ianguygil

-

Posts

636 -

Joined

-

Last visited

Content Type

Events

Forums

Downloads

Quizzes

Gallery

Blogs

Posts posted by ianguygil

-

-

no country refinances government debt at lower rates than Japan (since two decades).

1Y JGB 0.14%

5Y JGB 0.39%

10Y JGB 1.07%

Japan easily finances the government debt domestically. They do not rely on foreign countries to buy their debt, although China has started to buy some Japanes debt in order to diversify their FX reserve holdings.

And Japan has had serious deflation for 20 years now, prices in Yen are so much less than they used to be for almost everything, hotels, clothes etc.

Western countries, especially the UK and the US, do not finance all of their debt domestically.

Having had Uk and US girlfriends before and a Japanese wife now, I can see why!

:jap:

:jap: -

While I think many western governments, including the UK, are in a very serious fiscal situation, which will probably only get worse, I think it is worth noting that the average maturity of UK debt is much longer than many other western governments. This gives them some relative protection against short term swings in interest rates compared to the US and several other European governments who have focused on short term funding in order to lower their interest costs.

With so much in short dated debt, they will have issues with funding not just the new debt, but also the existing debt which is coming to term. So I would say, unbelievable mess that it is, that the UK is managing their debt issuance in a much more responsible way that many other nations.

The UK also has the advantage of having a growing population (I will not get into immigration politics here), which puts them in a far better macro position than those European countries with shrinking populations.

-

without going into the details the overall best deal is an account with a local bank that has a branch in your country,i use bkk bank- they are in new york,and transfer money from my american account(not in new york and not bkk bank!) to the bkk bank account in thailand.regardless of the sum the fee is 25 $ and there are no withdrawal fees if you use their machine where you have the account.

This is correct. It's not a complicated process, really. Direct bank-to-bank transfers tend to be the most secure and hassle-free. Sur-charges tend to be nominal to free. Nearly all worldwide accredited financial institutions have SWIFTCODE cash transfers at the ready. If problems arise.....one has account numbers and bill of lading proof to fall back on. Just find respective banks that work for you and your individual needs and desires.

I am an American living in Thailand.

When I want to transfer a few thousand dollars from my US bank to the Bank of Ayudhya, how can I be 100-per-cent sure that the dollars will not be converted to baht until they are here in Thailand?

A few tears ago I lost about $300 on a $2500 transfer. I've had two transfers since then that were okay. I just want to nail it down with the US bank. What do I tell them? Thanks, David

file name vertume

You should ask your bank to put "do not convert' in the SWIFT payment message. I believe it is in the bank-to-bank instructions field, don't remember the field number on a Monday morning, maybe Field 72??

-

Jim,

Please PM me with your contact details. I will get somebody on the Operations side to get in touch with you and to sort this out. We will call you.

We currently do not offer SMS to international phones because of the costs of the SMS and the fact that we do not charge for iBanking. That is something we are looking at. An International SMS costs about 30 times as much as a domestic SMS we purchase in bulk. So the ideas of others to use a local phone with roaming on a very cheap plan is a good on for this time while we sort out a workable solution for people like you. We definitely want to provide a rich service which meets your needs, it just takes time to work through the alternatives and come up with the right approach.

I will look for your PM. I will also give you my email so you can contact me directly at the Bank.

I have no idea about the Bank Mail problem. Please logoff, close your browser, go back in and try again. I am assuming you have nothing unusual on your PC. FYI, we block special characters to prevent a certain type of hack like a SQL Injection. Security always has to be first. But I understand you say you did not enter any special characters.

Thanks

Ian

it's cool to get a reply here from someone here who actually works for the Bank.

Ian, not that I want to hi-jack the topic, but what about the i-banking nowadays ?

my landlord helped me open a savings-account 4 years ago (she only could do so because even she is Taiwanese, not Thai, she is a very well-off customer of the local BB-branch)

we did not apply for i-banking that time. when she went to the same branch with me last year, the person in charge she knows very well was not there, and the old lady sitting in his seat just said the usual "Farang mai dai" after I told here I do not have a work permit (I never had, though I have a multiple non-Immi- B ) without elaborating further.

how is the situation now ? can every Branch still decide indivudually ? my account at BKK BANk is relatively useless, as I can not do any online-transactions, so basically I only use to get my Electricity-Bills deducted from there every month.

thanks in advance for clarification

Please PM me offlline.

We can deal with it securely they you can post whatever you feel is appropriate.

I will deal with this one on Monday, so please give me some time. I have to nip off somewhere in a few hours - even Bankers have families

Thanks

Ian

-

I pay $25 to my Investment company (fair) and transfer in dollars to Bangkok Bank. They have never charged me a fee. On the contrary they give me the best possible exchange rate.

Well, your investment company is charging you a $25 fee, which is probably the SWIFT wire fee. And, as shown above, Bangkok Bank charges .25% -- minimum 200 baht, max 500 baht. Not sure who "they" are/is, but it doesn't make any difference in this situation -- as both are definitely charging you a fee.

And, yes, by transferring dollars, not baht, you'll get a better rate (the baht is just too thinly traded to do well with offshore FX). And that rate is the telex rate (TT), which is only about 12-15 satang off the base rate/interbank exchange rate. Certainly a better rate than you would get buying baht with dollars at a Bangkok Bank cashier's cage.

In emergencies, a SWIFT wire is the fastest -- normally one business day (from the States anyhow -- but from Europe, SWIFT seems to take about a week....). But, it does cost considerably more than the cheapest way to send money (from the States, that is)..........

....which is ACH. Rates shown in a post above. And, most US financial institutions, if not all, now have the ACH electronic funds transfer option (some, like Bank of America use a middleman, which slows things down, and costs a few dollars -- but most don't charge anything). However, for this substantial cost savings, it takes two business days for the money to reach Thailand, at least with my experience with USAA Savings Bank (vice one day for a SWIFT transfer).

Don't know when the OP transferred his money, but, say it was Nov 4th, when the TT rate was 29.57. An ACH to BB NY of $11,000 would have $10, 990 sent to Thailand ($10 BB NY fee taken out up-front), where it would be converted to 324,474 baht (after the 500 baht Thai side fee was subtracted). A transfer even earlier than Nov 4th would have realized even more baht...

Why the OP's family only realized 320,000 baht -- with 3,500 baht appearing to be another fee -- is interesting. Yes, the first "cost" was exchanging to baht before transfer. But, the 3,500 "fee" ($115) doesn't quite make sense, as this is too much for a correspondent bank to charge. Maybe Wells Fargo added on to this.....

Anyway, suggest anyone with a US financial institution account -- and a Bangkok Bank account -- establish an ACH path to Bangkok Bank NY. Even if just for future emergencies.

SWIFT payments UK to Thailand take one business day.

Well, without getting too far into this, it is possible if there are intermediaries, that a SWIFT payment can take longer. But if you are sending from a UK bank which has a correspondent relationship with us, or whatever Thai bank you are using, it will take 1 day. If you are sending from your UK bank, via our London branch, it will take 1 day in most cases. But if you send from a UK bank which pays via another UK bank, who uses another bank (say Citi) as their clearing agent in Thailand, then Citi pays us via the local clearing networks, it will not only take longer, but you will encounter much more in fees.

That is why using BACS to our London branch is normally the cheapest and fastest, unless your bank in the UK is our direct correspondent.

-

Just a little side note about how fees work when sending money to Thailand via Bangkok Bank New York branch.

It is a tiered fee system. Charged in NY:

Under $50- no fee

$50-2500- $5 fee

$2500+- $10 fee

In addition, charged in Bangkok a sliding scale of up to 500 B depending on the amount sent.

So the maximum fee incurred (say you send $7000) would be $10 plus 500 B- about $27 US at the current exchange rate.

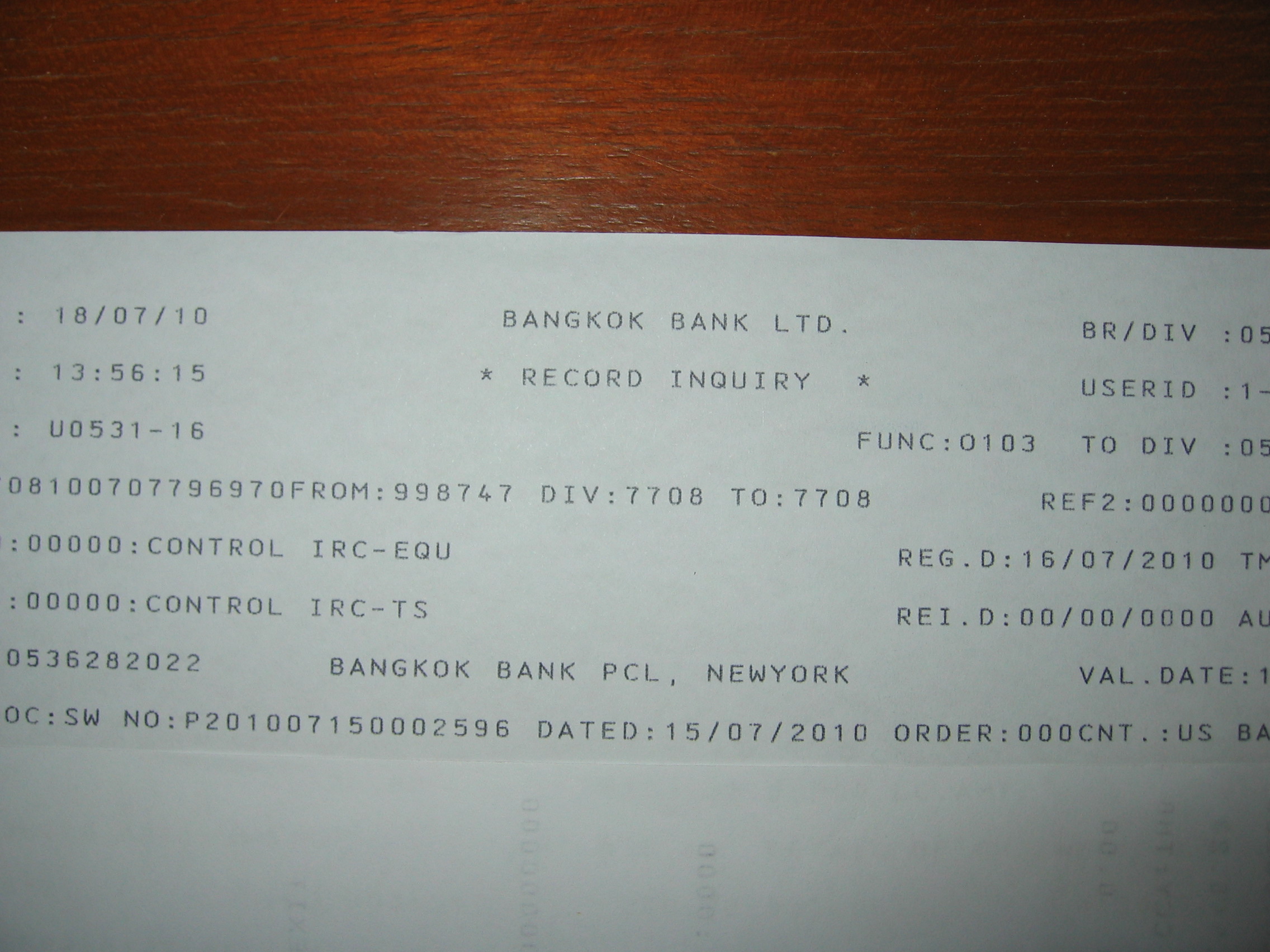

There is a way to determine exactly what fees are being charged. You go to your home branch, and ask for one of these:

I've blocked off the bottom of the document for privacy reasons. On this page is listed the entire money trail, from the originating acct to BBL New York to BBL Bangkok, and all the fees incurred. Also it shows the exchange rate which is always the current telex rate (known as the "TT" rate).

As this is not Chiang Rai specific, moved to the banking sub forum, with a live link remaining.

BTW, this document can come in handy should one wish to repatriate monies from Thailand back to the home country. It proves that the money in Thailand had a foreign source, and is thus legal to take out.

Here is the link to our website where these fees are detailed.

http://www.bangkokba...0usa%20fee.aspx

And here is the current content of that page:

Fees

- Bangkok Bank in New York charges the following fees for funds transfers initiated via the US ACH system:

Transferred AmountFee Less than USD 50.00Free

USD 51.00 - 100.00USD 3.00

USD 100.01 - 2,000.00USD 5.00

USD 2,000.01 - 50,000.00USD 10.00

USD 50,000.01 or moreUSD 20.00

- Bangkok Bank in Thailand also charges a fee of 0.25% of the amount in the Baht currency (minimum of THB 200; maximum of THB 500) when the funds are deposited into the recipientÆs Bangkok Bank account in Thailand.

Thanks for the excellent info and clarification, ianguygil!

My pleasure.

I encourage all board members to use our Website www.bangkokbank.com to lookup information. Fees and conditions are all clearly posted (as required by the central bank) and we use as little Banker Talk as is reasonable. We updated the site a few months ago and the new Sharepoint environment has much better search capabilities than our old site if you can not easily find something using the navigation menus (I would never have admitted there was anything wrong with the prior search functionality of course

)All please feel free to PM me if you can not find something or if you are encountering problems. A PM gets my attention much faster than a post, although feel free to post also as it shares the information with the board members.

- Bangkok Bank in New York charges the following fees for funds transfers initiated via the US ACH system:

-

But I understand you say you did not enter any special characters.

It may be possible he has his browser Character Encoding wrong such as UTF-8 or Thai. Needs to check to see if it is set to Western and see if that makes a difference.

I agree we need to check the browser setting. But please note that iBanking is fully Thai compliant and has been since the launch 9 years ago.

-

Jim,

Please PM me with your contact details. I will get somebody on the Operations side to get in touch with you and to sort this out. We will call you.

We currently do not offer SMS to international phones because of the costs of the SMS and the fact that we do not charge for iBanking. That is something we are looking at. An International SMS costs about 30 times as much as a domestic SMS we purchase in bulk. So the ideas of others to use a local phone with roaming on a very cheap plan is a good on for this time while we sort out a workable solution for people like you. We definitely want to provide a rich service which meets your needs, it just takes time to work through the alternatives and come up with the right approach.

I will look for your PM. I will also give you my email so you can contact me directly at the Bank.

I have no idea about the Bank Mail problem. Please logoff, close your browser, go back in and try again. I am assuming you have nothing unusual on your PC. FYI, we block special characters to prevent a certain type of hack like a SQL Injection. Security always has to be first. But I understand you say you did not enter any special characters.

Thanks

Ian

-

Just a little side note about how fees work when sending money to Thailand via Bangkok Bank New York branch.

It is a tiered fee system. Charged in NY:

Under $50- no fee

$50-2500- $5 fee

$2500+- $10 fee

In addition, charged in Bangkok a sliding scale of up to 500 B depending on the amount sent.

So the maximum fee incurred (say you send $7000) would be $10 plus 500 B- about $27 US at the current exchange rate.

There is a way to determine exactly what fees are being charged. You go to your home branch, and ask for one of these:

I've blocked off the bottom of the document for privacy reasons. On this page is listed the entire money trail, from the originating acct to BBL New York to BBL Bangkok, and all the fees incurred. Also it shows the exchange rate which is always the current telex rate (known as the "TT" rate).

As this is not Chiang Rai specific, moved to the banking sub forum, with a live link remaining.

BTW, this document can come in handy should one wish to repatriate monies from Thailand back to the home country. It proves that the money in Thailand had a foreign source, and is thus legal to take out.

Here is the link to our website where these fees are detailed.

And here is the current content of that page:

Fees

- Bangkok Bank in New York charges the following fees for funds transfers initiated via the US ACH system:

Transferred AmountFee Less than USD 50.00Free

USD 51.00 - 100.00USD 3.00

USD 100.01 - 2,000.00USD 5.00

USD 2,000.01 - 50,000.00USD 10.00

USD 50,000.01 or moreUSD 20.00

- Bangkok Bank in Thailand also charges a fee of 0.25% of the amount in the Baht currency (minimum of THB 200; maximum of THB 500) when the funds are deposited into the recipientÆs Bangkok Bank account in Thailand.

- Bangkok Bank in New York charges the following fees for funds transfers initiated via the US ACH system:

-

International Funds Transfer via Bualuang iBanking

International Funds Transfer via Bualuang iBanking is a great way to transfer money overseas quickly and conveniently with Bangkok Bank's highly secure internet banking service. Funds can be used to pay for overseas educational expenses, send money to relatives living abroad (for Thai nationals) or to repatriate income (for foreigners working in Thailand). The service requires a one-time registration set-up, and then transfers can be made on demand at your own convenience.

Go here:

Thank you for the link, have you tried this service yourself, or know anyone who tried it?

Can I send the money to my own bank account in Europe, it seems like the service is aimed at someone who will send money to someone else.

As aurelius says, this is a very straightforward service, used by a growing percentage of our customers. If you have any problems please PM me. Thanks

Ian

-

I have hired hundreds of IT staff over the years here. And I will not give too many pointers as we are in competition to some extent

However, I would say that among the Thai staff are some of the best I have worked with, including those in my long stints in San Francisco and London. I would also say that you get what you pay for, wherever you are. Also, I believe ADDECCO (spelling) has a salary survey for IT companies in Bangkok, should you happen to use their recruiting services. So that should give you some pointers.Back in the US, I once interviewed somebody for a senior techical position. He got every answer wrong. When I pointed out that things were not "so good" in the interview, he said to me that he "can not remember technical details worth a dam_n". One of my absolute favorite quotes in thousands of interviews. He still expected to get the job, even though he could not remember the basics of how things work. Years later somebody joined as a Vice Chairman with exactly the same name, I though my days there were numbered until I saw his picture and confirmed that it was a different person....

Finally, I am always disappointed by blanket statements about the entire population of any country. Without quoting anybody, I would say that it is clearly possible to hire and retain smart, qualified and effective IT people in Thailand.

-

I got a Be1st Debit card from BBL just a couple of weeks ago with my name on it. Ask at the branch - it takes a week or so as they have to process it centrally, but its no extra charge. The PIN was mailed to my address.

This is confirmed by the Product side in the Bank. It is available, but it needs to be created outside the branch.

Very useful having informed customers like aurelius :jap:

-

While I am not an expert in our cards, this should be no problem.

This is a "card not present" transaction, so there is no way for them to verify what is actually physically on the card..They just want you to tell them what the name is associated with the card. So if you enter your name as when you applied for the card (which I assume is identical to your old card) it should be accepted.

If you have any more problems please PM me. I will get someone on the business side to look at this tomorrow.

Today is a holiday :jap:

Ian

-

A recent trip to the UK showed me that Thailand must be suffering with exports......Thai rice was the most popular/bought rice a few years ago, the shelves in Asda, Tesco etc were crammed with Vietmaneese rice and no Thai seen anywhere, proof their exports must hurting...Also a nice pint in a pub was only 2 pounds, thats just 90 Baht, the same price as a crappy small Singha in a crappy beer bar here....Tourists only have so much to spend...if they got $1,000 for a 2 week holiday thats all they got and that used to be well over 40,000 Baht, now its down to round 29,000...

I was in London a week ago on business.

A pint of beer in a pub, and I went to about 5 pubs, is around 3.50 GBP to 4.00 GPB. That is for bitter, not for lager.

So the prices are about what they have been for about 2 years

I get the often. The hotels are horrendously expensive.

-

Please call 1333.

There is an English menu and we have English speaking staff always working.

They will answer your questions. Thanks

If you live here you can get iBanking and check online. It is the same product as used in the US by CHASE and many others.

Ian

Hi Ian,Bangkok Bank told me foreigner need a workpermit if they want to use iBanking,no workpermit,no iBanking,was the reason why I changed to Kasikorn

I will send you a PM as with the other poster. If you want to use iBanking still I will see what I can do to help.

From our website, these are the actual conditions. You do not need a work permit. But you need proof that you live here, not a hotel address.

"How to apply

1. Apply at an ATM

You can register for Bualuang iBanking at any Bangkok Bank ATM using an ATM card or a Be1st debit card between the hours of 7 a.m. – 10 p.m. For detailed instructions, please click here.

Please note: if you do not have an ATM or debit card, please sign up at a branch.

2. Apply at any Bangkok Bank branch

Step 1: Visit a branch and submit documents Visit any Bangkok Bank branch and fill in a Bualuang iBanking Application Form. Submit the form at the branch together with the required documents:

- Citizen ID card or valid passport

- Passbook(s)

Foreign customers should provide their passport and evidence of a local residential address (not a PO Box or Hotel). Please also bring details of any accounts you wish to pre-register.

"

-

Thanks for all the helpful responses. That graphic of the BB online log-in totally convinces me that it's out there, but for me?

When signing up for my savings account I asked about ibanking and the efficient young lady told me with certitude that as I have an O-A visa and no work permit I can't get ibanking.

Since I am a resident -- if that means having a rental contract, which I do, and which I flashed at the efficient young lady -- I'll go back and give it another try. Maybe she wasn't such an efficient young lady after all.

But what the heck: have to buy another liter of soy milk at Villa Market anyway.

Thanks all.

Shido

Please PM me.

I will send you my Bank email and we can make sure this moves along smoothly. Thanks

Ian

-

Please call 1333.

There is an English menu and we have English speaking staff always working.

They will answer your questions. Thanks

If you live here you can get iBanking and check online. It is the same product as used in the US by CHASE and many others.

Ian

-

I really do not know about USAA, so you should ask them yourself directly. And tell them you want to pay directly to Bangkok Bank in Thailand and ask if they have a correspondent relationship to support this.

USAA's SWIFT wire transfers have always taken one business day -- and have received the advertised TT rate at BB. So too with SunTrust -- several years back when I was with them. Haven't the foggiest who their correspondent bank(s) are -- but since I had no problems, I really wasn't concerned.

I was just curious about the OZ chap who apparently got ripped-off because of too many SWIFT wickets to go through -- and your awareness that such wickets can -- and do -- exist. Curious, because of all the years perusing this forum, I have never seen any SWIFT wires from the States criticized for FX gouging, except when baht was mistakingly sent, vice dollars. But, then, I may have missed something.......

Anyway, just curious about how such things can occur.

Jim

I will try to go back to the post and send you a link.

What it is (why it can happen) is that some large global banks sell themselves as the global clearing agent for many regional banks so as to simplify their lives, give discounts on volume, just like in any business. Seems you have just been lucky. But that is why having an account with us is advantageous as you are much more likely to find your bank has a correspondent relationship with us compared to smaller rivals. We have a large percentage of our business on the International side compared to all Thai competitors.

Jim,

This is the term you need to use to tell your local bank to pay directly and not to go through a Thai intermediary. As I said before this only works if your bank has a correspondent relationship with us. I got this from our Global Payments people when the prior guy from OZ had a problem and his payment was cleared via Citi in Bangkok.

"please advise the remitter to state "Do Not Convert" in the payment message field of the telegraphic transfer form. The funds should then be remitted directly to Bangkok Bank."

-

Actually, as this is a possible fraud, the best thing for you to do is to call our 24 hour call center and ask them to investigate. You can still email me, but I am busy all day in meetings and presentations and may not get to this until this evening.

So please call us on +66-2645-5555. Thanks

-

If you think that your account has been compromised you need to contact us directly and give your details (name, account number etc.). It would be best if you called us directly as they will need to ask you some questions. I will send you a PM with my Bank email address and then we can start the process. But this is very urgent if you truly suspect fraud has occurred. So please get on this right away. I will get somebody on the operations side to deal with this. Thanks

Ian

-

As AURELIUS said it is very possible and easy to do. We offer a good range of currencies and definitely have EURO and USD accounts. And as AURELIUS said you can access them on iBanking and transfer from them to THB online when you need to.

Please PM me if you have any more specific questions you want ot ask and I can handle them offline (amounts, how much you want to fund, where you will transfer the funds from etc.). I can arrange for an appointment if that will help. As AURELIUS said the Head Office deals with large numbers of such accounts, so that is a good bet to get this done quickly.

-

I realize that you are asking for a resource in Thailand. However, I would definitely recommend that you buy this stuff in Japan. In the old part of Tokyo, not far from Hakuzaki, there is a whole street full of 20-50 shops selling these things. From the incredibly high end, to the more affordable. As you are (apparently) a pilot, if you fly to Japan it would be a simple thing to pick it up there.

The quality is breathtaking. It really looks like the real thing. Some of the things I see here are quite clearly fake. But these things, fish, sashimi, noodles, look like you can eat them.

Just my advice.

-

And no need for us to even use SWIFT. Which is why we can offer a lower price and a shorter time for the kinds of transactions in the US between 3rd party banks and our local branch (ACH to BBL NY then our internal network from BBL NY to BBL in Bangkok),

Ian, correct me if I'm wrong.....

....but, even tho' the pipeline from NY to Bangkok contains no SWIFT network equipment, the transaction itself is SWIFT encoded, thus satisfying the security requirements in-place for international wires from the US. This too also allows ACH transfers to BB NY, for subsequent routing to Bangkok, to meet the new International ACH Transfer (IAT)requirements.

Jim

I won't get too far into the details of what we do as it is an internal issue. But I can say that the security, and compliance issues, including all AML and central bank reporting, are fully satisfied.

Other banks have been doing this for a long time. When I was with Bank of America they used an internal formal called EXEC983 an put the BofA to BofA payments on their internal network. Very cost effective and provides the ability to provide funds immediately rather than the 2-3 day settlement which applied back then with SWIFT.

I hope this is enough to explain things.

-

"Would there still be an intermediary needed if you used the Bangkok Bank branch in Sinapore to transfer funds to Bangkok Bank in Thailand? And wouldn't you not even need to transfer if depositing in a Bangkok Bank account? I am not being sarcastic .. just curious because the OP sent the money to Bangkok Bank and there is a Bangkok Bank branch in Singapore on Raffles Place."

i suppose the answer is no.

I am sorry Naam. I am traveling, letlaged and did not read this post properly.

No. No need for an intermediary if the payment is between our branches and Head Office.

And no need for us to even use SWIFT. Which is why we can offer a lower price and a shorter time for the kinds of transactions in the US between 3rd party banks and our local branch (ACH to BBL NY then our internal network from BBL NY to BBL in Bangkok), and the UK (BACS to BBL London then internal network from BBL London to BBL in Bangkok).

Apologies from me again. I was not ignoring. I was just reading in a fog...... in my mind:blink: ... it is 3 am here right now..........

I will ask our Global Payments people to try to provide some guidance on how to make the payment with the least hops and the least charges. There is a term you can use for those banks who do have a DT/DF (Correspondent) relationship with us to force them to go directly not via intermediaries (if there is no correspondent relationship they have no choice).......

Merchant Accounts

in Jobs, Economy, Banking, Business, Investments

Posted

Please contact me via PM. I can get somebody here in Bangkok Bank to take you through the options we have including our Payment Gateway product. Thanks

Ian