UKresonant

Advanced Member

-

Joined

-

Last visited

Everything posted by UKresonant

-

Thanks for that info. I guess the English translation of POR 162/2566 lost a bit somewhere. From 2024 on A. Earned / derived whilst Thai Tax resident. B. Assessable in the future if that at "A" is remitted to Thailand. If they think that when you spend one year ever, tax resident, and then they will tax anything that is sent to Thailand for eternity, then yes I will try and circumvent that, or think what that very special year may be. I wonder if they will bring out a 90per 179 day ME Visa? I suppose two single entry 90 day ones would do. Would be interesting if you find where you read /;seen that. Sounds like more mines in the minefield, or it could be easy the ain't really fully unfurled their new colours yet perhaps. Smiley face or Smiley with sharp teeth

-

not quite what you asked for, may be of some use? (consider as a draft)

-

Government could be National or Local authority... https://www.gov.uk/hmrc-internal-manuals/international-manual/intm343040 Part C.1: UK State Pension or Incapacity Benefit... "If there is no ‘other income’ article, you cannot claim exemption under the treaty from UK Income Tax on your State Pension". https://assets.publishing.service.gov.uk/media/637e192f8fa8f56eabf75e5b/Double_Taxation_Treaty_Relief_Form_DT-Individual.pdf Part 😄 Application for relief at source from UK Income Tax (Thailand = No) (Relief at source may be available in cases where HMRC is able to exercise its discretion to issue a notice...????) Where we cannot agree to allow relief at source or cannot arrange it, you can claim repayment of part or all of the UK tax taken off, as appropriate. (Big Maybe, could be double tax for months, until sorted, if possible) P34 note (R/H Column) 4. Treaty does not include an article dealing with DT-Company Non-Government pensions. Also, no relief for State Pension or ‘trivial commutation lump sum’. https://assets.publishing.service.gov.uk/media/5b05425fed915d1317445ed2/DT_Digest_April_2018.pdf

-

That is the choice under consideration, to have the Beer in the UK or Thailand 😋

-

With the assumption of being Thai Tax Resident at both events....

-

Nope.

-

I'm starting to think the Thai RD may think it is odd were asking about tax on pensions. Cashng in your RMF units appear to be exempt from tax https://sherrings.com/rmf-ssf-salary-sacrificing-tax-allowances-thailand.html Normally the Retirement Mutual Fund would be cashed in, and they would tax whatever income is produced from where you place the tax exempt lump sum. Trying to find an example of similar in English for a Thai company pension .scheme. So the.question being "do I need to pay tax on my pension?" Expected logical answer would perhaps be NO in the Thai pension context.(?)

-

OCCUPATIONAL MANDATORY (PROVIDENT FUND) "Tax EEE tax policy is currently adopted in Thailand, i.e. contribution, investment and payout are all tax exempted, although such tax relief is subject to limit of...." from this 2009 publication https://www.ilo.org/wcmsp5/groups/public/---asia/---ro-bangkok/documents/publication/wcms_836733.pdf Trying to find a more recent reference....

-

Could it be treated the same as Thai Pensions, Tax free at point of taking it, but then anything derived from it is taxable? (UK Article 24) would not like to test that though! Maybe since the UK does not offer relief at the UK end (except Thai National & resident on Gov ones), they thought at the time the were always to get Tax credit relief under UK DTA 23 3). So assumed they did not need an article. https://assets.publishing.service.gov.uk/media/637e192f8fa8f56eabf75e5b/Double_Taxation_Treaty_Relief_Form_DT-Individual.pdf https://www.gov.uk/government/publications/thailand-tax-treaties#:~:text=The double taxation convention entered,Corporation Tax and development tax

-

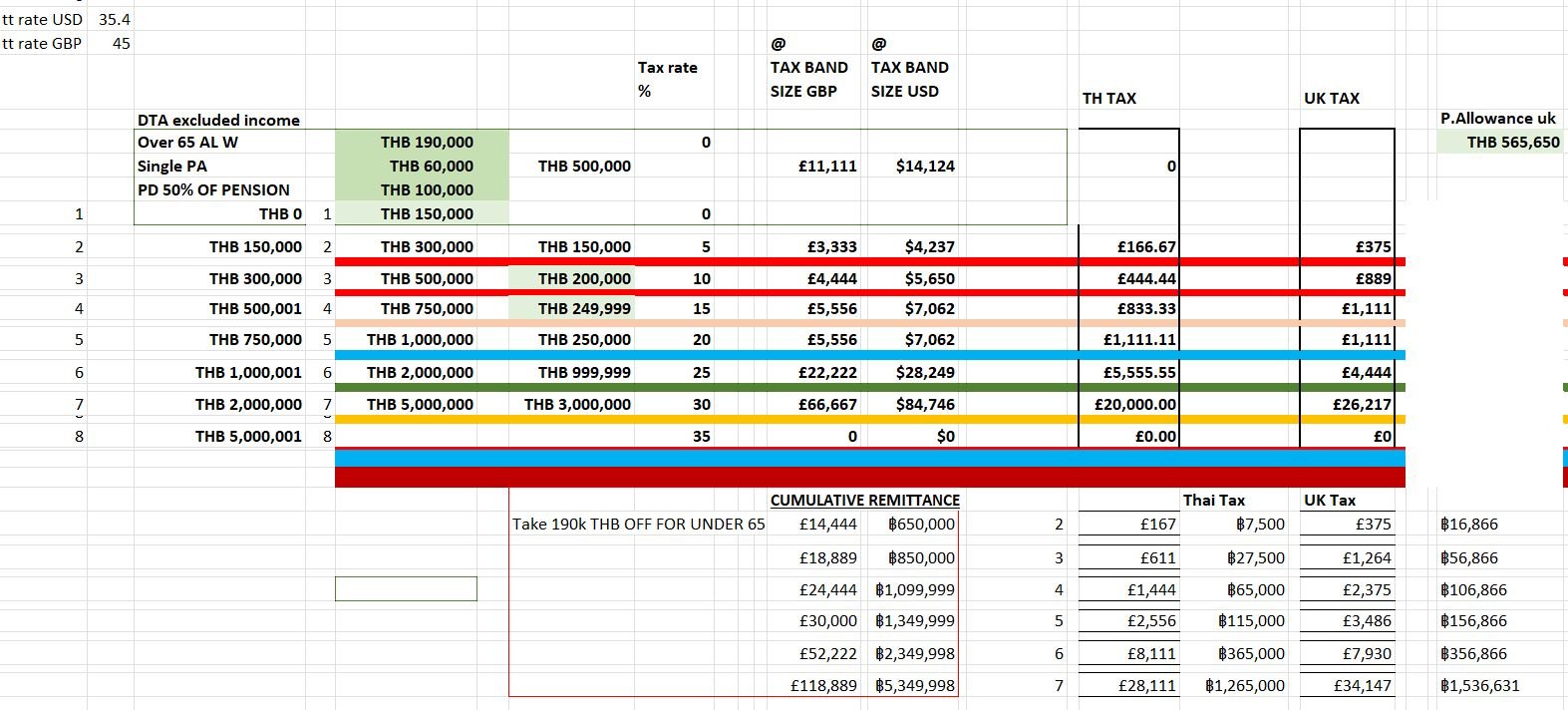

(Por 161/2566) For a resident of Thailand who Derives or Earns , whilst being a Resident of Thailand, foreign source assessable income from 1st Jan 2024 onward it's subject to tax when remitted to Thailand (Whenever). Previously it became taxable when remitted in the preceding Tax Year (to the Tax Filing 1st Jan - 31st March), when derived or earned, whilst being a Resident of Thailand. (Por 162/2566) don't apply 161/2566 for stuff prior to 1st Jan 2024! So if UK Pensions are of no interest to them to be taxed, by those RD offices perhaps are they thinking they were not derived while tax resident? wording of DTA would suggest not. Or s it because UK does not give relief from UK Tax, and the tax yield after credit relief (UK DTA 23) or exemption (UK DTA 19) is hardly going to yield very much. But there seemed to be a lack of interest, in Thai RD taxing pensions, going back many years. Someone way back suggested it was UK DTA 24, in that Similar Thai Pensions are not taxed as when they are not Government pensions, they are the same except it is a 100% tax free lump sum, rather than a 25% Tax free, and an ongoing payment. Equal treatment? Still a bit of a mystery. (No written exemption or firm explanation that I've ever been able to find). Going forward, Dividends, CGT as Personal income tax will, bank interest etc will still surely be. (this post is a bit delayed as I see there about 10 new post before I pushed the button) p.s I think the tax code is very much written from the Thai National, Thai resident, thinking of going overseas, context. Also we perhaps have a pre conceived concept, of the some times over officious application of untidy tax laws they are tasked to enforce.

-

Reading UK HMRC form "DT-individual" in conjunction with the Digest of Double Taxation Treaties (2018). Getting any relief from the UK end seems unlikely perhaps. Government pension - only if Thai national and resident in Thailand (N&R). Other Pensions "No Relief"

-

.......whilst tax resident in Thailand (?) re 162/2566.... (Just in case anyone is out on a 8month contract or back home to re-charge the financial batteries, have spoken to some doing that, on on flights home over the years)

-

I have to agree about the ISA I can see dividends paid out of the tax free ISA wrapper could be taxed as normal dividends, but no idea on calculating capital gains from any disposal out of the ISA if tax resident in Thailand.

-

The Thai Tax system is still usefully allowing remittance basis. So to some extent the amount being taxed, and what you remit can be controlled. The amount Thai tax is a bit variable compared with the UK tax, whether it is more more less, with various factors especially if above or below 65 years of age. It seems always less than the UK Income Tax once over circa 2 million Baht p.a. Looking if it were someone going to the UK , you only get 7 years of remittance basis , then it becomes unworkabley expensive for mortals. The Gov opposition party (due to this years election) are are actually wanting the remittance basis to be cancelled. With no apparent thought on how repulsive and inward looking, that will make the UK appear for companies may wish to go with inward investment, and find essential personel, may not wish to go. This years Thai tax move will have a component of reduced spend and small VAT offset probably, for folk with mostly foreign income. Details and a practicle mechanism yet to be seen of course....

-

Here is an extract from the UK remittance pages, I've not yet found the equivalent Thai RD page, but suspect it may be somewhat similar, in respect to you question..... "...Most remittances to the UK will be under the general rules but there are additional rules under which your foreign income and gains may be remitted to the UK. For example, you gift some of your foreign income or gains or something deriving from them to a person other than a relevant person - a gift recipient. It’s still possible for there to be a remittance of your foreign income or gains if the gift is used in such a way that it benefits a relevant person. Your money or property does not have to be physically imported from overseas for a remittance to occur. For example, it could be money you receive in the UK from another UK resident, in return for money or assets representing your foreign income and gains transferred to them abroad. 1.3 Relevant person A relevant person is: the individual themselves, that’s, the person to whom the foreign income and gains belong the individual’s spouse or civil partner, or people living together as if they’re spouses or civil partners the individual’s children or grandchildren under 18 years of age (this includes children or grandchildren of their spouse or civil partners).....

-

Why, thank you! It is disappointing that people don't pay attention to there home country's attitude to the subject, as Thailand cribbing across some of their tax regime, just highlights how aggressive they are. They could copy more and it would be much worse! Governmental organisations have a high motivation to grab more tax so it may be spent inefficiently (already spent with poor value for money more like). No one has a feeling about the subject, until a mirror suddenly appears.

-

That's the way I always look it as well when I've been there (and I've never done an extension yet ) That's the only Visa options available, other than actual custom and practice.

-

Are there many in those groups that seek a long term continuity of relationship with Thailand , like retired / married groupings, even if they are not in Thailand continuously? If they don't have a long term inclinations in Thailand, you are most probably correct and their posture may also reflect their home country tax and general environment, as for many other nationality groups. However North America and Europe are highly regulated tax environments, which could account for some variance in attitude. There are also non Nationality specific attitudes, not recognising how Thailand has developed and is developing fast in at least some, if not most ministerial jurisdictions. Not looking down and perhaps looking up slightly soon may become appropriate...A common interface struggles with their general subject situation having been defined 45 years in the past, however in other control aspects it may be looked on from overseas with envy.

-

Depends how short term their outlook is, they have very minutely damaged the brand again perhaps, they have a high confidence in the product, which initially is great pitch, with apparently not much complexity to new customers. unless your have a prior experience comparator quite some years in the past. I worry about new customers, that have done large assessable in year transactions in preparation for coming over, arriving before mid-July and get taken to the cleaners the following January...

-

I won't be likely to be immediately affected by this change of posture by Thai RD , watching from afar in safe mode, with popcorn. I normally put a lottery ticket on an almost regular basis every month, in case my lucky number comes up! It's very easy and straight forward to by a ticket currently. If it were a very convoluted process, involving proof of Fx to buy the ticket and had to get it certified whilst the information involved in the transaction was quite obvious, In that case I might not put a ticket on, (or put myself in the situation that it would become a rare an infrequent consideration to buy a ticket, unless someone wanted or needed me to). In a similar fashion if it is a straight forward process to file a tax return in future, to get a receipt for an inward remittance, that may potentially cause a threat of some possible liability or penalty, hanging around like a fart in an elevator, I perhaps would rather put the ticket on to stop my unlucky number coming up. Yes, I may be an idiot for putting a lottery on, but when I was there last summer in a period of 4 weeks, they twice yielded much more than a large grocery shop at central.......so not impossible odds (unlike the UK one has been **** for for quite a while now) Good luck...

-

I was thinking more of a 10 year multi 180 day entry Visitors visa like The Thai's can get for the UK, (no 90 day reporting or TM30 would be nice.)

-

Over and above the Thai requirements, might you be traveling to Europe on Holiday at any point..... If you are planning to travel to an EU country (except Ireland), or Switzerland, Norway, Iceland, Liechtenstein, Andorra, Monaco, San Marino or Vatican City, follow the Schengen area passport requirements. Your passport must be: issued less than 10 years before the date you enter the country (check the 'date of issue') I got nearly the maximum add on time when I last renewed but will have to renew more than a year and a half early to be on the safe side! (had a short stay land side at CDG once due to an extended time of a flight connection) https://www.gov.uk/foreign-travel-advice/france/entry-requirements

-

Always carried the Son's Birth Cert Thai & English, (as suggested when I asked once at BKK when departing) Had Mum write a sentence on the Flight booking in English sayings agreed with the trip, and with her phone number. Haven't used the local office Amphur letter /doc. At least 3 round trips to UK without Mum, not asked for any proof. But all flight bookings were made months in advance, and logged on Airline systems as Family Companion traveller. Now over 16 so would not.anticipate any problems going forward.

-

If you left more than say 3000 baht in the account(s) when you left, send a 1000 baht to the account using one of the "free" Fx services to make a transaction on the account. Go into a main branch to get a new ATM card as soon as your back. (think ahead if they ask for a Thai address (no proof needed probably) If you just left a couple of hundred baht, the account likely may be toast.

-

Best keep accounts open if you can, I would leave approx. 4000 baht in each Thai Baht savings account + any fees for an active ATM etc, just top it up with a 1000baht every year. (Apart from FCD accounts where the typical minimum to avoid disintegration fees may be $1000 equivalent (+ATM card fees). Avoid the "do you have a work permit?" questions if you need them in future.