Pib

Advanced Member

-

Joined

-

Last visited

-

Just to get a feel how well (or bad) the Atto 2 may sell in Thailand below is EV registrations for "Feb 2026 in Malaysia." Only 20 Atto 2's were sold....maybe Atto 2 sales are fizzling-out after its launch 7 months earlier in late Jul 2025. But February is probably a slow sales month each year like how it's slow in China, Thailand, etc., around the Chinese New Year....just a slow selling period based on recent years. Additionally, only one month of stats is just a brief snapshot in time. Top 30 EV models in Malaysia for February 2026https://soyacincau.com/wp-content/uploads/2026/03/260310-malaysia-ev-registration-feb-2026-top-30-ev-models-1-578x1024.jpg

-

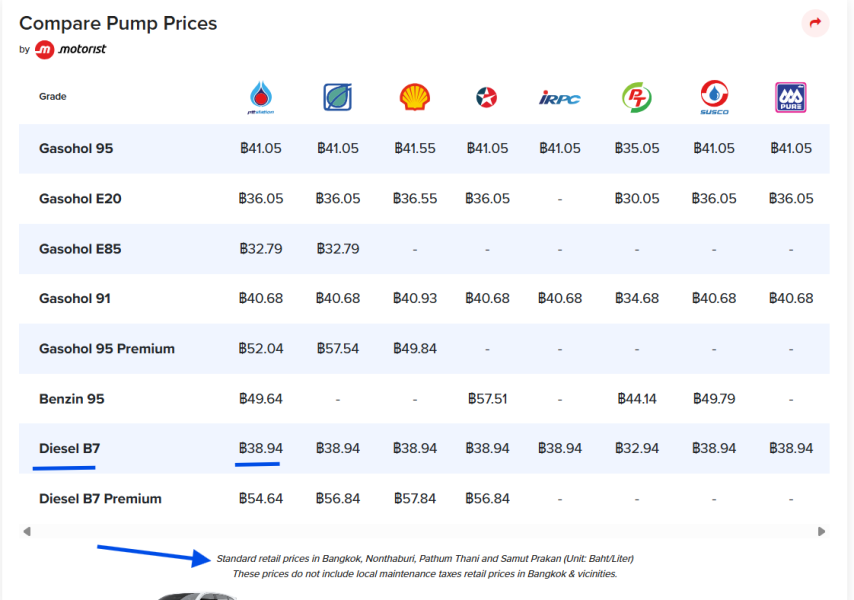

Ouch!!!!....this will probably help "EV" sales. But it will probably hurt "overall sales (ICE/Hybrid/EV combined)" as it will make many people feel uneasy about the economy, their job, buying a big ticket item like a vehicle. Fuel prices in Bangkok area as of 26 March 2026.

-

Just to get a feel of how well (or bad) the Atto 2 may sell in Thailand below is how well it sold in Malaysia in 2025.....it was the 6th best selling EV. https://automacha.com/here-are-the-30-best-selling-evs-in-malaysia-in-2025/ Top 30 Most Registered EV Models In Malaysia (2025) Ranking Model Total Registrations (Jan – Dec 2025) 1 Proton e.MAS 7 8,677 2 BYD Sealion 7 4,454 3 Tesla Model Y 4,401 4 BYD Atto 3 4,069 5 Tesla Model 3 2,880 6 BYD Atto 2 1,779 7 BYD M6 1,683 8 Zeekr 7X 1,510 9 BYD Seal 6 1,279 10 Denza D9 1,200 11 BYD Seal 1,056 12 Zeekr 009 914 13 XPeng G6 892 14 Chery iCaur 03 836 15 Chery Omoda E5 647 16 XPeng X9 644 17 Leapmotor C10 500 18 GWM Ora Good Cat / 07 446 19 Porsche Taycan 421 20 Smart #1 / #3 / #5 414 21 BMW iX2 405 22 Mercedes-Benz EQE 326 23 Porsche Macan EV 318 24 BMW i5 316 25 MG4 294 26 MINI Aceman 286 27 BMW iX1 279 28 Volvo EX30 275 29 BMW i4 239 30 Proton e.MAS 5 213

-

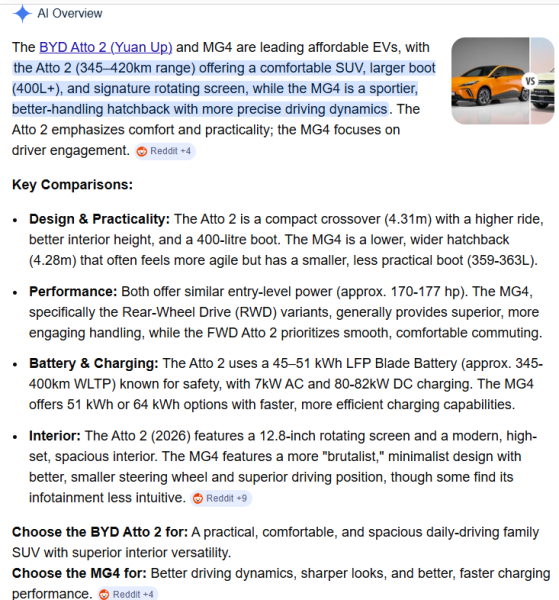

No doubt some of the MG4 hatchback technical specs are better, but the Atto 2 SUV interior and exterior appearance will surely win many people over as a vehicle's "first impression" interior and exterior-wise are the biggest factors in whether a person ends up liking a vehicle or not. I liked the Atto 2 interior and exterior when I gave it a few minutes look-over today at a BYD dealership....the interior size really surprised me and very nice seats. Below is how AI feels about an Atto 2 and MG4 comparison.

-

While waiting on the wife to turn her grey hair into black hair at a beauty shop I went to a nearby BYD dealership to kill time and take a brief look at the BYD Atto 1 and 2. Based on just a few minutes of looking at and setting in each model I was impressed with the Atto 2. It looks good inside and out. And feels pretty roomy. Now the Atto 1 was too small for my liking.

-

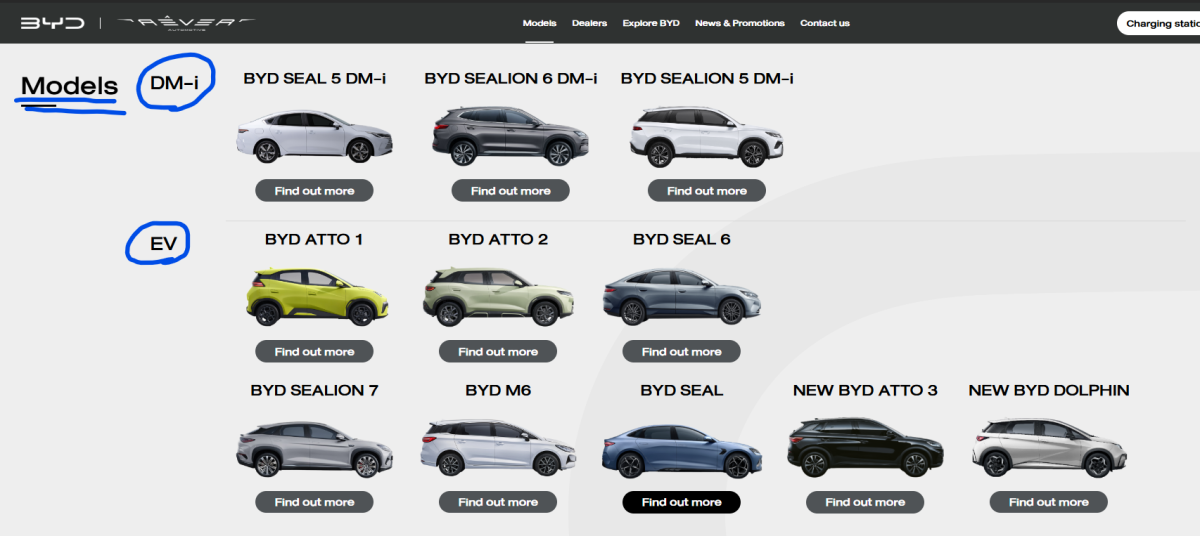

BYD started selling EVs in Thailand in 2022...the Atto 3 model. Now in early 2026 they are selling the 11 models shown below in Thailand...3 hybrid models (the DM-i models) and 8 BEV (100% electric) models. Oh, how times have changed. https://www.reverautomotive.com/en

-

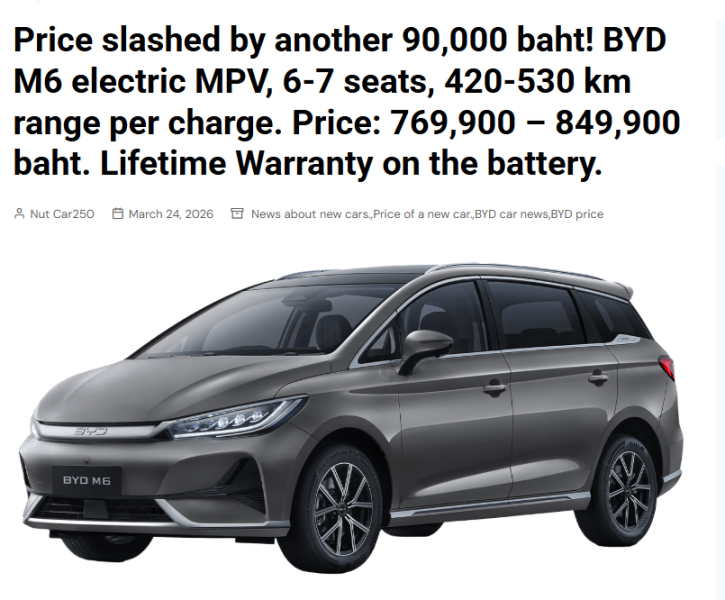

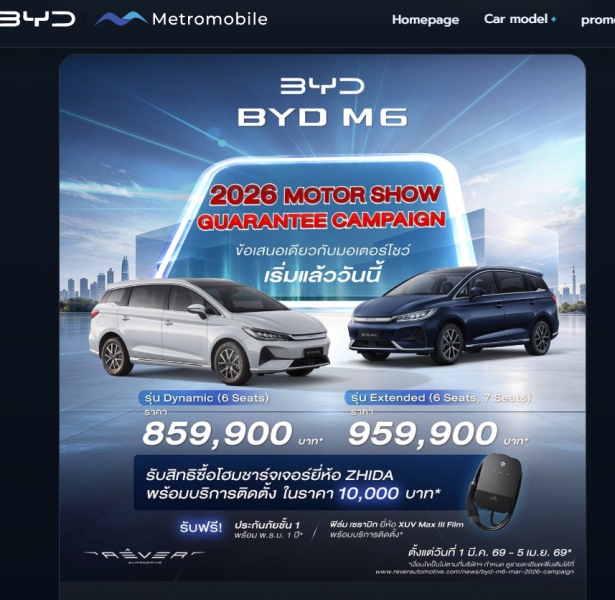

BYD in price cutting mood. https://www.car250.com/ And below is the BYD Motor Show promotion "just before above the price cut." Below snapshot is from a local BYD dealership website which hasn't updated to the latest promotion yet. Once again, I expect folks who bought the M6 over the last 6 weeks or so are now PO'ed.

-

The motor show promotions are almost always nation-wide at any dealership. You do not need to attend the show in Bangkok to get the same pricing/deal. Typically to reserve/buy a vehicle at the motor show you fill out the same paperwork and place a deposit of Bt3K to Bt10K "just like you would at your local dealership." Backing out of the reservation can result in loss of the deposit...the deposit paperwork you sign will state the rules that can result in forfeiture of the deposit. Just because you make a reservation deposit does not lock you into completing the buy.

-

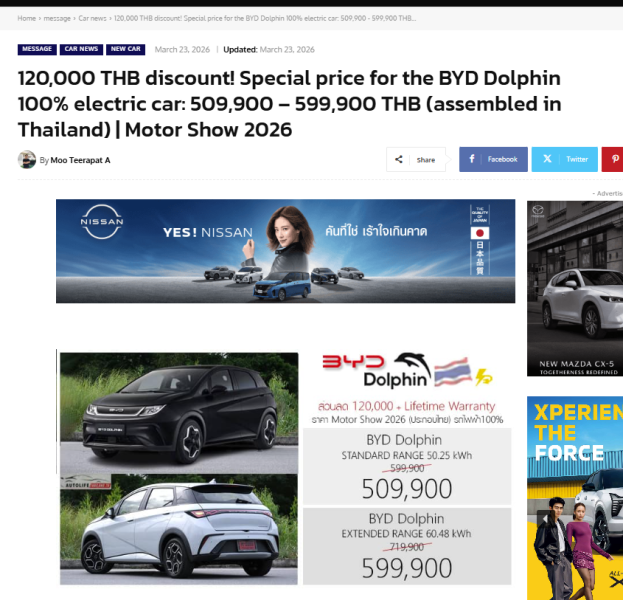

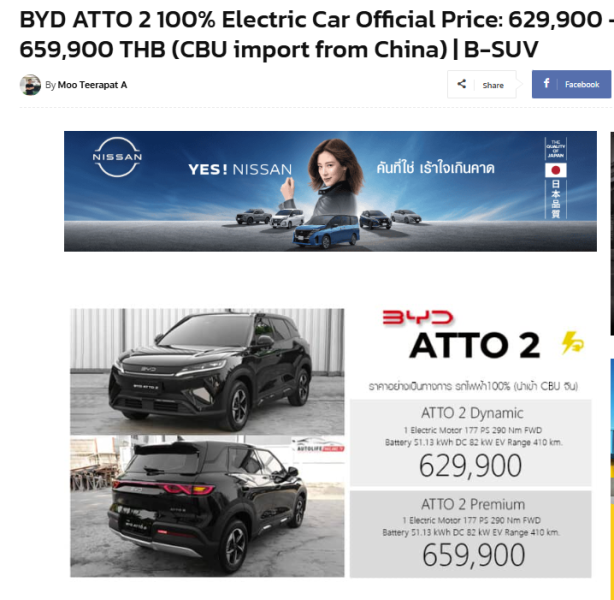

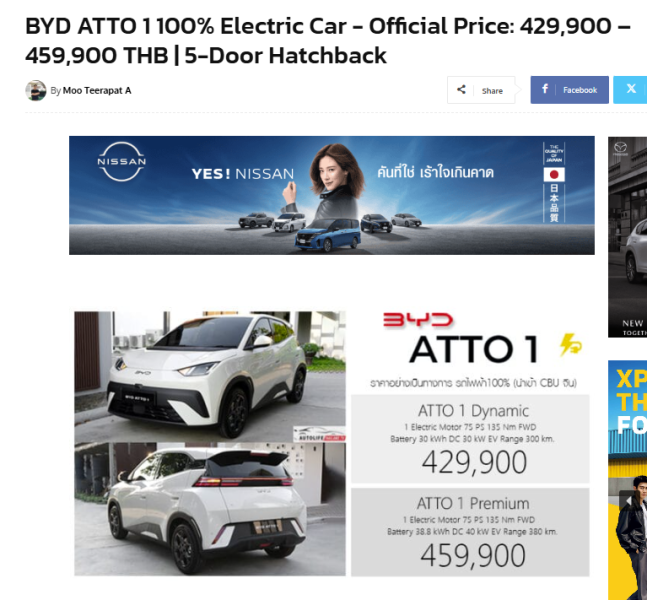

BYD getting into the price cutting again....and definitely offering plenty of choices in the small SUV arena. BYD Dolphin pricing....a BIG up to Bt120K price cut. BYD Atto "1" pricing BYD Atto "2" pricing

-

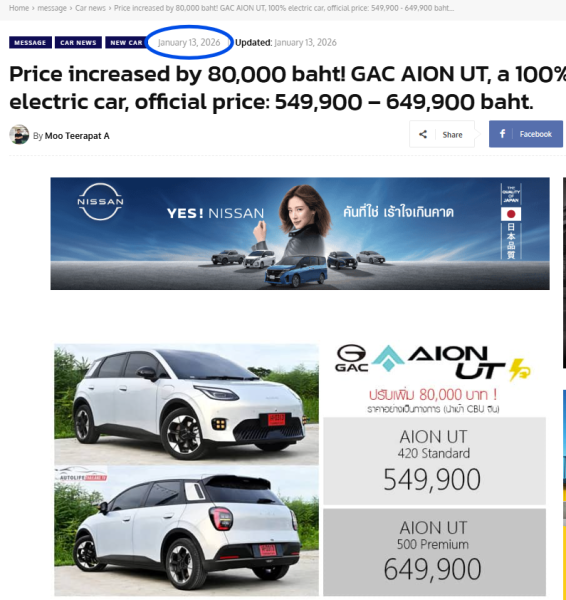

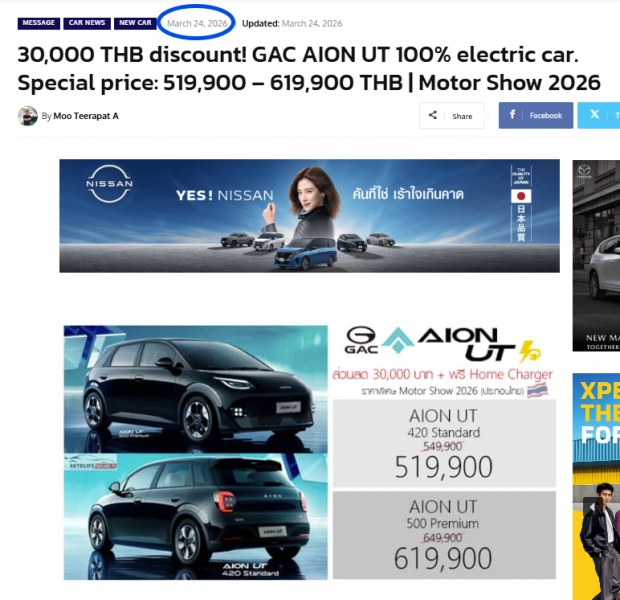

AION UT pricing increased Bt80K in mid January (1st image below)....but now in late March reduced Bt30K (2nd image below). That should PO those who bought since the mid Jan increase. Up Bt80K in January Down Bt30K in March.

-

For those interested in getting a PHEV you might want to read below article/report...and also take a look at below Youtube video which talks about the report. With a PHEV you are probably not getting anything close to fuel savings advertised and that you hoped for when buying the PHEV because the petrol-powered engine actually runs more often than you are aware of....sometimes running in EV Mode only. Before I thought that when a PHEV is in the "EV Only" mode and assuming it had battery charge remaining that it would indeed run off the battery only, but that's not how it works unless maybe you are driving conservatively on a flat road with no stopping. https://electriccarsreport.com/2026/02/phevs-use-more-fuel-than-advertised-major-study-finds/#:~:text=The%20Study:%20Real%2DWorld%20Data,What%20is%20this? PHEVs Use More Fuel Than Advertised, Major Study Finds The promise of the Plug-in Hybrid Electric Vehicle (PHEV) has always been a seductive one: the “best of both worlds.” You get enough all-electric range for the daily commute and a combustion engine to kill range anxiety for weekend road trips. On paper, it’s the perfect bridge to a fully electric future. But new real-world data suggests that promise doesn’t always hold up. A comprehensive study by Germany’s Fraunhofer Institute found that many PHEVs consume significantly more fuel in everyday driving than their official lab ratings suggest — in some cases, up to three times more. The Study: Real-World Data From 1 Million PHEVs...... (go to above weblink for full article). A Youtube video talking above PHEV study. AI query result Recent studies analyzing data from approximately 1 million plug-in hybrid electric vehicles (PHEVs) in Europe have revealed significant discrepancies between official fuel efficiency ratings and real-world usage . While manufacturers often claim extremely low fuel consumption, the study shows that in practice, these vehicles consume significantly more fuel than advertised, particularly when they are not regularly recharged by their owners. Key Findings from the 1 Million Vehicle Study: Fuel Consumption: Real-world fuel consumption for PHEVs is often three times higher than the official laboratory-tested figures. Performance: Instead of the 1–2 liters per 100 km promised, actual usage is closer to 6 liters per 100 km, similar to conventional cars, according to a report from the Fraunhofer Institute. Charging Habits: The research suggests that many drivers, particularly those with company cars, do not charge their vehicles frequently, leading to higher fuel consumption. Inefficiency in Practice: The study indicated that some luxury brands, such as Porsche, showed particularly high fuel usage, with some vehicles operating on electric power for only a tiny fraction of their total mileage.

-

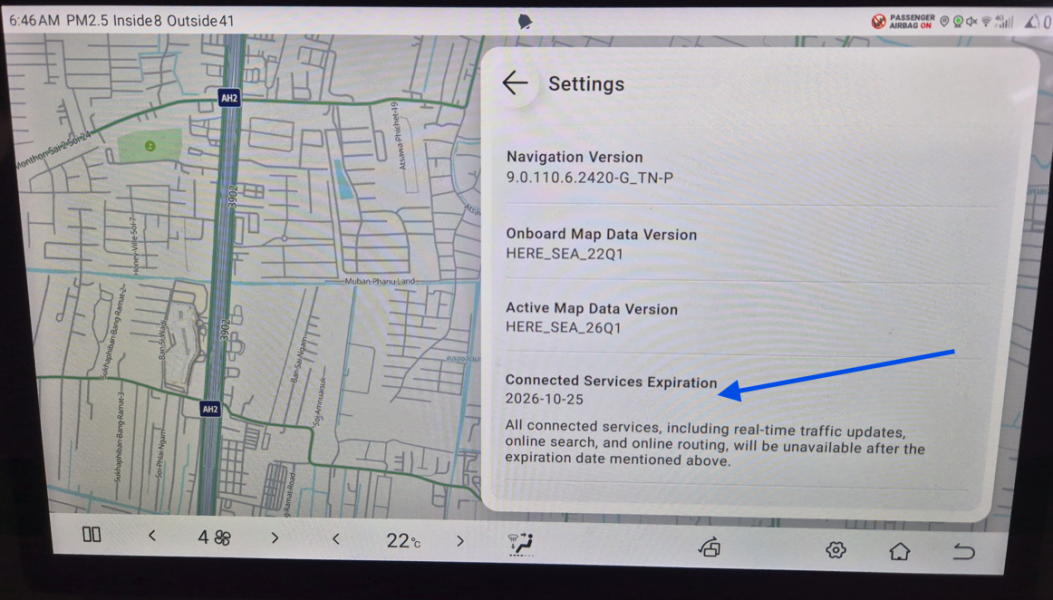

No, the end date of your monthly data allotment of 2GB which is 2 years (or 2 years 3 months if you got the updated SIM) after receiving your BYD and the end date of the BYD map software which is 3 years after receiving your BYD vehicle are two different animals....two different dates. My monthly data allotment of 2GB expired several months and I've been using my phone hotspot function ever since for a vehicle data connection while driving. Actually I was suppose to get 2 years 3 months since I got the SIM update but the data allotment died after around 2 years or maybe 2 years 1 month. Without a data connection certain functions on Google Maps or BYD maps will not work like current traffic conditions, recommended routing, etc. But with the BYD map there is another date to be concerned about....their "Connected Services Expiration" date which you can see by going into the "About" selection in the BYD map settings. After this expiration date "All connected services, including real-time traffic updates, online search, and online routing, will be unavailable....." See below snapshot I took this morning. In my case the BYD map Connected Services Expiration date is 25 Oct 2026 which just happens to be exactly three years from the date I picked up my Atto in 25 Oct 2023. Now that exactly 3 years date could just be a coincidence but my bet it isn't....my bet is tried to the date you drove your new BYD vehicle home from the dealership. And I also remember about a year ago when the BYD map software (by TeleNav Software) did a major update where its menus appearance/setting change significantly (t was an OTA update at home and "not" part of a vehicle OTA update....it was just an update of the BYD map software only) that the software provided a summary/comments at the end of the update that after the expiration date that a person would need to subscribe directly with TeleNav Software to retain full functionality like online real time updates, routing, etc. Now I do not know if that "Connected Services Expiration" date might be extended when BYD does an OTA update to update "all" the software on the vehicle (no just a standalone map update)....or, if that BYD map Connected Services Expiration date is tied to the date you picked up your new BYD vehicle with a 3 year period for full BYD map services....kinda, like their Data Allotment period of 2 years worth of data...after that you have to use hotspot functionality.

-

Yea, the SL7 onboard charger is a 11KW charger when using 3 phase (16A max per phase) or 7KW when using single phase (32A max). Regarding the BYD maps, yea, it could be better. Unless something has changed you can only save a max of 20 Favorite locations, the zoom in and out returns to the default zoom level after about 30 seconds (this really bugs me as I like to select my zoom level), and just a variety of other things I don't like when compared to Google Maps. I use Google Maps running under GPack on my Atto. Running Google Maps under Gpack (installed by BYD dealership) is better than running it under Android Auto/Apple CarPlay which seems to act like a handicapped Google Maps. Under Gpack Google Maps is just like running it on your smartphone....no limitations like when running under Android Auto/Apple Carplay. I prefer Google Maps to other map programs as I'm use to Google Maps, I have Google Maps on my smartphones, and when you switch vehicles as long as the vehicle has Google Maps once you log into your Google acct you now have your personalized Favorite map locations again. Plus, after X-amount of years the BYD map program will stop updating/will not show certain things like traffic jams/road conditions ahead of you unless you subscribe directly with the BYD map company. Yeap, Google Maps is the way to go.

-

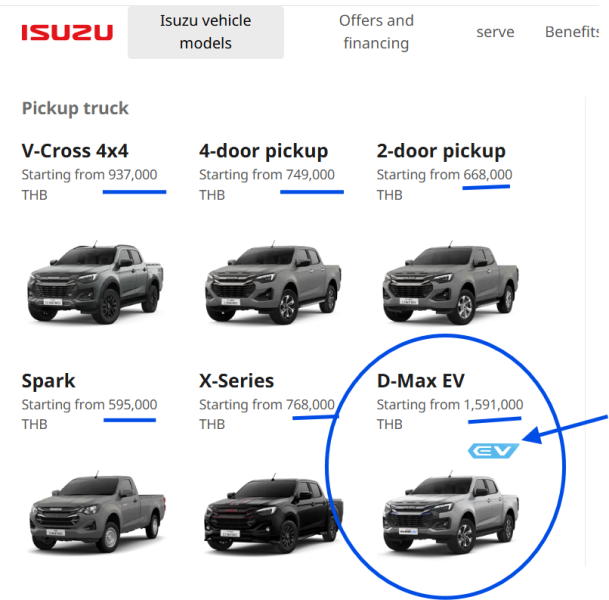

The D-Max EV costs a "lot" more than Isuzu ICE trucks.....like twice as much as a Isuzu ICE 4 door pickup at Bt749K. Expect only a few "gentleman" farmers and some cities folks will buy the D-Max EV since it costs so much more than an Isuzu ICE truck. https://www.isuzu-tis.com/isuzu-x-series

-

The 7X Standard and Long Range models have different seats from the AWD. The Standard/LR have "Soft PU" seats while the AWD has "NAPPA" seats (real leather). Additionally, the Standard model front seats do not have the "ventilation and massage" functions but the LR and AWD front seats do have ventilation and massage along with some additional seat adjustments the Standard model does not have. Knowing exactly which model you were setting in could make a significant difference in how the seats feel. And I expect once the seats get broke-in a little they would feel somewhat different like how a demo model gets set-in a lot.