Nemises

-

Posts

2,757 -

Joined

-

Last visited

Content Type

Events

Forums

Downloads

Quizzes

Gallery

Blogs

Everything posted by Nemises

-

Expats How Do You Deal With The Toxic Air Pollution in Thailand?

Nemises replied to Mitkof Island's topic in General Topics

-

Agree. Sometimes it can be hard accessing the HDMI socket. Lucky my multi-purpose Leatherman has the necessary screwdrivers 😁

-

Already mentioned the app: LiveNet Do you use LiveNet? Does it show advertising videos?

-

Just returned from a holiday staying at a “luxury” hotel. My room had a TX 6 android box. Was trying to watch the Australian Open tennis on the box using LiveNet but it kept switching to advertising videos (always during match critical stages) thus completely ruining the viewing experience. Thank goodness I could stream the tennis on my phone during those ‘ad block outs’. I couldn’t cast my phone because it was not a smart TV. This problem will never happen again as I will be sure to pack my laptop and HDMi cable from now on - regardless of the hotel’s rating. Just wondering if these annoying LENGTHY video advertisements occur on all android boxes? Or just LiveNet?

-

Agree. In fact I prefer to use my modern, powerful laptop (with a wireless mouse) instead of ‘dodgy android boxes’ or a phone. I find an HDMi cable more reliable than casting from a phone especially when travelling - which is often - as not all hotel TVs have casting abilities. Also, some of my home-country channels are geo-blocked on my phone (even when using a VPN) but not on a laptop.

-

I had the “fortune” to date a beautiful Thai lawyer. Lasted until she ordered me to ditch my late model Ford Ranger and replace it with an upmarket European car to match hers. In other words, about 1 week.

-

Dell for me, every time! My minimum specs: 15.6” screen i5 Intel processor 32 Mb RAM 256 GB HD. Comes complete with HDMI & multiple USB ports. If possible buy in home country, claim Sales Tax refund at airport on way back to LoS.

-

Who got bored in Thailand and went back?

Nemises replied to georgegeorgia's topic in ASEAN NOW Community Pub

Still lots of beautiful, peaceful, locations in Thailand without hardy any tourists nor crime. -

No. Open OneDrive, click on the required image/s, click the download button, it’s/ they are all now back on your phone….in less than a few seconds.

-

Today’s Aus news. Pint of beer to rise to $15.00 next month. https://youtu.be/2cTEsKtda_Q?si=BWSyAWNFoeWJzn9M

-

American on Dirt Bike Kills Thai Woman Crossing Road in Chiang Mai

Nemises replied to Georgealbert's topic in Chiang Mai News

Reckless driving causing death Anyone got a link to what sentences have been handed down previously to foreigners found guilty of this? (Link only required please, not predictions). -

The front page news item you’re referring to was exactly 2 years ago this month! No one is saying it’s still a “fuss”.

-

Can only see “Happy Hour” $6 schooners on that link. How much during normal hours?

-

Venture way out to St Mary’s or Rooty Hill for a $6 or $7 schooner? No thanks.

-

Can’t reply as you mentioned the A word and those posts are being removed.

-

You are wrong. Love being here ......and love not having to do 90 day reports at IO's - thank goodness there's an easy solution to the OP's problem.

-

Never truer words spoken.

-

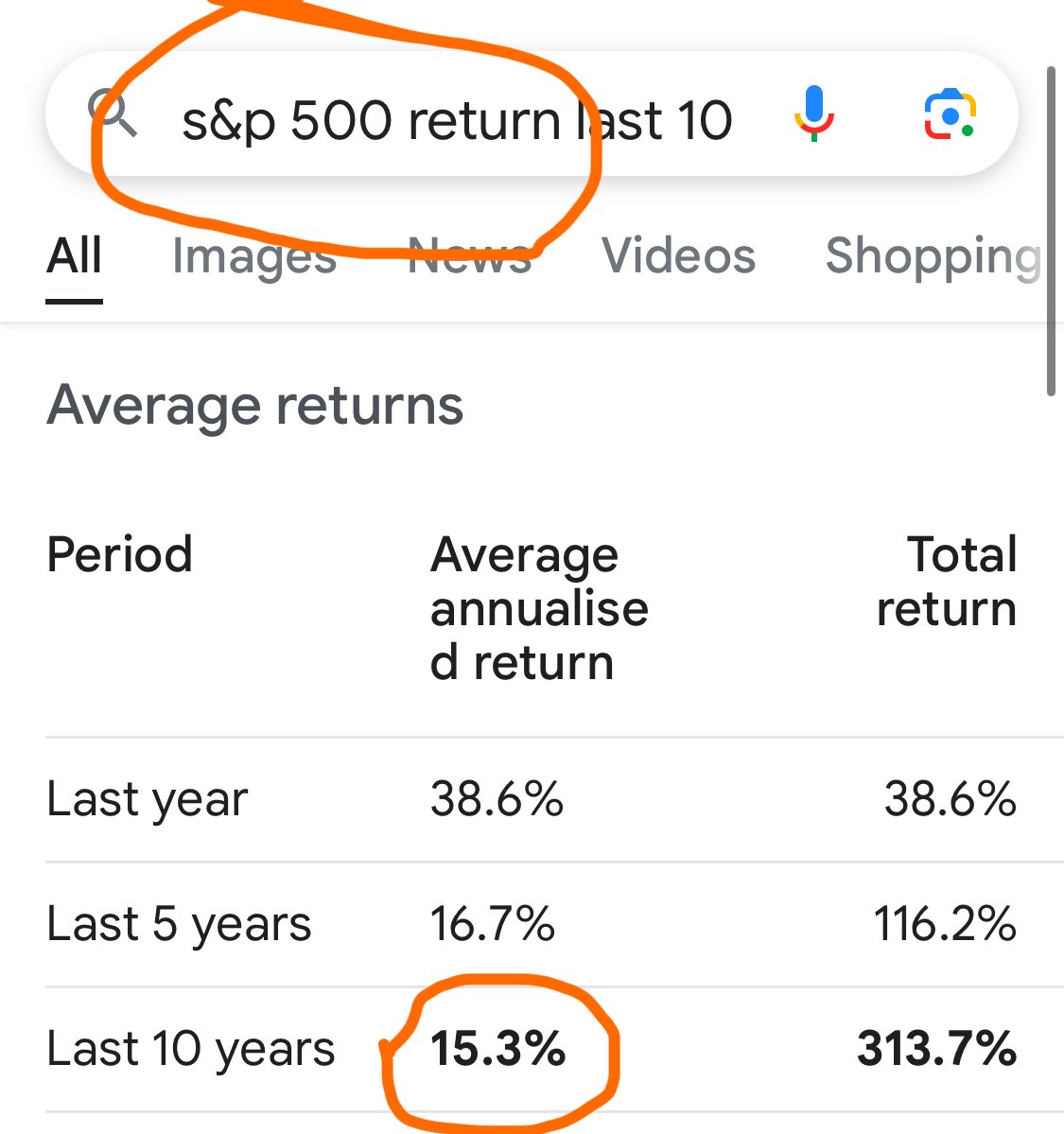

Fantasy? So the 15% average that the S&P 500 has returned over the past 10 years is a “fantasy”. Got it 👍

-

Love being here. Also love looking at the 2 million baht balance that my original 800k investment is now worth after 10 years in the S&P 500 instead of sitting dormant in some Thai bank. Have no idea about immigration rules as I've never been in an IO... and never will.

-

Agents are also for those who have their money invested in their home country and have better things to do then F-ing around with Thai IOs and their reporting BS. Not to mention getting near-zero % return on your 800k sitting uselessly in some Thai bank.

-

Australian Aged Pension

Nemises replied to VOICEOVER's topic in Australia & Oceania Topics and Events

Begs the question: what % of your pension do they take if you are ever needed to pay them back? Anyone know? (Asking for a friend). -

Have an android TV box with a VPN. Just wondering what's the best (most reliable) for UK Premier League/UEFA tournaments please.

-

Thanks ricklev, I did the same (NordVPN) and it's working fine again. Much appreciated.

-

thetvapp.to is no longer :(( Looking for a similar site please. TIA

-

Causes of High Electricity Bills in Thai Apartments

Nemises replied to CharlieH's topic in General Topics

Suggest ask them. See ya.