oldcpu

Advanced Member

-

Joined

-

Last visited

Everything posted by oldcpu

-

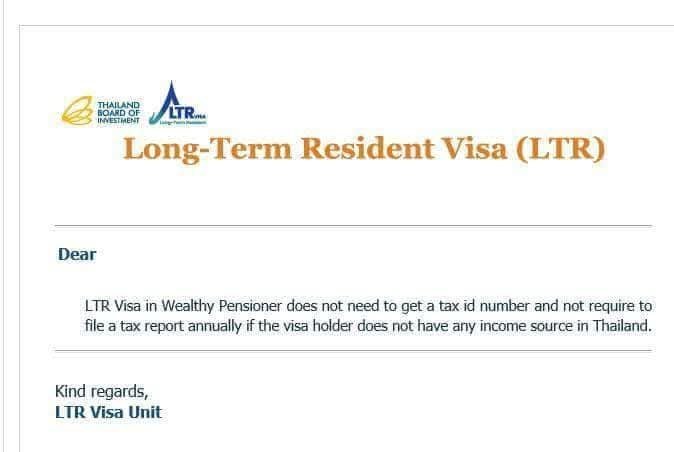

I saw this on a Facebook LTR visa page, where i believe an LTR-WP visa holder contacted BoI and asked if they needed to obtain a Thai TIN and file a Thai tax return.

-

A quick look suggests that article references POR.161, which was later clarified more with POR.162. Further, note that articles massive qualification statement: With regards to the Thai Enquirer article stating "exempt will be those who have been taxed in a foreign country that has a standing Double Tax Agreement with Thailand" that is IMHO a simplification to which most agree it is a simplification. Its more complex that that I believe. In the case of some DTAs, both Thailand and the source-country of the pension (for example), can tax the pension. In that case, one is into tax returns and tax credits (unless one has an LTR-WP, LTR-WGC, or LTR-WFTP visa). In the case of some other DTAs, only the source country of the pension can tax the pension (or similar remuneration) - where in this case countries such as Canada (with its DTA with Thailand) and other country's civil service/military pensions only being taxable in the source-country. In that case, if no other income, there is no need for TIN nor tax returns. And in other cases (Germany springs to mind) only Thailand can tax a German state pension (by state pension I mean NOT civil servant/NOT military) and not Germany tax the state pension. In that case such state pensions if received after 31-Dec-2023 and if remitted to Thailand are to be taxed in Thailand (also only if Thailand taxation threshold exceed). Further complications are tax return filing thresholds ... and of course presence of an LTR-WP, LTR-WGC and LTR-WFTP visa plays a factor. So its very DTA specific here as well as there being some other factors. ... and add to that a paranoid view by some who (IMHO) incorrectly claim that a TIN and Tax Return is needed still, despite the Thai law making it clear in some cases that DTAs (as called up by Royal Decree-18) can make it clear some pensions are exempt Thai tax and hence in some cases legal that no Thai tax return need be filed. Ergo lots of confusion, not per se due strictly to Thai RD, but rather due to the paranoia (although the paranoid may call it ultra conservatism) on this forum.

-

That's an interesting interpretation. Not one I expected, but one I would be happy to see. I suspect most of use with trading accounts that are a mix of cash and equities, have a 31-Dec-2023 record as the total value (cash + share price at close business 31-Dec-2023) of our savings. I believe this and all subsequent trading / cash records then need to be kept, if desired to show subsequent remittances to Thailand came from the pre-1-Jan-2024 amount..

-

That Carden assessment begs the question ... why would the Thai RD NOT put a location on the Thai tax form if it was necessary to provide such information. No where in the Thai tax guide , that I could see, requires that. ... I am very suspicious that an unnecessary requirement is being pushed forward to try and raise money for a tax advisor office (to get expats to obtain TINs and file tax returns through such offices, when such is not a requirement for some (as confirmed by local Thai RD Tax offices - and the Thai RD helpline)).

-

Yes ... they might ... and they might not. From the experience of many at the local Thai RD offices (and from the main Bangkok RD help line) there does not read to be much interest in the Thailand RD in going after foreigners to prove such remittance source ... much much much less would be Thai immigration caring whether one has filed a tax return. Who knows? We will just have to wait and see. My view is to follow Thai tax law. Also take note of relevant Minsterial Instructions and of relevant Royal Decrees and of DTAs. Check if legally required to file a tax return noting NOT ALL INCOME is to be considered when evaluating the threshold to file a Thai tax return (in consideration of Royal Decrees, DTAs , and Ministerial directive). i suspect (hope?) with time, there may be superior summary information IN ONE LOCATION with regard to foreign sourced income (taking into account Thai tax code, the country of source income, DTAs, Ministerial Instructions , and Royal Decrees). At present one has to consider all and make an evaluation, as opposed to just one place/document.

-

Thanks. For anyone reading, my understanding is only health insurance from the Thai branch of a health insurance company can be used in the Thai tax return as a deduction. That surprises me a bit. This can be VERY different dependent on the source country of the pension. For example, Canadian sourced pensions (and similar Canadian sourced remunerations) are NOT taxable in Thailand (and not to be included in Thai tax calculations) per the Thai-Canada Double Tax Agreement. But German state pensions (ie non-civil-service/non-miliary) pensions can ONLY be taxed in Thailand (if one a Thai tax resident). The source country and type of pension (civil-service/miltiary or every day citizen pension) can make a BIG difference per international agreements Thailand has agreed to (per Royal Decree-18). Also that is of interest. Typically there is a 15% with holding tax on your interest in a Thai bank account. So you may have already paid some Thai tax which is why that was considered !

-

My speculation is simply keep enough paperwork to prove the paper trail of the government (civil service or military) pension ) coming to Thailand (even if via another bank) and also keep enough paper work to credibly show your state pension (ie NOT civil service pension nor military pension) credibly did not come into Thailand (perhaps via showing the savings accumulating in the foreign bank or that state pension being spent outside of Thailand). You may need to do a bit of extra paperwork as a backup 'just in case' ever queried to show the money trial (although IMHO such need to show is highly unlikely - but easier to do with transfer information is relatively 'fresh').

-

I also find the 'state' pension terminology confusing (it is not used in Canada either to the best of my recollection). My understanding is on this forum, when many say 'state' pension they mean the pension that most every citizen of a county gets if they (and/or their employer) contributed to their country's pension system. And when they state 'government' pension, many mean a civil servant pension and/or a military pension. As i noted before, all Canadian pensions (and similar remunerations) are taxable ONLY in Canada (and not in Thailand). On the otherhand, Germany is the exact opposite, where my understanding German 'state' pensions (ie the one every German resident gets who contributed to the German pension system for a sufficient number of years) is taxable only in Thailand. ... I can't recall off the top of my head if a German government pension (ie civil servant/military) is taxable in Thailand.

-

I assume your health insurance is from a local Thailand branch of a health insurance company? is that correct? Is your income local (earned in Thailand income) or a pension from another country? May I ask which country? and is your pension a government pension (ie that of a civil servant or ex-military) or is a state pension (one that every citizen gets if they contribute to their county's pension system)?

-

Well, the Thai RD, when contacted, disagree with you. OK. They disagree with you So you think you know better than the Thai RD and Thai tax law, ehh ? I don't think so. There is no need to go court when one is 100% compliant with Thai tax law, according to the Thai RD. Ohh ... you mean go to court for the KhunHeineken countershuffle? Ha ! Now that is funny. Ohhh ... apologies ... I forgot ... you think you know better than the Thai RD.

-

The tax free threshold uses assessable income to determine the threshold. Those expats whose income is exempt Thai tax due to a DTA don't need to include such in threshold calculation and hence don't need a TIN ( if no other income puts them over the threshold) nor do they need to file a Thai tax return. Unlike you, I do know a number in that category. If you don't know many, perhaps you need to get out more. It is important expats understand the DTA of their income source country has with Thailand to assess if their income is excluded from Thai tax, or taxable in both the source country and Thailand, or if such income only taxable in Thailand.

-

Absolutely and Thai RD confirmed. NO TAX on remitted foreign income for LTR visa holders. NO CAVEATS in that confirmation by the Thai RD. (Edit - I refer specifically to LTR-WP, LTR-WGC, and LTR-WFTP visa holders) That information has been posted a number of times already on this forum in different threads.

-

And a phone call to the Thai Revenue Department will remove that incorrect interpretation. One of our forum members checked with the RD tax department. No tax on remitted forum income for LTR visa holders. The Royal Decree is worded that way because when filing annual Thai tax returns one is always referring to the previous tax year. However those tax advisory companies don't want to go the extra check to confirm their error (by contacting the Thai RD). Why? Because clarifying is not in their financial interest as they may lose a potential frightened LTR visa holder as a client, where the LTR visa holder (and the Tax Advisory companies) did not bother to check with the Thai RD help line (or read the Forum user's post who noted what the THAI REVENUE department confirmed) (Edit - I refer specifically to LTR-WP, LTR-WGC, and LTR-WFTP visa holders) Some seem to take a joy out of posting misinformation - without taking the time to check themselves. .

-

And if you paid attention in the video, the word assessable income was later noted.

-

Not much stated in that video for the aspects most of us are discussing. The hard questions were not asked/emphasized. Why you even posted that, given what it lacks to clarify, is a puzzle to me.

-

In regards to the quality of hospitals in different South East Asian countries. Singapore and Thailand have the best hospitals. After that, in order of decreasing quality are Malaysia, Philippines, and Vietnam. So if leaving Thailand, but staying in South East Asia, that may be a consideration.

-

He read only part of the law. He cherry picked a small part. Then he then deliberately ???? ignored other salient parts of the Thai tax code. Why? Why? Why ignore such? Why would that youtube blogger NOT quote other salient parts of the Thai tax code that others on this forum have pointed out? Inquiring minds want to know.

-

So you believe him over (1) local Thai RD officials from different provinces (where the RD HQ in Bangkok has delegated the assignment of Thai TIN to the local provincial RD officers , and you believe him over (2) Thai experts from the Thai RD help line, who made the time and effort to double check the questions asked, before answering. Just another youtube blogger trying to drum up business. That may be. I don't know. But what I do believe, is most living here should be given good advice, and not inaccurate advice pushing them to file a tax return if it is not needed. Again , it needs to be assessable income over the threshold. We are 100% in agreement there. .

-

Anglo Siam Legal ehh?? The Anglo Siam Legal rep really needs to talk to the Thai RD and get their facts straight. If they did, they would have learned that getting a TIN is for a tax resident and filing a Thai tax return is for a person who is "liable to personal income tax". Clear enough ? Clear? Ok , what does "liable to income tax" mean? I will tell you. It means enough assessable income. Clear? OK ? Does Siam Legal mention that? No? Why not? Inquiring minds want to know. Also, noted in that video at the start Anglo Legal claim " Invited for comments, but then comments are turned off. So video says onething, and Anglo Legal does something else". They turn off the comments despite inviting comments. Why? Lol !! Lol !!! Why is that? My guess? They don't want their mistakes pointed out to them. So .. let us go further. Now , lets say one applies on line for a Thai Tax ID Number (TIN). What happens there? Let me tell you. The online application goes to the RD tax headquarters in Bangkok. What does the Head office (Thailand's tax experts from the RD) in Bangkok then do? Guess what? Bangkok will not assign a TIN for another province. OK? Clear? Crystal clear. Right? Clear for you now I hope. So Bangkok forward such applications to the provincial RD to assign a TIN if required. The provincial office determines if one is a tax resident, and determines if one has sufficient assessable income (making one 'liable for personal income tax') . We have many cases that the provincial RD tax office refused to provide a TIN due to the expat not having enough assessable income and hence is not "liable to income tax' per Thai law. More of the KhunHeineken countershuffle in action.

-

No ... the response is the "KhunHeineken countershuffle". Better than relying on your posts .

-

EXACTLY WHERE in the video. I am not going to waste my time going through yet another video unless you point out the exact time. I already pointed out local Thai RD (more than just one rogue RD tax department) have stated for some no TIN will be provided and a tax return not required (for those tax residents specific financial situation). I have already pointed out a Thai RD help line stated no tax return required for those whose assessable income is too low. And all you have is a video where you can not even point out exact time where allegedly what you claim is the case? Pathetic.

-

Decades eh ... pure exaggeration on your part. ... Plural , no less.

-

Really ? Decades? Are you certain on that? EDIT: I vaguely recall it was much lower in the 1990s, and only changed some time after year 2000.

-

So what ? The Thai RD is quite public that they work on a system where the tax resident needs to evaluate if they have sufficient assessable income to file a tax ID. My suspicion is if we are talking ENORMOUS amounts of money, or if the Thai RD has other reasons to check up on a person, they will they bother to check up on those who legally do not file a tax return. You and I have very different views here. Mine are backed up by a local Thai RD. Also backed up by a forum user who phoned the Thai RD help line. Your view? Maybe at most backed up by your speculation, and the youtube videos of some Tax advisors who are possibly hoping to generate income by frightening some to submit tax returns when legally NOT required. I know whose view I am going to follow. .

-

If doing nothing would cause problems downstream, why would a number of Thai RD offices tell the foreigners who are tax residents that given their circumstances they (1) did not qualify for a Thai TIN, and (2) did not have to file a Thai tax return. .