JimGant

-

Posts

6,619 -

Joined

-

Last visited

Content Type

Events

Forums

Downloads

Quizzes

Gallery

Blogs

Posts posted by JimGant

-

-

1 hour ago, oldcpu said:

Those forms do NOT appear to be intended for any LTR visa holder other than the LTR Highly Skilled Professional

Yeah. My quote was from the Expattax folk's FAQ page -- which, I've found, has a lot of questionable observations. But, hey, they do start out their webpage with the disclaimer: "The information on this website is for informational purposes only and is not professional tax advice." So, maybe they're honest, if not dependable. Hey, they're the ones who maintain pre 2024 income, to be non assessable when remitted, must only be from a savings account. Chew on that for awhile.

-

25 minutes ago, Jingthing said:

But that is an opinion and if you're not a Thai tax lawyer how much power does that have with Thai Revenue?

...still waiting to see something official from TRD that says that Por 162 pre 2024 income must manifest itself only as bank account savings, in order to be exempt from Thai taxation. Absent that, I would submit you're free to choose the avenue that provides the best outcome for your remittance of pre 2024 income. Because, absent that, you've got a solid argument in any audit scenario. Worst case, if you lose -- 'cause your solid argument certainly gives you credence against a tax evasion charge -- is pay the taxes owed, with interest. Having said that, if you do decide to not declare these pre 2024 monies on a Thai tax return -- there's nothing there for TRD to peruse as a potential audit -- since there are no line items for non assessable income. Thus, chances of an audit for a nil line item is zip; only if you're caught up in a random compliance audit would -- MAYBE -- they would ask about non declared, non assessable incomes. Hey, weigh your odds of an audit -- and what's the worst that could happen if somehow your pre 2024 income remittances didn't stand scrutiny.

Up to you. No brainer, IMO.

-

1

1

-

-

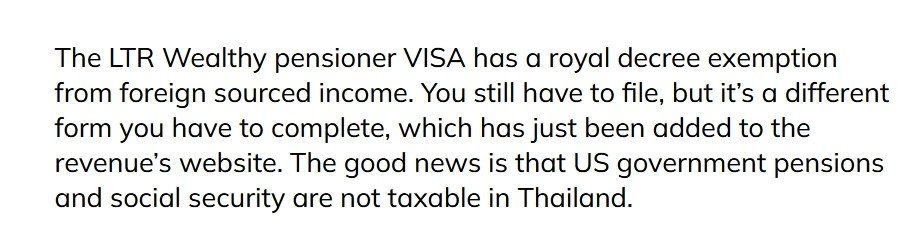

Does anyone know anything about this, from the Expattax FAQ page, where they say there's now a new form you have to file for Royal Decree exempted income:

-

1

1

-

-

1 hour ago, chiang mai said:

Yours is the best and most convincing evidence to date that it is exempt, thank you for saving everyone from wasting time with home grown arguments.

Ah, so now pre 2024 income, to be non assessable per Por 162 -- doesn't just have to be from a savings account -- but can also be from a Roth IRA. Good catch.

-

1

-

1

1

-

-

- Popular Post

- Popular Post

18 minutes ago, Jingthing said:That is about money in the bank

Says who? Expattax alludes to this. So does Chiang Mai, on this forum. I can't find any TRD backup for this. If I could, I'd withdraw all my arguments. But to say, all that pre 2024 income must be held in a savings account, in order to be non assessable from Thai taxes, is ludicrous. Look at Por 162 again:

QuotePOR 162 says that the assessability of foreign income earned before 31/12/2023 shall not be enforced.

How does that translate into: To comply, that income must be held in a bank account. Maybe logic would say it must be held in a financial account, allowing for liquidity or near liquidity (for whatever that's worth). But certainly, if liquidity was a requirement, I'd be allowed -- to realize greater interest -- to move that income from a savings account, to a brokerage, or to buy CDs -- or to an IRA account, to have US taxes deferred. Certainly TRD isn't putting out restrictions on what I can earn from where I park that pre 2024 income..... Somebody's certainly misinterpreting what they thought TRD said about: Must be kept in a bank or savings account. Or TRD is bonkers..... (rhetorical).

Anyway, I have an LTR visa, so this discussion is moot. But for Jingthing -- it won't likely make a hill of beans whether or not your IRA remittance is covered by Por 162, or not. If it is, then Thailand can't tax it -- but the US taxes it in full, without any Thai tax credit deductions. But, if Por 162 isn't a player, then the DTA takes full affect -- and Thailand has primary taxation authority on your IRA remittance -- but because of the saving clause in the DTA -- the US has secondary taxation rights, but has to absorb a tax credit for the Thai taxes. Bottom line: Only in the latter example, if Thai taxes exceed US taxes, will your total tax bill exceed US taxation only.

-

5

-

31 minutes ago, Ricohoc said:

An end of year statement from my US bank will confirm funds held (millions of baht) in savings. As long as savings prior to Dec 31, 2023 are proven by bank statement, they're savings and not taxable under the current information.

Amen

-

1

-

-

37 minutes ago, Jingthing said:

While not exactly pensions by US definition, my current understanding is that TR classes them as PENSIONS and sadly not exempt under the DTA as social security is

But Por 162 says pre 2024 income, which is what IRA consists of, is exempt from assessable income. That its payout is categorized as a "pension" is neither here nor there. Now, without Por 162, yes, that IRA payout would be subject to primary taxation authority by Thai taxation. But, Por 162 overrides this.

-

1

-

-

27 minutes ago, Jingthing said:

You're missing that IRAs and 401ks are not bank accounts.

So what? "POR 162 says that the assessability of foreign income earned before 31/12/2023 shall not be enforced." The value of your IRA/401k on 12/31/2023 consists of foreign income earned before 12/31/2023 -- irregardless of what shape or form that income now exists (stocks, bonds, whatever). That this income is not in a bank account is totally irrelevant.

-

1

-

-

3 hours ago, chiang mai said:

I'm a Brit and am aware of Jim Gant's views on Roth and IRA's. I think there are issues there that are unclear/uncertain and I have fielded a question to Jim regarding valuations but have not yet read his reply.

Haven't seen that question -- please resend. Thanx.

-

8 minutes ago, chiang mai said:

In practical terms it has to be so. We're back to this valuation of assets on 12/31/23 again and the next day effect of commingled funds.

I don't follow... What's so hard to understand about the value of my IRA, brokerage account, whatever on 12/31/2023? This is the baseline for how much I can subsequently remit to Thailand as non assessable income. What happens to these accounts post 2023 -- co-mingled funds, or whatever -- is of no consequence -- the 12/31/2023 baseline number remains intact. What am I missing?

-

2

-

-

2 hours ago, chiang mai said:

POR 162 only relates to funds that are in cash and in a personal bank account.

Says who?

-

2

-

-

2 hours ago, chiang mai said:

I think that Answer 5 in misleading.

It states the money is not taxable because the person is not resident in the year it is earned, but it doesn't mention the year the money is remitted

But it asks, "is it taxed when it is brought into Thailand." Certainly sounds like "when remitted" to me.

But, Sherrings is even more clearer when it says: "no tax is owed, because accumulated money is savings from earnings in years you were not a resident of Thailand."

Certainly sounds like a case for the argument that prior year's income becomes "savings" after a certain time element, or more specifically, after being subjected to home country taxation.

So, based on Sherrings, don't worry about prior year's foreign income, when remitted to Thailand in a subsequent year, being considered income at all, but savings. Ergo, not an assessable income moment.

-

1

-

-

1 hour ago, digital said:

Answer to Q14 is perhaps clearer:

No tax is payable when you bring accumulated money from working or operating a business abroad into Thailand, because accumulated money is savings from earnings in years you were not a resident of Thailand

Yeah. I'm getting my threads mixed up, but I recently posted something akin to the above, namely, income after a certain amount of time on the vine, and after being subject to home country taxation, is no longer considered income, but savings. As such, it should no longer be considered as income for Thai taxation purposes. TRD, I guess, could disagree. However, I think with Sherring's input, you should be comfortable not declaring as assessable income monies from past years, now comfortably labelled as savings. And could make a logical argument, in the 1% case you're called in to TRD for an audit.

-

1

-

-

2 hours ago, Sheist said:

Can you elaborate on the "recent info" that says we can use FIFO? (not about IRA, but cash)

Well, maybe not recent. But the latest accounting advice I could find that allowed FIFO for non specific (fungible) assets.

-

15 hours ago, chiang mai said:

Earned whilst not Thai tax resident but remitted when you are....Thai assessable.

When does income no longer remain income? Joe Blow fully retires in 2025; moves to Thailand; is there for over 180 days, thus a Thai tax resident. All the money he subsequently remits is from income he earned in 2024. And which has already been subject to home income taxes. Wouldn't such income now be considered savings, which to me perfectly describes income after being subjected to home country taxes? And what if Joe Blow didn't become a Thai tax resident until 2030 -- would those 2024 monies still be considered income when remitted? Hmmmm. Maybe not, based on what we've heard supposedly coming from the TRD, namely: "Income taxed in your home country is exempt from Thai taxes." Sounds like an appreciation that after tax income -- or at least income that had been subjected to taxation -- is now savings.

Anyway, without any further guidance coming from the TRD, I know what advice I'd give to Joe Blow.

-

1

-

-

4 hours ago, chiang mai said:

Isn't this a valuation issue? I agree the income was earned prior to 31/12/23 hence Por162 applies. But without knowing the value on that date it's not possible to separate assessable and non-assessable funds.

Not sure I follow.... I certainly know the value of my IRA on Dec 31 2024. Yes, I converted the income I had contributed to the IRA into mutual funds, but it's their value on 12/31/2024 that becomes my baseline figure for what I can remit to Thailand non assessable per Por 162. Already in 2024 I had to sell some of the mutual funds in my IRA to meet the required minimum distribution. And this sale, now cash, has been remitted already to Thailand -- and per Por 162, it certainly would not show up on a Thai tax return.

-

What country are you from? Many DTAs, following the OECD Model tax treaty example, have your home country -- where your rental property is located -- as the primary taxation authority. BUT -- the treaties also give your country of residence secondary taxation authority. In this situation, you file with your residence country (Thailand, in this discussion) -- but they have to absorb a tax credit for those taxes you pay to your home country. Two examples of this DTA language is with the UK and US DTAs with Thailand.

So, if the above applies, you'll be off the hook for double taxation. But, if Thailand's taxation on this rental income is higher than your home country's -- being an expat in Thailand means a bigger overall tax bill on your rental income.

-

1

-

-

50 minutes ago, Etaoin Shrdlu said:

An officer from the RD stated that IRAs and 401ks are considered by the RD to be self-directed pensions and that withdrawals would be considered assessable income subject to the rules relating to timing and remittance.

Yes. And per the DTA, Thailand has primary taxation authority to tax these remittances. UNLESS this new TRD rule is used as an exception:

QuoteThe Revenue Department issued another instruction on 21 November 2023 to clarify that their new interpretation of the law will not apply to foreign income earned before 1 Jan 2024

So, what's in your IRA? Pre 2024 income; thus not assessable by TRD decree. Yes, tax deferred, in the case of Traditionl IRAs -- or after tax income, in the case of a Roth (or tx exempt, for subsequent earnings). But, in both cases, the assets in your IRA began as pre 2024 income -- what they look like on 12/31/2023 is irrelevant, i.e., cash, stocks, whatever. So, it looks clear -- at least to me -- that the TRD decree means your IRA distributions, albeit labelled self directed pensions, are not taxable -- except for income accumulated post 2023 -- and recent info says you can use FIFO, thus these earnings would represent the last element of any monies remitted.

Without that Nov 2023 decree, the whole remittance scenario would be different. The Traditional IRA would be taxable by Thailand. As for Roth IRAs -- look at the US-UK DTA for the protocol that dictates a tax exempt Roth by the US must be tax exempt by the UK. If we ever get to this point with Thailand, with worldwide taxation, then probably such a protocol would be needed for the US-Thai DTA to exempt Roth IRAs. But, a story for another day.

-

23 hours ago, Jingthing said:

Also good to know that anything you have abroad as of December 31, 2023 in bank accounts (as opposed to investments, etc.) can be sent to Thailand at any time in future as not accessible income for Thai tax.

Actually, the value of your investments on 12/31/2023, when converted to cash and remitted to Thailand, would not be assessable. So, too, IRA required minimum distributions -- plus anything additional -- would not be assessable income -- up to the IRA's value on 12/31/2023.

-

On 6/3/2024 at 10:50 PM, Galong said:

Social Security Username

This applies if you created an account with Social Security prior to September 18, 2021, and sign in with a username versus your email address. Starting September 2024, these accounts will be retired, so we encourage you to consider setting up an account with Login.gov or ID.me.

Well, it's long past September -- and today (12/17/2024) I could still log into my SSA account with the old system (no Login.gov or ID.me required). I wonder how much longer this will exist, 'cause setting up the new options is a PITA?)

-

1

-

-

6 minutes ago, chiang mai said:

Plus also, the TEDA are different this year to last so that needs to be confirmed in the instructions or on the form..

Ok, good point. My interest is, why would -- or could -- they even address DTA items, or other non assessable incomes -- since there is no "one DTA fits all." But, yeah, sure there will be some changes -- "happy" will be changed to "glad." I just can't imagine any really substantive changes being made. But, we'll see.

-

2

2

-

-

2 minutes ago, chiang mai said:

Whatever we get, and there has to be something, otherwise nobody can file,

Why? What's wrong with the old/current tax forms? What new info is imperative, otherwise "nobody can file?"

-

14 minutes ago, chiang mai said:

is completely reliant on and waiting for the TRD to release the new tax forms and fill in some knowledge gaps in everyone's understanding?

In your opinion, just what changes could we expect? Current tax forms only have income line items for assessable income. Would the new forms have line items for remitted non assessable income (per DTA, or per being pre 2024 income items) -- so that TRD could see what's not being taxed? I guess this could be some interesting information for the green eye shade folks -- but to me, it seems it would be an unnecessary clutter.

What else? A new edict accompanying the forms, saying: If bottom line says, "No taxes owed," no need to file? Highly doubtful, I guess -- but I can only hold out hope that TRD has some element of sanity.

Anyway, just curious on what changes, if any, you expect. For me, the current forms are fairly straightforward, and capture all that is needed for a relatively stress-free tax filing adventure. And, of course, if after you figure out on the back of an envelope, that you owe no taxes -- then just don't file. (NO, NO -- let's not go there again. The readers on this forum have more than enough input to decide their individual action.)

-

1

-

-

2 hours ago, Presnock said:

From what I have read about pensions and taxes, bottom line is a "civil" pension is usually exempt but unless taxes are taken out by the paying government, I think the DTA's allow the Tax resident country to tax according to their tax charges.

Yes, for most OECD countries, civil/military pensions are taxable EXCLUSIVELY by the paying country. This includes Ireland, per their DTA with Thailand. This means, if your home (paying) country decides not to tax your civil/military pension -- you're home free from any taxes, as the EXCLUSIVE clause prevents Thailand from taxing this income, if remitted. This falls under the "exemption" phase of double tax prevention.

Other categories of income, found in DTAs, however, do allow both countries to tax same income, with one being designated primary taxation authority, while the other one is the secondary taxation authority -- but has to absorb a tax credit for the taxes paid to the primary country. Rental income is a good example in many OECD treaties. Here, the situs country of the rental income has primary taxation authority; but your country of residence has secondary taxation authority. Here, if your home (situs) country decides not to tax your rental income, then your country of residence can tax all of it, without having to absorb any tax credits (since there aren't any such credits from the primary country). Thus, in this example, you ain't home free 'from any taxes', because this is avoidance of double taxation by tax credit -- not by exemption. So, without exemption, you end up paying someone. No freebies here.

Thai gov. to tax (remitted) income from abroad for tax residents starting 2024 - Part II

in Jobs, Economy, Banking, Business, Investments

Posted

Wait a minute... We keep hearing that the minimum threshold for the requirement to file a tax return is 120k single -- 220k married. Now the BP is reporting the threshold is 300k baht per year. Which is it?

Ah, so the 25k/mo -- 300k/year -- is, on average, the threshold after which taxes are due. Which just happens to be the threshold whereby a tax return is required to be filed. Could it be that -- the threshold to file a tax return just happens to equate to the threshold after which taxes are due? Naaa. That makes too much sense.

But what about those 6.25 million folks who filed tax returns, but didn't owe taxes? Were they, of sound mind and pure soul, merely adhering to the requirement to file, if one exceeded 120k/220k? Or had their employers withheld taxes, as required -- and they were just filing to have these withholdings refunded? (And, as a BP article recently reported, there were many fraudulent tax filings for the return of phantom wiithholdings.) Hmmmm.