Misty

-

Joined

-

Last visited

Posts posted by Misty

-

-

21 hours ago, Yumthai said:

My understanding, and I might be wrong, is that:

If the Surviving Spouse Is a Non-Citizen Non-Domiciliary (the case here)

As with domiciliaries, the unlimited marital deduction will not apply when the surviving spouse is a non-citizen non-domiciliary. Unlike domiciliaries, non-domiciliaries do not receive the federal estate tax exemption. Instead, they receive only a $60,000 exemption. Any amount they receive above $60,000 from their spouse’s estate will be taxed at a rate of 40%. A QDOT may also be employed in this situation to avoid high tax rates.

However, you are right stating:

If the Surviving Spouse Is a Non-Citizen Domiciliary

The unlimited marital deduction will not apply when the surviving spouse is a non-citizen. Fortunately, the federal government allows U.S. domiciliaries to claim the federal estate tax exemption. This exemption allows a decedent to transfer a certain amount of money to beneficiaries free of tax. The amount of the federal estate tax exemption for 2024 is $13.61 million and adjusts each year for inflation. However, the exemption is set to drop to $5 million in 2026, so couples should regularly review and update their estate plans to keep up with changes.

Essentially, if one spouse is a non-citizen but a domiciliary, estate planning can proceed as if both spouses were citizens when the estate is valued at less than the federal estate tax exemption rate. The estate will still be protected from tax even without the advantage of the unlimited marital deduction. If the estate has a value above the federal estate tax exemption rate, the amount in excess of the exemption will be taxed. One way to avoid undesirable tax consequences is to place the excess amount in a qualified domestic trust (QDOT). QDOTs will be discussed in more detail below.

https://www.dlgva.com/estate-planning-with-a-non-u-s-citizen-spouse/

Hi Yumthai, this is actually an area I've worked in for decades. I am not a lawyer, but after years of working with a number of US estate tax lawyers I do have a general working knowledge. It is a complicated (and always changing) area, so my only goal here is to provide some general information. People should consult directly with a lawyer as interpreting websites is leading to a lot of confusion.

The different links that have been provided (ex: Fidelity, Wiggins) are providing correct information. However, the interpretations that people are posting here may not be correct.

What estate tax deduction applies, the status of the deceased (ie. whether they are a US citizen) is what is relevant. If the deceased is a US citizen, the US citizen's estate receives the standard deduction for US citizens. For 2025 this is $13.99m and Ithe new tax bill has raised this to $15m in 2026. It doesn't matter if that US citizen is outside of the US, is married, who they are married to, whether they have a will, who or what they leave their estate to. Their estate receives the full standard deduction.

This is different if the person who dies is a nondomicile/non US citizen. So if the person who dies is a Thai citizen who is domiciled in Thailand and they have US assets, then in that case the $60k standard deduction applies.

The OP says he is a US citizen. So his estate would receive the standard US deduction that all US citizens receive (currently $13.99m going to $15m next year).

There are additional considerations but I don't want to add to the confusion, especially as it's unlikely that many US citizens posting here have estates valued at greater than $13.99m and if they do they are definitely talking to US tax lawyers already.

So again, as I started out suggesting on this thread, the best thing for people to do is consult directly with a real US estate tax lawyer. By that I don't mean read something on a website and try to interpret it, as clearly that is causing confusion.

-

1

1

-

-

1 hour ago, Yumthai said:

You still don't get it.

Have a reading:

https://www.wiggin.com/publication/estate-planning-considerations-for-non-u-s-citizen-spouses/

When both spouses are U.S. Citizens, it is unlikely that they will be faced with a gift tax or estate tax bill. The federal estate tax exemption of $13.61 million (in 2024) for each of them and the unlimited marital deduction for a married couple enables them to pass wealth free of tax. The unlimited marital deduction rules don’t apply when one of the spouses is not a U.S. citizen.

What happens when the U.S. citizen spouse passes away naming the non-U.S. citizen spouse as beneficiary? The answer is, the non-U.S. citizen spouse can inherit property in the manner as a citizen. However, under federal estate tax rules, a surviving spouse who is not a U.S. citizen must pay taxes on the inherited amount. The unlimited marital deduction rule does not apply!

I'm sorry, but I really do get it. The unlimited marital deduction is unlimited. The $13.99m (in 2025) is not the "unlimited marital deduction". Every US citizen is entitled to a $13.99m deduction, and this can go to anyone. No estate tax is due unless the estate is greater than $13.99m.

The $60k deduction OP referred to is for a non-US citizens with US assets. The OP says he is a US citizen, so $13.99m deduction applies, not $60k.

-

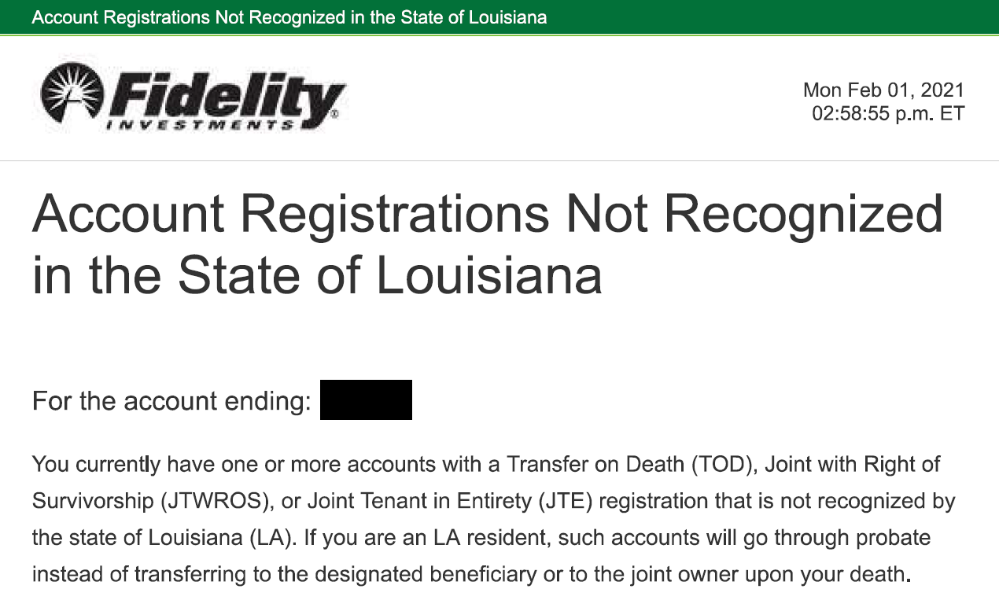

11 hours ago, JohnnyBD said:

I am a US citizen married to a non-US citizen non-resident spouse. My residence was Louisiana, and it's one of a few states that do not recognize TOD or JTWROS. Texas is another, where another daughter lives. All my assets at Fidelity Investments has to go through probate (see snippet below) and they are subject to US estate taxes if given to my wife. The unlimited marital deduction rule does not apply to non-domiciled non-US citizen spouses (see snippet below). I could leave some cash to my wife in my US bank (non-situated assets) by using a POD designation which LA does recognize, but my wife cannot enter the US and submit a death certificate in person at the bank, so that won't work. I plan to name my daugher using a POD to avoid probate, then she can send the cash to my wife tax-free each year up to the annual gift exclusion limit. I hope that clears things up.

Lifetime Gift/Estate Tax Exemption $60,000 (estate tax exemption) Unlike U.S. citizens who have a high lifetime exemption ($13.99 million in 2025), non-domiciled non-U.S. citizens have only a $60,000 estate tax exemption for U.S.-situated assets. There is no lifetime gift tax credit available to nonresidents to offset gift tax liability.

Okay, you say you are a US citizen, and therefore you are not a "non-domiciled non-US citizen". So the $13.99m exemption applies. The $60k limit is for non-citizens.

-

17 minutes ago, JohnnyBD said:

I have already consulted a US estate tax lawyer, and he told me the rules for leaving inheritance to a non-US citizen non-resident spouse are different than for a US citizen spouse. As I stated before I was told that if you leave your non-US citizen non-resident spouse anything over $60,000 in US assets, it will be taxed. And, if you leave your non-US citizen non-residewnt spouse as a beneficiary on one of your US bank accounts, it will also be taxed.

What happens when the U.S. citizen spouse passes away naming the non-U.S. citizen spouse as beneficiary? The answer is, the non-U.S. citizen spouse can inherit property in the manner as a citizen. However, under federal estate tax rules, a surviving spouse who is not a U.S. citizen must pay taxes on the inherited amount. The unlimited marital deduction rule does not apply! The federal government does not want someone who isn’t a citizen to inherit assets and pay no estate tax for fear that those assets would leave the country untaxed.

In that case, the only way that makes sense is if you yourself are not a US citizen. Is that the case?

If not, please could you DM me the details of the lawyer?

-

On 11/11/2025 at 9:34 PM, JohnnyBD said:

Just asking. Did you look into the US tax consequences of a JTROS? I was considering naming my wife as a beneficiary on my Fidelity brokerage & Chase bank accounts until I read some of the rules (see below). Also, I read if I put her in my WILL which had to go through probate, there would be a 40% tax on any monies above $60k. So, my plan is to let my daughter transfer money to my non-US citizen spouse up to the yearly gift exclusion limits to avoid any US tax consequences.

Holding property in joint tenancy with a non-citizen spouse is generally not recommended due to significant U.S. estate tax complications, as the surviving spouse may face a full estate tax liability on the entire property's value instead of a 50% split.

What happens when the U.S. citizen spouse passes away naming the non-U.S. citizen spouse as beneficiary? The answer is, the non-U.S. citizen spouse can inherit property in the manner as a citizen. However, under federal estate tax rules, a surviving spouse who is not a U.S. citizen must pay taxes on the inherited amount. The unlimited marital deduction rule does not apply! The federal government does not want someone who isn’t a citizen to inherit assets and pay no estate tax for fear that those assets would leave the country untaxed.

Suggest contacting a US estate tax lawyer. For 2025, the federal estate tax exemption is $13.99 million per individual, so a US citizen can leave up to $13.99m to anyone, spouse or otherwise. A US citizen can also leave an unlimited amount to a non-US spouse above this amount if a QDOT is established above the $13.99m. The $60k deduction is for non-US citizens with US assets, not the other way around.

-

1

1

-

-

12 hours ago, Jackinabox said:

I Really appreciate your detailed answer Misty. Now just have to find some legit thai company she can work at if it is Thai majority company...

If you get a chance, give the LTR unit a call about the WP46 and check with them about your questions. That unit was so helpful to me when I was applying. Also, my WP46 form went through a couple of updates as the form was processed through the section of the Labor Dept that works with the LTR unit, so you may find that you submit the form, and then the LTR unit may ask for some changes or updates later.

-

1

-

-

5 hours ago, Jackinabox said:

Hello (WP holder here), Wife want to get a DWP to work BOI said she need to be employed in a company and fill WP 46 anyone but have some discrepancies in the form. anyone have any experience with that have the following questions :

-

Company signatory – Should the person signing be listed as “Director” or “Authorized Representative” (as per company registration)?

-

Income section – Does “current income” and “income for previous year” refer to my personal income or the company’s? (if it is a new company leave blank?)

-

Employee numbers – For “total number of Thai employees,” as she is excluded from. as I understand . the 4 to 1 law can this be 0

-

Education documents – I will attach my C.V. and diploma. Are these enough, or do you need certified or translated copies?

-

Work permit no - i guess this will be filled later after approval?

-

Company structure - since this will be a newly opened company. Does the director of the said company need to be thai? What needs to be the objective of the company? Does it need to be a Thai shareholders majority company?

Can anyone answer from his experience or direct me to a english speaking lawyer that has experience with WP 46?

P.S this is the example form BOI gives : https://ltr.boi.go.th/documents/Employment-certificate-WP46.pdf

Hi Jack, I've submitted the WP46 for LTR linked digital work permits. Company signatory was an executor director of the company (in this case me). The income section is for the company's finances. Thai employee numbers - in the case you mention it sounds like this would be zero if there aren't any. Education documents - pretty sure this is for the person applying for the WP, in this case it would be your wife's education documents. Work permit number - leave blank initially. Company shareholders - does the company have a Foreign certificate or US-Thai Amity treaty approval? If not, my guess would be the shareholders should be majority Thai.

For a law firm that can help, the LTR site lists a number of "certified agencies" that help with the LTR visa itself, and some are law firms. See this link:

https://ltr.boi.go.th/page/ca.html

-

-

10 hours ago, Dezmo said:

I still have not received the Visa. I DM them again on Facebook... waiting...

I submitted the BOI letter to NYC on September 2 after receipt on September 1. It mentioned it is good until Oct 31. I did already pay the fee. I forgot what day I mentioned arriving in Thailand...maybe mid Nov..but just changed my flight o Nov 24.

Maybe they are approving in some order of arrival?

I just hope that by applying and paying the fee the BOI letter expiration now does not apply 😞 and it's fine since I paid already.

I'm sorry to hear about the delay. My experience with NYC via FB messaging was they were very prompt, answering within 24-48 hours. The BOI LTR unit has connections, albeit somewhat indirect. I'd suggest both emailing and calling the LTR unit to see if they can help clarify what the delay could be. They may be able to move things along through their back channels.

-

Much has been researched & written (and largely overlooked by the main stream media) on Epstein and various of his associates. Here's a couple of articles worth revisiting from decades ago:

"Jeffrey Epstein: International Moneyman of Mystery" The New Yorker 2002 https://nymag.com/nymetro/news/people/n_7912/

"The Talented Mr. Epstein" Vanity Fair 2003 https://www.vanityfair.com/news/2003/03/jeffrey-epstein-200303

-

1

1

-

1

-

-

Our firm's auditor has informed us that under Thailand's Labour Protection Act, any of our employees of retirement age or older can choose to retire on their own and is due statutory severance pay based on their length of service. We have a several employees in that category and have set aside funds should they choose to retire. I don't know if the same applies in your situation or in education but it might be worth getting legal advice.

-

2

-

-

1 hour ago, Anthony mellows said:

So beards are now banned.Didnt Abraham Lincoln and most of the generals in the American civil war have beards. I cannot see how that affects your performance.Even Vance has one.

In the old days, the Nuclear Biological Chemical (NBC) warfare training stated that beards could block the seal of protective masks. Not sure when beards came back into vogue since then, but maybe everyone wanted to look like Delta force.

-

1 hour ago, Tug said:

It was a spectacle those silent grim men having to listen to the both of them…..those guys and gals know (things) they have been watching this clown show administration.watching trump grovel to putin watching trump sell out the Ukrainian people…..betraying our alliances…..they know what Russia is about…..they know what N Korea is about…..sitting there listening to thease clowns.The silence was deafening.those folks aren’t the trailer trash average trump voter I don’t think they were impressed nor do they want to kill their fellow Americans.im of the impression that didn’t go as trump and company planned.

The silence was deafening. LTG Hertling called it: https://www.thebulwark.com/p/what-to-expect-quantico-meeting-generals-admirals-trump-hegseth

-

1

-

-

11 hours ago, JohnnyBD said:

I love it. Yes, many are more savvy than one may think. I have a friend from Belgium who just spent over 90 million Baht on 3 luxury condos, 2 in Bangkok and 1 in Pattaya. We live in an upscale area of Bangkok where many condo units sell for 30 to 100 million plus. Many of them are purchased by foreigners. I recently bought 2 condos for my wife in a really good area of Bangkok, but they are not in that price range. I'm not that rich.

Yes, I know a number folks for whom the LTR visa is a good fit. They split their time between places like Bangkok, Phuket, Chiang Mai, Hua Hin, across the eastern seaboard and in other countries including their country of origin. They have wealth. Not all are retired. Some own and are running their own businesses in Thailand.

-

2

-

-

- Popular Post

6 hours ago, TroubleandGrumpy said:Filthy rich as in a multi millionaire in $USD?

Yes.

-

2

2

-

1

-

1

1

-

On 9/20/2025 at 9:18 PM, 1tent42 said:

I suggest you email the Thai consulate where you applied for the e-visa. If it is New York they are not responsive. They do not answer their phones. But your experience may vary. it could be someone in the approving chain may be out on vacation.For the first LTR visa I received in the very early days of the program, I used the NY consulate. They didn't answer their phone, so at first I ended up calling the LA consulate to get answers. Then I discovered the NY consulate's FB page and DMed them. After that, the NY consulate was great, answering all questions in detail, via FB DM.

No idea if FB DM communication still works now, but it's worth a shot for anyone trying to talk to NY consulate. It worked a charm in Sep 2022.

-

1

-

-

- Popular Post

18 hours ago, howerde said:I looked at the LTR pensioner, however i have no faith in a 10 year visa that requires a review after 5 years who knows what garbage they could conjour up and blame a higher authority for any changes, i had an O-X visa and that is exactly what happened to me, the only positive is that LTR is done by the BOI rather than immigration,

I 100% agree that the BOI's involvement is a positive. For 30 years I had to deal with immigration and work permits on one-by-one, paper work intension, extremely time consuming, annual extensions. I never want to go back to that system. The BOI's courtesy, professionalism and lack of corruption has made all the difference. Plus I now have a 10 year visa, no 90 day extensions, 5 year stay that's renewable, 5 year work permit, and tax benefits.

-

1

-

5

-

2

2

-

1

-

8 hours ago, oldcpu said:

What means clarity and whose clarity? I believe the saying This Is Thailand applies here.

BoI (Board of Investment) for Thailand are clear - no Thai tax on remitted income for some LTR categories. ie Exempt from Thai tax on remitted foreign income are Wealthy Global Citizens, Wealthy Pensioners and Work-from-Thailand Professionals (while the Highly-Skilled Professionals category pay 17% Thai tax on remitted foreign income (if not protected by a DTA)).

However ... in practice ... in Thailand ... the 'devil can be in the details' ... or in how this is (or is not) applied.

One of the users on this forum, noted they called a Thai Revenue Department help line and asked that very question about LTR visa being exempt from Thai tax and the Thai tax calculation. My recollection, after a bit of waiting (while the Thai Revenue Department person answering the help line went to check) they subsequently received a verbal answer that there was no Thai tax on the noted selected LTR visa holders remitted foreign income to Thailand.

Now - having typed that, an official at a local RD office where I live, never heard of the LTR visa.

Further, a user JackGats, on this forum, who has an LTR visa, reported on this thread he ended up having his remitted income in 'essence taxed'. If I understand his post correctly, at a local RD office (when he filed a tax return) the local RD official used JackGat's foreign remitted income to Thailand, to cancel out his request to have a refund of the withholding tax on his interest from a Thai bank. ... Which in essence means he was taxed equal to the withholding tax refund he had coming to him. My understanding this was from a LOCAL RD office (and not the main RD office in Bangkok).

My view is each local RD office quite possibly goes their own way here.

What is encouraging thou, is the main RD office in Bangkok, have been clear no Thai tax on remitted income for selected LTR visa holders. ... Its just some local RD offices either do not know of the LTR visa, or they see the tax situation differently (than the main Bangkok RD office).

As I noted, This is Thailand. That can often mean 100% clarity is an elusive thing.

Hi, just to clarify - I have the LTR-H visa - unfortunately the 17% tax rate is only for salary income earned in Thailand. Foreign remitted income does not receive any tax break. (From BOI LTR unit).

Also as I understand it, under the other LTR visas any income earned while working in Thailand, whether the salary is paid in Thailand or paid overseas, is taxable at the marginal rates in Thailand - it isn't considered "foreign income." It is considered income earned from working in Thailand. So it doesn't matter if this income is remitted into Thailand or not, it is still taxable at normal Thai tax rates when it is earned. It is only passive income (income that is not from working, such as interest, dividends, capital gains, etc) that qualifies for the foreign remitted income exemption. (From discussions with tax professionals)

-

1

-

1

-

-

Yes, I've needed a TM30 for each of the following:

Transferring LTR visa to new passport

Certificates of Residence for all the following: getting a new international drivers license, buying a car, selling a car

-

2

-

-

On 3/21/2025 at 12:35 AM, Jangunnim said:

LTR doesn’t even have a path to PR or citizenship, yikes… with those requirements you would kind of expect something but apparently not lmao. I don’t know why I assumed in my mind that of course it would have some path because they even have own section for it in chamchuri and now in the one Bangkok I guess. But they hawking a 10 year tourist visa

No, the LTR visa couldn't be more different from a tourist visa. It's a visa that allows recipients to work, so it's a business visa, except better in so many ways. No need for 4 Thai employees, tax benefits, no messy, exp and time consuming annual renew as its for 10 years, and the BOI is not corrupt etc etc

-

1

-

-

- Popular Post

2 hours ago, mran66 said:Preparing for my application and reading what they have on their website. Saw this:

"The LTR visa stay permit is granted for a period of 5 years upon initial entry into Thailand; however, its validity is strictly limited to the expiration date of the passport"

If I understand this correctly, the validity starts after first entry to Thailand, however if I am already in Thailand, does it start when it is issued? If not, when?

Also, as my plan is to get the visa issued to my old passport expiring end of this year, and then get a new passport when visiting home country in summertime, I assume I can enter the country with new passport, showing the visa in old passport, and then have the visa transferred to new passport when here(?)

I received the LTR visa in country, and the validity of the 5 year period permission to stay started on the day I received the visa, and ends when my passport expires next year.

I plan to get a new passport from my embassy while in Thailand. The LTR unit said once I have the new passport, I'll receive the permission to stay through the 5 year date from when I received the LTR visa. It'll be shorter than 5 years at that point, however, since I received the LTR visa some time ago.

-

3

-

19 hours ago, John207 said:

Thanks for your input. When I reentered Thailand in January, the immigration officer stamped me in with a two-month validity which I didn't notice. However, when I reentered Thailand just a few days ago, the immigration officer pointed out to me that his colleague had made a mistake, and I was stamped in till January 28. I suppose that should resolve the issue.

Just to be sure, January 28 of what year? When re-entering, the IO has always stamped an "Until" permission to stay until 5 years from the day and year that I received the LTR.

-

13 minutes ago, DrPhibes said:

If you open a bank account using your Thai ID in the US, that US institution will report your info to the Thai gov. If you opened an account in your US passport in Thailand, that Thai institution will report your account to the US. They don't make any kind designation as to residency for you.

are you saying "how will they know"

-

19 hours ago, DrPhibes said:

Yes, there is a 2 way exchange of information. For the US, they report the information of Thai residents that hold US accounts to the Thai gov. For the Thai side, they report the account information for US residents to the US gov. The US does not report information of accounts held in the US by US citizens to the Thai authorities. That is tier 1 FATCA reporting.

That would be good to know, if true. Could you provide a reference from the agreement saying Thai residents who are also US citizens are exempt from US information sharing?

The Thailand-US IGA is a Model 1 agreement.

https://home.treasury.gov/policy-issues/tax-policy/foreign-account-tax-compliance-act

-

4 hours ago, DrPhibes said:

But since the US does not participate in CRS, the Thai government is not receiving any info of my accounts in the US. Just reports my single Thai account to the US under FATCA rules. That account is now receiving only US social security money since the 1st of this year from my wife, underage child, and I. Way more than enough for our Thai needs and wants. Not special, just different.

The Thai government should now be receiving information on accounts in the US.

Although the Thai-US FATCA IGA was signed in 2016, it only came into force last year. The IGA includes reporting obligations that go both ways (Thailand to US, and US to Thailand). Specifically Article 2 of the IGA, item 2b explains about what US financial institutions need to report to Thailand. https://www.mof.go.th/th/view/attachment/file/3134303034/FATCA_IGA_Us.pdf

-

2

-

Joint tenants with right of suvivorship

in US & Canada Topics and Events

Who is dying? If it is you, after your death, your estate receives the US estate standard deduction that all US citizens receive, i.e. $13.99m in 2025.

Or are you saying your wife who is a non US citizen/non US domicile is the one who is dying? In that case, her US asset estate would receive the $60k deduction if she leaves her assets to anyone who is not her US citizen husband.

I am actually trying to help you, and unfortunately you're misinterpreting online information. This is a complicated area, and your best bet would be to hire a US estate lawyer directly and not try to do it yourself with online information. Have a good day!