bradiston

-

Posts

5,518 -

Joined

-

Last visited

-

Days Won

1

Content Type

Events

Forums

Downloads

Quizzes

Gallery

Blogs

Everything posted by bradiston

-

Ok, first the good news. WRLife has appiinted AA world as their agents. They have a well attended phone number and people who can respond to questions like "Can I lower my cover/increase my deductible" efficiently and quickly. Their number is +66 2 821 6776. They have a website which is still being built at aa-world.com. So they sent me figures for various deductible amounts and also a sample of lowering my cover, from $400k to $200k. The latter makes remarkably little difference in terms of premiums. I would save in the region of $170 pa. Peanuts. So it doesn't look worth doing.

-

Good comment. I hadn't thought of lowering my level of cover. I'll look into it.

-

As it happens, I can too. But I'm paying for "cover" which only extends to IP critical injury/disease, and where I end up paying for every OP (surgical or otherwise) procedure which can be critical in its own way but is automatically excluded. Ok, I only save 40k THB pa in premiums with the maximum deductible, but that almost pays for a single cataract operation (cheapest I've found is 45k THB) which WRLife don't cover in their main package. Even with their extra packages (dental/optical) you only get $1000 worth of optical treatment, 33k THB, plus the added expense of the additional cover. It doesn't even cover one operation, and they could argue it's OP, so no cover at all. I'll probably opt for the maximum deductible, and if the worst does come about, pay whatever I have to, up to $5k. I've looked at one other insurer, and have yet to decide whether to jump ship from WRLife.

-

Did you mean how the premium decreases for each deductible increase? That's easy enough as WRLife provide a table of example figures. My conclusion is, electing to pay a deductible only makes sense if you feel you are not at risk of incurring overwhelmingly hefty hospital fees any time in the near future. It simply lowers the premium, but incurs the risk of having to shell out up to $5000 each time you end up hospitalised.

-

Maybe a subject for a separate thread. I signed up with WRLife August last year. They put a 6 month moratorium on my existing Afib, which is now well over. I got badly caught out, or you might say, careless, when the BKK Pattaya hospital reported back they wouldn't cover the costs of cataract surgery. It's in an add on package, and it's OP in any case. But my question here isn't really related to the ins and outs of that. It's more to ask your opinion on paying a deductible. I can pay up to $5000 of any in patient treatment they approve. It lowers my premium from 10400 THB pm to 6643 THB pm. Now, I'm assuming as the actuaries and underwriters have access to vast terrabytes of data that allow them to put these numbers together, which I don't have, how can I workout if it's worth signing up for the $5000 package? It seems very tempting. Anyone in the industry have away of calculating these things? Like a table of the most optimised packages? I'll probably go for the $5000 deductible, and just "be good, failing which, be careful". My very primitive methodology for assessing the benefits have to make massive assumptions about the coming state of my health. Maybe one big payout in 5 years.

-

Talks in forming coalition have yet to start – Pheu Thai leader

bradiston replied to webfact's topic in Thailand News

Cue the PT ratting out on all their previous utterances, given to garner support for themselves. Never liked or trusted PT. They must be several members short of a parliamentary majority to offer a 10k THB bribe, and expect it to pass without comment. They deeply resent playing second fiddle(rs) to MFP. Now watch the whole thing unravel. -

Selling a house

bradiston replied to bradiston's topic in Real Estate, Housing, House and Land Ownership

I've had 4 made up. Cheers! -

Selling a house

bradiston replied to bradiston's topic in Real Estate, Housing, House and Land Ownership

Thanks for all the replies. I've managed to list on a few sites, and FB. Location is key. Where my house is might be considered a backwater, off the beaten track, so very few agents will handle it, even though it's what might appeal. Most sales there are done by word of mouth, or visitors who know what they're looking for, so I'll have to content myself with that. -

Why is this being posted here?

-

Thailand’s experiment with weed goes up in smoke

bradiston replied to snoop1130's topic in Thailand News

"After four years of support from the ruling coalition government, Thailand is expected to vote against the decriminalisation of marijuana in Sunday’s general election." What the heck does this sentence mean? For or against, it's not what Thailand is voting for. It's a general election, not a vote on weed control. Media spin, par excellence. As throughout the whole decriminalisation process. -

DWP paid into my Wise account today.

-

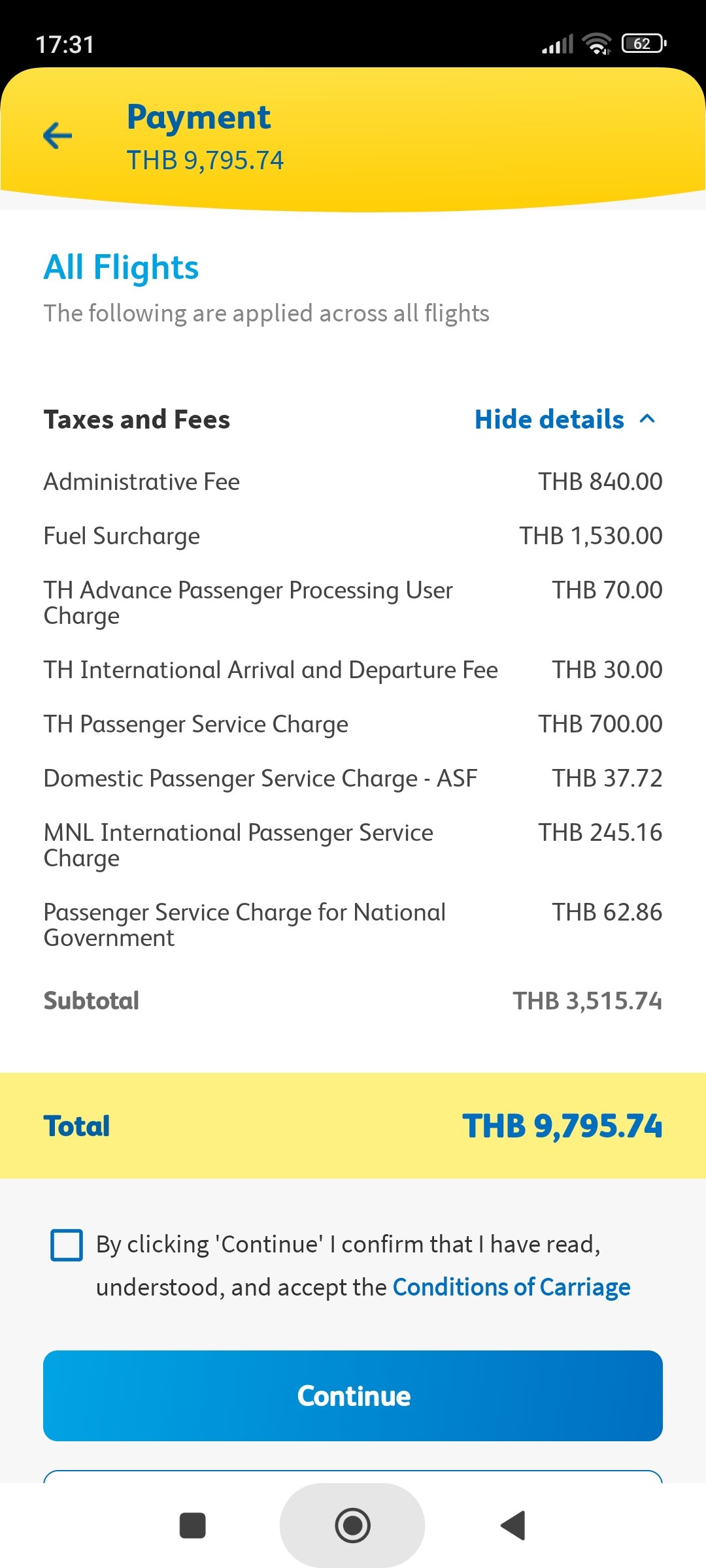

The 700 THB amount is listed as "Passenger Service Charge". Where do you see a departure tax?

-

There is no new tax. It's all fake news.

-

No. Rubbish reporting does.

-

Where's the 800 THB departure tax?

-

Below where?

-

The Thai international arrival and departure fee is currently listed as 30 THB. But there are numerous other charges. See my screenshot above.

-

Here's a screenshot of the add ons for a return flight to Manila from BKK recently. More than 30% of the fare.

-

Crafty Thai woman allegedly steals British tourist’s Rolex in Pattaya

bradiston replied to webfact's topic in Pattaya News

Variation no 3 on gold necklace/lady boy/Beach Rd story. There must be a book of these somewhere. -

It wasn't BP. It was PN and AN.

-

Search BP under "departure tax".

-

Exactly. It's been picked up by AN and PN as a done deal. Nothing of the sort. They should publish a retraction.

-

Search the BP under "departure tax". You'll see it was all a non starter. You're wasting your time even commenting on it, and the OP should never have posted it. Such poor journalism.

-

This is an opinion poll. Totally fake and out of date news.

-

"Dear Valued Client, Please be advise as per check we regret to inform you we cannot cover the Cataract surgery, Because you do not have Optical benefits under your Policy. Serenity Plan: Module 3 Dental / Optical – NO Thank you for your understanding. Regards, Lally"