panasonic refrigerator - double door with the freezer on the bottom. We have a small Samsung in the dining room that gets lots of opening to get out cold water and yoghurt drinks - saves wear and tear on the more expensive Panasonic that actually has food in it. Double drawers in the refrigerator section - one for meats/seafood, one for vegetables. https://www.panasonic.com/th/consumer/kitchen-appliance/refrigerator/2-door-bottom-freezer-refrigerator.html No complaints except for the little bit of groaning as the freon circulates, that and needing to brace the overflow reservoir that was vibrating - a rubber washer fixed that. Assume it will keep going longer than me. Not cheap (today's prices seem to run around 20K - , but I have some faith in the brand from my many Lumix digital cameras and other things over the years.

-

We have be relying upon FVAP's fax service back to our election office for years. When I looked to see why our ballots had not been received our Registrar of Voters had this to say: Military and Overseas Voters Alert! Effective August 1, 2025, the Federal Voting Assistance Program discontinued their service of faxing overseas voters’ election materials to county election officials. You can no longer send your voting materials to fax[at]fvap.gov. We are going back for a short visit in October so we can drop our ballot in the drop box outside of City Hall, but for next year does anyone have any trusted fax service? I will see if ACS at the embassy has any options (we are going to be at the Bangkok Consulate before we leave, so ACS could actually perform a Service for American Citizens. Steve

-

Had no luck inside, went to the porch with better light and got it to work.

-

In the U.S. the Treasury reports an average for the tax year for every country. Baht in 2024 was 34.33. https://fiscaldata.treasury.gov/currency-exchange-rates-converter/

-

I have one only to pay Google for YouTube prime. Google refused to continue my account using a U.S. Visa card. They demanded a Thai card and the Bangkok Bank MasterCard works. I think the issue for Google is that the Thai pricing is less than the U.S. pricing.

-

You might consider pre-filling out an example CRODA (Consular Report of the Death of an American Citizen Abroad) so your survivor has most of the information in front of them when dealing with the ACS (American Citizen Services - https://th.usembassy.gov/u-s-citizen-services/ ) whom I found to be very courteous and sympathetic. The Thai Consulates here issues an electronic version: https://th.usembassy.gov/electronic-report-of-death-of-a-u-s-citizen-or-u-s-non-citizen-national-abroad/ More information here: https://fam.state.gov/fam/07fam/07fam0270.html Here is a version to illustrate the layout and information included - pre-filling it out will ease the burden of your survivor(s) https://common.usembassy.gov/wp-content/uploads/sites/117/2023/10/DS-2060.pdf Besides my information - passport, birth, U.S. address I I listed as notify/copies to my spouse, my U.S. executor and alternate, my U.S. broker, and checked social Security and VA (I am a veteran). At one point a translation of the Thai death certificate - this requirement has be dropped. There is a Thai translation of what the Embassy can and cannot do as a call-out on the upper right of https://th.usembassy.gov/u-s-citizen-services/death-of-a-u-s-citizen/

-

U.S. Postage rates for Priority Mail envelopes from the U.S. to Thailand (price group 7) is $57.60. What the rate is for the SSA I don't know - may be negotiated. For reference the return envelope to Wilkes Barre was ThB 68 or a bit over $2.00 this morning which is similar to the U.S. to Thailand $1.70 for airmail letters

-

Received at lunchtime outside of Nang Rong, Buriram - Postal Code 31110 - dated July 31st. No date on the envelope, but I do note that it was sent Intl. Priority Airmail. I received an envelope from my pension provider it cost them $1.70 for pre-sorted 1st class mail ($0.68.6 plus an additional $1.014). Postmarked on the 17th and arrived fifteen days later on August 1st.

-

I used SNOWWHITE in Bangkok to print a large graphic in HP RTL format with excellent results. info(at)snowwhite.co.th Their webpage does mention scanning so you could contact them through various means, they are very responsiv and priced my job quite reasonably.

-

As to USD/ThB exchange rates. I typically use 33 ThB per dollar as that reflects a midpoint (28-36)in my experience from 2012 to 2024. When I lay out benefits for my wife's spouse/survivor benefits I use 30 in the main tables and expand possible benefits to 27, 30, 33, 36 as I believe that is a more accurate way to help her understand that she will not be poor in her old age: Survivor: @ 27 ฿/$: ฿54,981 @ 30 ฿/$: 61,090 @33 ฿/$: ฿67,199 @ 36 ฿/$: ฿73,308 Spouse: @ 27 ฿/$: ฿25,153 @ 30 ฿/$: ฿27,947 @33 ฿/$: ฿30,742 @ 36 ฿/$: ฿33,537 Fortunately I never used my SSA paid benefit to qualify for my retirement extension choosing to park the ThB 800K in a term account. Now that I have an LTR visa I pay attention to exchange rates only for large purchases and to keep my only Thai bank account balance high enough to allow them to claw back the benefit paid during the month of death.

-

Never far from our minds as we count the years (going on eight) that a neighbor is still bedbound after a major stroke. His stroke was misdiagnosed by the local hospital as a headache and sent home with (you guessed it) paracetamol. By the time he was transferred to the next level hospital it was too late - they could keep alive but there was no hope for improvement in his condition. His mother (in her 70s) is full time care nurse and regrets not giving any instruction to let him die when under care. He is aware and tries to communicate through vocalizations and nods, but what goes on in his mind is unknown other than he is unhappy. We bought a hospital bed with pump to avoid bed sores, a wheelchair, and diapers for when the 30-baht allowance runs out and whatever else she/he could use to make the long road less arduous but we cannot ease the emotional burden other than being a friend. I have discussed with my wife the U.S. Social Security definition of when she will need to ask to be appointed representative payee (in charge of spending my Social Security benefit for my benefit): WHO NEEDS A REPRESENTATIVE PAYEE (From SSA-787 Medical Opinion of Capability.pdf) “Some individuals … who have mental or physical impairments are not capable of managing their SSA benefits or directing others to manage them to meet their basic needs, so we select a representative payee to receive their benefits on their behalf. …. However, a person’s need for some assistance with financial tasks such as bill paying, etc. does not mean he or she cannot make decisions concerning basic needs and is incapable of managing his or her own benefits. If the individual is able to direct the management of his or her own benefits, then we will consider the individual capable.”

-

Ran into this at work fifteen years ago when the lunch bunch included Bob L. from Hong Kong, Sam A. from Beirut, Hassan from Daka, Garth H. from South Africa, and me from New York. I would make a allusion to cultural touchstones from the 50s and 60s and got blank looks. Coincidentally those were the end of a common culture in the U.S. Comes from working with a group that grew up as the smartest kid in the room (all engineers, some of them even civil) leavened with me, the smart ass.

-

You don't remember the requirement for full year health insurance policy to coincide with the visa? Pacific Cross would not extend but offered to cancel and apply again.