Mike Teavee

-

Posts

4,306 -

Joined

-

Last visited

Content Type

Events

Forums

Downloads

Quizzes

Gallery

Blogs

Posts posted by Mike Teavee

-

-

49 minutes ago, JeffersLos said:

Why a minivan? Why Cambodia?

Anyway. Drive your car or ride your motorcycle to a border, maybe 500 baht in gas. Burma, Laos, Cambodian or Malaysian visa, whatever price that is, say 1500THB average. 2000THB give or take. Forget getting extensions at immigration. Just do the road trip once every 2 months, cost approx 1000 baht a month.

It wouldn’t surprise me if they start forcing people who do back-2-back 60 day visa exempt entries to spend at least one night outside of Thailand (have seen it mentioned that DTV holders cannot come back same day) so a Visa Run company might end up more convenient/cheaper if they can help you get back same day.

-

Just now, chiang mai said:

I'm uncertain but believe it should remain true because the pension disbursement has not yet started.

Logically UK Gov says your pension will be based on the date you reach State Pension age or the date you move abroad if this is later, which could be taken as if they know you were living overseas before hitting SP age then it would be frozen as at SP age.

Practically I'd expect them to not even check & just start paying you whatever the differed pension was & freeze it at that.

-

2

2

-

-

52 minutes ago, chiang mai said:

I agree with this. The annual increase remains in effect, until such time as you decide to take the pension, after which, the issue of frozen or unfrozen arises, but not before.

Is that still true if HMRC & DWP both know that you're non-UK Resident (in my case HMRC know from my annual Self Assessment Filing & DWP know as I was paying Class 2 AVC/NICs on the basis I was working overseas).

-

I just completed this quiz.

-

My Score83/100

-

My Time49 seconds

-

-

1 hour ago, rwilem said:

Was scrolling on facebook yesterday and was treated to a sponsored post from an agency/outfit in Bangkok. Big and bold announcement dedicated to announcing their '90-day reporting service' for foreigners.

Not that I'm interested, I do my 90-dayers myself. but I did see the price for the service. 1000 baht is lowest, and seems there are a few price tiers.

Not sure about linking policy, mods can remove it if not kosher, I'm just adding it for info purposes.

https://www.ptservicesagency.com/en/thailand-90-days-report

Wow, as per the link I posted above, Asia Visa Tour advertise 380B for a 90 day report & I pay 1-200B in Pattaya but to be honest even 1,000B feels cheap when the alternative is a 1.5 hour each way trip to CW.

-

1

-

-

- Popular Post

- Popular Post

12 minutes ago, lapamita said:no undertsand

everybody posting diffrent thing

question can i go ou tand in as long i want same with NON O multiple )in this case max 180days) ,,,valid for unlimited entrys .. easy yes or no

one posting no , other yes

YES...

Every time you enter you will be given 180 days permission to stay, if you want to stay longer than this you will need an extension but you can not stay more than 360 days without leaving the country.

Once you leave the country, come back the next day & you will be given 180 days again... Rinse & Repeat for 5 years.

Edit: Rough Schedule (I'm assuming 30 days per month every month, it's just a rough schedule).

- Jan-June In Thailand then make a decision, extend for 180 days or leave Thailand for at least 1 night

- July-Dec In Thailand then If extended last time, need to leave Thailand otherwise can choose to Extend or leave for at least 1 night

- Jan-June In Thailand then If extended last time, need to leave Thailand otherwise can choose to Extend or leave for at least 1 night

- July-Dec In Thailand then If extended last time, need to leave Thailand otherwise can choose to Extend or leave for at least 1 night

Etc.... for the 5 years.

-

1

-

2

2

-

1

1

-

8 hours ago, Cuchulainn said:

Yeah, but it says to report in person after re entering.

Mail in accepted?

Have you tried asking one of the Agents to do it for you? The one I use in Pattaya charges 100B for a 90 day report & I know you can do it via an Agent after re-entry as I got back from the UK in May, got a new passport end of July & my agent did my 90 day 1st week in August.

I used Asia Visa Tours to do my 90 day report when I lived in Bangkok (This was pre-Online system being usable & they had an office on the ground floor of my Condo building), their main office is on Suk Soi 24, 3 min walk from Phrom Phong BTS https://maps.app.goo.gl/fvUGSJhW5mywps3a7.

Just checked & they charge 380B (https://www.asiavisa.net/複製-業務内容), which was a lot cheaper (& less hassle) than a round trip to CW from On Nut.

-

1

-

1

-

-

- Popular Post

- Popular Post

12 minutes ago, lapamita said:/ is that true??

can not multiple go in and out of country ??

bcs i minimum travel 6 time a year in and out ????

true ??

No it's not true, you get 180 days permission to stay on each entry after which you can extend (1 time on that permission to stay) or leave the country for 1 night & come back for another 180 days.

Technically (assuming you do 180 Days + Extension then one night out of Thailand & repeat) you would only need to spend 1 night out of Thailand in any one 360 day period for 5 years.

-

2

-

1

1

-

3 hours ago, Zyxel said:

It looks like it's about to tell you you're in Slytherin...

-

1

-

1

1

-

1

-

-

1 hour ago, Jumbo1968 said:

Out of interest why would you pay CGT on your U.K. property after selling it ?

Because it's not been my "Primary Residence" since I moved overseas in 2008 & I've been renting it out since 2010.

-

1

-

1

-

-

47 minutes ago, Cuchulainn said:

But then it must be done in person at CW. I'm hoping to avoid that.

My cunning plan (Baldrick!!) is to stick with current 90 days reporting irregardless of leaving country and hopefully avoid a trip to CW

The online site asks you for your last date of entry into Thailand so you'll either need to leave it as the old date (and risk it being rejected) OR update it & trigger an automatic response that says you need to report in Person (at least that's what I got when I tried mine a couple of weeks back).

-

1

-

-

45 minutes ago, sometimewoodworker said:

The advice of a tax consultant was not predicated by any idea of hiding the source of the required 250k but an expert opinion as to if it would class as assessable or not assessable for Thai taxation. It is an uncommon source and could easily be seen as either. If the opinion is that it is not assessable that would obviate the requirement to be non resident when it is paid out.

I am almost certainly going to be non resident for 1 tax year because I have a significant capital gain to realise and capital gains are certainly assessable.

Agree 100% & I'm giving serious thought to selling my UK House that same year which would raise Capital Gains that would certainly be assessable (Even after the CGT I would need to pay on it in the UK) but I also believe that, currently, the Tax "Experts" have no more information than us laymen so (personally I) wouldn't consult one until the situation is much clearer (I don't need to make a decision until 2026 so happy to sit back & see what happens).

As an aside Thailand's visas have changed so much in the past 6 months It would be silly of me to decide exactly what I'm going to do in 18 months, the LTR could (I'm not for 1 minute suggesting it would) lose it's "Tax Free" remittances or the Non-IMM O could morph into a 5 year Visa/Extension With tax free remittance of pensions (Which to me makes absolute sense for guys from a country that Thailand has a DTA with).

But the plan at the moment, is to do an Hotblack Desiato in 2026 🙂

-

3 hours ago, sometimewoodworker said:

However if it is only for that reason that you want to be nonresident you may find that a professional tax accountant’s opinion is less expensive.

My main reason for bringing the money over is as a $250K "Investment" to support my application for an LTR Visa so a Tax Firm being able to "Hide" this remittance for me wouldn't help.

I can show an income of >$40K pa today, but I need to invest the $250K to get the visa & my PCLS will get me there (or at least close enough where I can make up the difference from money I'm currently not remitting to Thailand because of these tax changes - sincerely hope they wake up & realise that people are not bringing money in because of the current tax situation).

-

25 minutes ago, treetops said:

One thing not taken into account which may affect things is that many UK pensioners using pension drawdown will be taking part of their monthly income from the tax free allowance of 25%. This will reduce the UK income tax they pay and depending on the amount taken like this may or may not push them into the position where they will owe tax to Thailand.

Agreed, some people's circumstances are going to be different (e.g. somebody may have additional allowances in the UK & their UK tax paid would be lower that the numbers I quoted) so it's important to use the actual Tax paid in the UK & not the numbers that I gave but hopefully the examples give people a feel for what their Thailand Tax Liability would be.

It will be interesting to see how the 25% tax free allowance from UK Pensions are treated. Will TRD treat it as income that has had no tax paid on it (probably as they're unlikely to understand what it is) or will they make some allowance to exclude it from assessable income (Highly doubtful) - I'm on a Defined Benefits / Final Salary pension and when I take my PCLS (25% Tax Free Pension Commencement Lump Sum) it's a one shot deal so I'm planning to be non-Thai Tax resident that year.

-

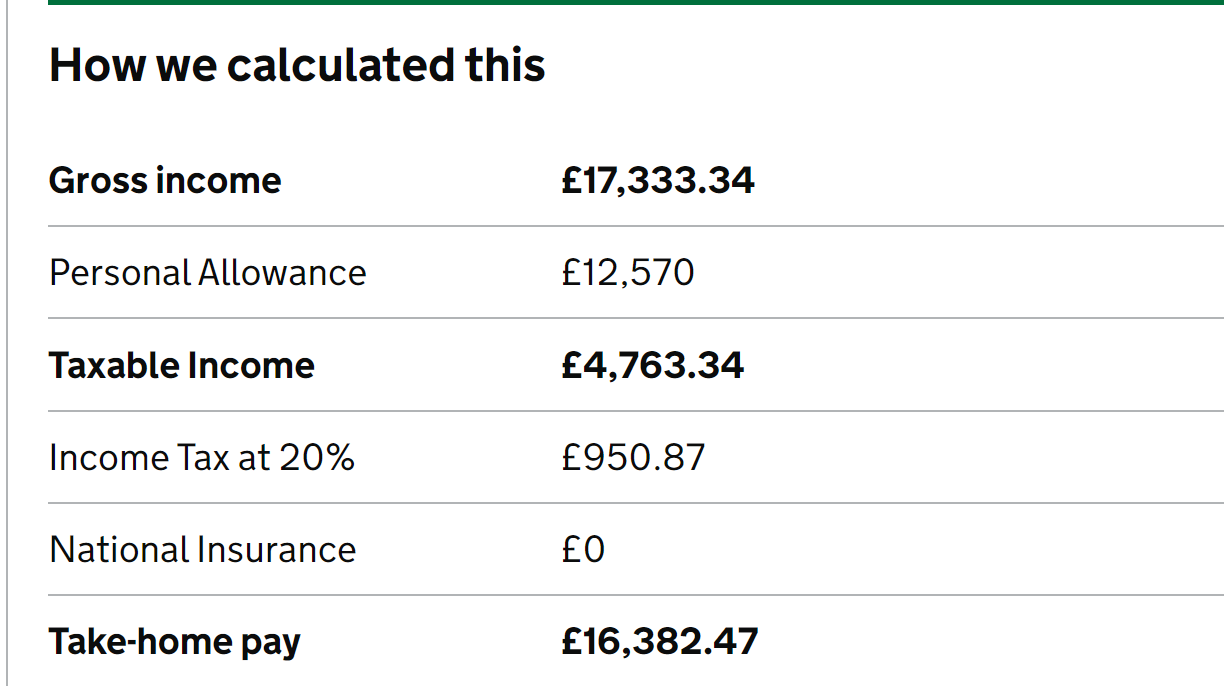

1 hour ago, topt said:

Apologies Mke but just for accuracy what figure did you use for the PA as I get a couple of pounds difference to your UK tax paid numbers?

Thanks

I used HMRC "Estimated Take Home Pay" calculator... https://www.tax.service.gov.uk/estimate-paye-take-home-pay/your-pay which has the 2024/25 personal allowance at £12,570...

Using the 65K pm / £17,333.34 pa example...

[No NI to pay as I clicked the link saying "Over the State Pension age"]

-

1

-

-

- Popular Post

- Popular Post

1 hour ago, Mike Teavee said:I don't believe you'll get caught either but that doesn't mean that you're vindicated, it just means you got away with it & unless you're remitting >100K pm you're getting away with nothing as you wouldn't owe any tax anyway

Apologies I know it's bad form to quote yourself but out of curiosity I ran the numbers on a few scenarios & was surprised to learn that only people remitting Assessable (Non-Gov) UK pension incomes (NB I'm only doing the calcs on UK pensions as that's the topic of this thread) of approx. 42-49K pm would have any Thai Tax owing, below this & your TEDA + 150K @ 0% would cover you, above this and the Tax you've already paid in the UK more than covers any Thai tax due.

Basic assumptions, a Single person, over state pension age so has 355K TEDA (60K personal allowance + 195K >65 allowance + 100K allowance for "Expenses") and £1 = 45THB.

50K pm Income...

- Remitted income - 600,000

- Taxable Income after 355K allowance = 245K

- Tax due = 150K * 0%, + 95K * 5% = 4,750 Thai Tax

- UK Tax already paid on £13,333.34 = £150.87 = 6,789 THB which can be offset against the 4,750 to leave no tax liability.

65K pm Income...

- Remitted income - 780,000

- Taxable Income after 355K allowance = 425K

- Tax due = 150K * 0%, + 150K * 5% + 125K * 10% = 20K Thai Tax

- UK Tax already paid on £17,333.34 = £950.87 = 42,789 THB which can be offset against the 20K to leave no tax liability.

100K PM Income

- Remitted income - 1,200,000

- Taxable Income after 355K allowance = 845K

- Tax due = 150K * 0%, + 150K * 5% + 200K * 10% + 250K * 15% + 95K * 20% = 84K Thai Tax

- UK Tax already paid on £26,666.67 = £2,817.53 = 126,788 THB which can be offset against the 84K to leave no tax liability.

500K PM Income

- Remitted income - 6,000,000

- Taxable Income after 355K allowance = 5,695,000

- Tax due = 150K * 0%, + 150K * 5% + 200K * 10% + 250K * 15% + 250K * 20% + 1,000,000 * 25% + 3,000,000 * 30% + 645K * 35% = 1,490,750 Thai Tax

- UK Tax already paid on £133,333.34 = £46,203 = 2,079,135 THB which can be offset against the 1,490,750 to leave no tax liability.

... Obviously as you get higher numbers you're taxed 45% in the UK Vs 35% in Thailand so the difference between what you pay in the UK will be even greater than what you would owe in Thailand

Edit: And this is why I believe TRD will end up giving a "Pass" to things like UK Pension income as they know the effort involved in processing every return isn't worth the small amount (<3K) they would get from the guys in the 42-49K pm range.

-

1

-

1

1

-

3

-

2 hours ago, sandyf said:

I did acknowledge an alternative interpretation which you would have seen on my 2nd post.

However I don't see why anyone would feel compelled to try and prove a worst case scenario, unless of course they had a vested interest.

Taxation is a personal issue and I for one am not going to volunteer may state pension as taxable income unless someone with the authority to do so says otherwise. By the same token others are free to take any action they feel appropriate.

if it came to pass I never had to pay any tax I wouldn't assume vindication, just that you don't have to be a Lemming.

Nobody is trying to "Prove a Worse Case Scenario" we're just trying to explain the facts & if you believe differently then that's up to you.... I don't believe you'll get caught either but that doesn't mean that you're vindicated, it just means you got away with it & unless you're remitting >100K pm you're getting away with nothing as you wouldn't owe any tax anyway so it doesn't make sense not to include it IF you're filing a return anyway.

FWIW, I have no facts to back this up but honestly believe we'll see them giving a "Pass" to people who are only remitting pension income from countries like the UK where they know they've already been taxed (& I count the State Pension as already taxed albeit at 0%) & a DTA can be used to offset tax already paid against what's owed in Thailand but until then State Pensions are assessable income.

-

57 minutes ago, martyn1 said:

Thanks.

So this 800k deposit for retirement, which is required and I cannot touch it, has no special treatment and is just income brought into Thailand and subject to tax?

By July I meant if I come to Thailand in July and transfer and apply for retirement , I am not tax resident in given calendar year by 180 day rule.

There's been no announcements to say it would be treated any different than you sending any other money over (Same is true when sending money for a Condo purchase which you'd also think they would want to encourage0.

If you have spent no time in Thailand this year & came on 5th July then you would be non-Tax resident for the year so free to bring over anything you like... Obviously if you've already had a 2 week holiday here earlier in the year then the date would be pushed out to 19th July etc...

-

On 7/31/2024 at 11:04 AM, martyn1 said:

Will be 800k deposit taxed, if I stay more than 180 days? Or better to apply in July?

It doesn't matter when you apply, it matters how long you spend in Thailand in the calendar year you apply (Time in country on a Visa Exempt stamp counts as much as on any other Visa).

Whether it will be taxable or not depends on:-

- If you're Tax Resident (i.e. spend 180 days+) in the year you remit it - If not, no tax.

- What the source of that income was, E.g. if it's from pre 1/1/2024 income/savings then no tax.

- What it says in your country's DTA around income that's already been taxed (i.e. can you claim any tax paid in your home country as a credit against Thai Tax)

... For points 2 & 3 don't forget that you'll be remitting money to live on so this would need to be added to the 800K when calculating your total tax bill.

FYI, A Single UK guy <65 remitting 1 Million THB of assessable income that has already been taxed in the UK would be roughly tax neutral when it came to owing Thai Tax.

-

1

-

10 minutes ago, sandyf said:

Comes back to the question, does the UK have exclusive taxing rights on the state pension? The wording of the DTA would suggest it has.

I had "trivial commutation" at one time and if I remember right it was tax free.

You seem to be the only person that believes that & as several of us have posted information (including links to the DTA & Expat Tax companies) that says it's not true we'll have to agree to disagree, it's been argued enough in the other threads already..

I had "Trivial Commutation" once, Worked for EDS for a couple of months (Ironically at DWP) & had a small (IIRC the limit was/is <£10,000) pension that they were moving to another provider so I had the choice of taking it tax free... so I did.

-

1

-

-

8 minutes ago, sandyf said:

Read the 5th post on this thread.

Can you provide a source for that statement so we can understand it's context more....

Doesn't really matter as the DTA says...

Any pension paid by the Contracting State or a political subdivision or a local authority thereof to any individual in respect of services of a governmental nature rendered to that State or subdivision or local authority thereof shall be taxable only in that State.

So for the purposes of Thai Taxation, State Pensions are Tax assessable whereas "Government Pensions" like Military, Civil Service, NHS, Council Worker etc... pensions are not.

Edit: Playing Devils Advocate, State Pensions are mainly paid for out of Employer & Employee National Insurance contributions so where the Employer wasn't a Government department could be argued are not being paid for by the Government.

-

1

-

-

26 minutes ago, sandyf said:

Your are wrong. The state pension is taxable, not at source but lumped with other income to determine liability.

Why haven't you backed up this claim.

" but as things stand it is considered Assessable Income in Thailand."

Many seem to think they know the answers, but reluctant to substantiate.

Sorry, I didn't want to repeat myself from the post directly above the one you quoted where I said:-

State Pensions:-

- Are not considered a Government Pension, these are things like Civil Service & Military etc, not the pension of your average Joe.

- Are taxed, it's just that they're the 1st thing that's added to your total income so are covered by your Personal Allowance which is considered taxed at 0%.

The fact that they are considered assessable income has been discussed many times (too death) in the other Tax threads but here's a Q&A from ExpatTax... (Search for State Pension)...

Potentially, yes. This is dependent on the tax rate in the UK and if it was remitted into Thailand. State and private pensions in the UK are taxable in Thailand, but you can use tax already paid as a credit. Even if your tax rate is high in the UK, and even if there is no tax to pay in Thailand for your situation, you will still have to file a tax return.

Both your state pension And private pensions are classed as assessable income If you transfer To Thailand. You will likely have To file a tax return. Our Assisted Tax Filing Service will help you to claim the tax credits for tax paid In the UK. This is called assisted tax filing. Click here to learn about foreign sourced assessable income.

Show me where it's not-Tax assessable & if you can't then by default it is Tax Assessable. #

-

2

-

Just now, sandyf said:

That is to do with the Social Security Act, not the DTA.

Only a certain mentality would believe that when the DTA was drawn up that the UK would give up the right to be the sole beneficiary of the tax collected on the UK state pension.

The UK has 1st dibs on taxing State Pension (but as it's below the basic personal allowance doesn't get anything from it) so they're not giving up any rights. I'm sure if they were to update the DTA today, State Pension would be exempt but as things stand it is considered Assessable Income in Thailand.

-

1

-

-

State Pensions:-

- Are not considered a Government Pension, these are things like Civil Service & Military etc, not the pension of your average Joe.

- Are taxed, it's just that they're the 1st thing that's added to your total income so are covered by your Personal Allowance which is considered taxed at 0%.

All of that is irrelevant to the OP though as the UK tax he's paying on the equivalent of 80K THB pm would be higher than what he would owe in Thailand & the DTA means he can offset UK Tax on income so nothing to pay.

I did the maths on 84K pm for somebody who only had the 60K personal allowance & 100K "Expense" allowance & it came to <1,000 THB owed, the fact that his military pension is not Taxable in Thailand means that he's way below the point where he would owe Tax here even without his other allowances (e.g. the 195K > 65 allowance).

-

1

-

1

Wise transfers!

in Cryptocurrency News

Posted

Was it to Bangkok Bank?