Ben Zioner

Advanced Member

-

Joined

-

Last visited

Everything posted by Ben Zioner

-

Right now everything is just dreamlike. Yesterday I had some delicious salmon lunch. We shared a bottle of white wine with my wife. Followed by apple crumble and coffee. Light dinner and a good night sleep. And zero pain, I just can feel the cut under the ribs this morning, but a level of 1 to 2, and the last paracetamol was 8 hours ago.

-

No comment

-

Well, I am 71 one, and I don't intend to drop my current cover, which includes also one of my daughters.

-

With afterthought, the problem with this thread's headline is "openly". Is there "something as an "openly rag head" or an "openly African American " ?

-

That's what they recommend, it is said that the majority patients return to their normal diets after a few weeks. I won't try McDonald's to soon though.. I think we have to do our homework, I have eaten full fat yoghurt, croissant, danish, cheese, without the slightest but of stomach upset nor diarrhoea, if I pass the lunch (salmon and white wine) test I'll take my Lady to Fuji tomorrow. But I'll take imodium (as PEP not PREP) with me, just in case.

-

How many tabs can you open?

-

Had my Gallbladder removed 48 hours ago a Bumrungrad by Dr. Theerapol. I am amazed by the effectiveness of the laparoscopic procedure [as performed by Dr Theerapol]. No pain [and no food] at all during the the first 24 hours, some mild soreness since yesterday. Four meals and even coffee so far, and no problems whatsoever, I'll try salmon with a glass of white wine for lunch. The downside being that I am going to get even fatter... Once more, ladies and gentlemen, if you settle in Thailand make sure you have a proper health cover and you'll be safe. The above procedure costs about 270k, which is what you'd pay in Switzerland. But why not you'll get great doctors and great nurses.

-

You need this for Internet browsing?

-

Yes, that's the Farang VAT.

-

Pu$$y Power

-

What is a "facial"? Like splashing all over her face?

-

Would make sense wouldn't?

-

Could someone explain why this answer get a "sad" emoticon, while it is 100% pertinent? Mysteries of AN and inability to overcome one's animosities?

-

Maybe just because US has been a well managed country for the past three years.

-

Local stuff is leass than 20% of what I buy. Holidays go overseas now as we all should minimize remittances.

-

Must say that I am not overly happy with Nord these days. They removed all the servers they had in Geneva. Only Zurich now. The number of servers is important as yo need to have a wide range of IPs for certain services.

-

So you just don't know what you are talking about, do you?

-

The irony...

-

This is a case where the "sad emotion" was totally pertinent. But what makes your post utterly ridiculous is that those who rained the largest amounts were mostly Japanese or Korean customers.

-

It is not, even under the current unfortunate xenophobic climate. For about 100 Euros, you get a few drinks and hour to chose the nymphet you can do back in your hotel. That's still cheap.

-

Used to be part of the fun, get 20 Baht notes for 500 or 1000 Baht and rain them down of the stage. The girls where like chooks at feeding time.. Not seen it happen recently. Everything has changed, not much fun left only a few nice young bodies for quickies, and even that gets off limit for whiteys in some places, certain days of the week. Now even Stickman agrees that there is an anti westerners mood around. Read his last columns.

-

Never had one. And he is mixture of Stalin and Reagan at a mental age of 4.

-

I would agree that "mentally challenged" is a bit strong, I would have phrased it as "pathologically resistant to [ineluctable] change".

-

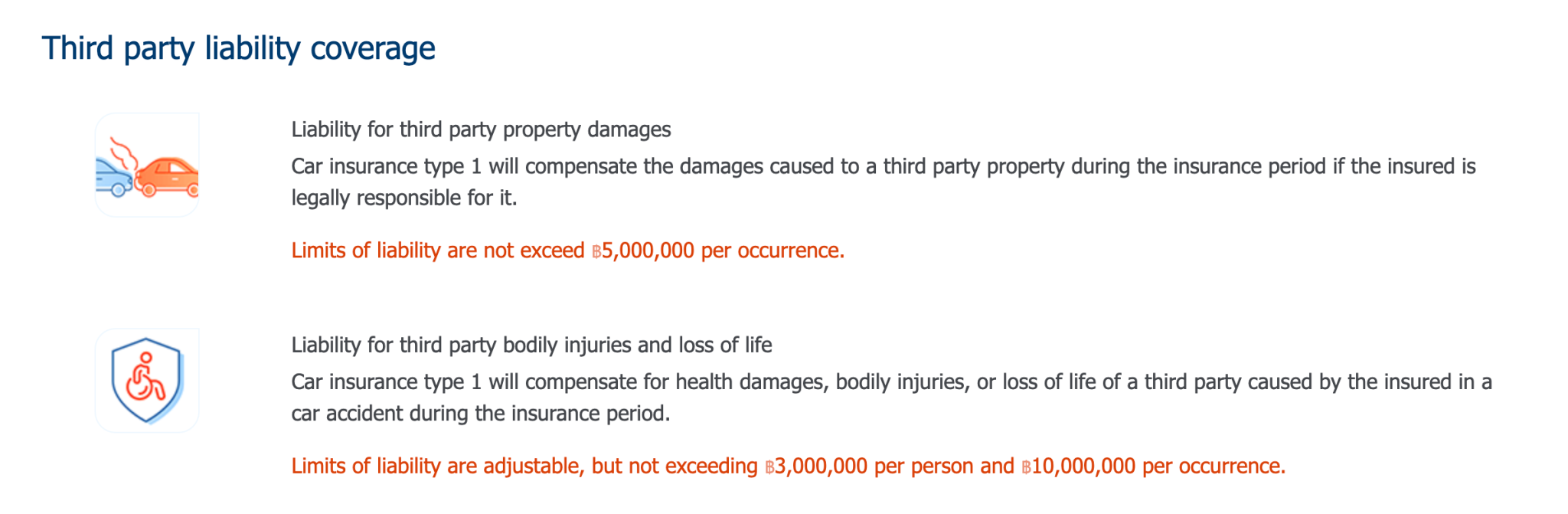

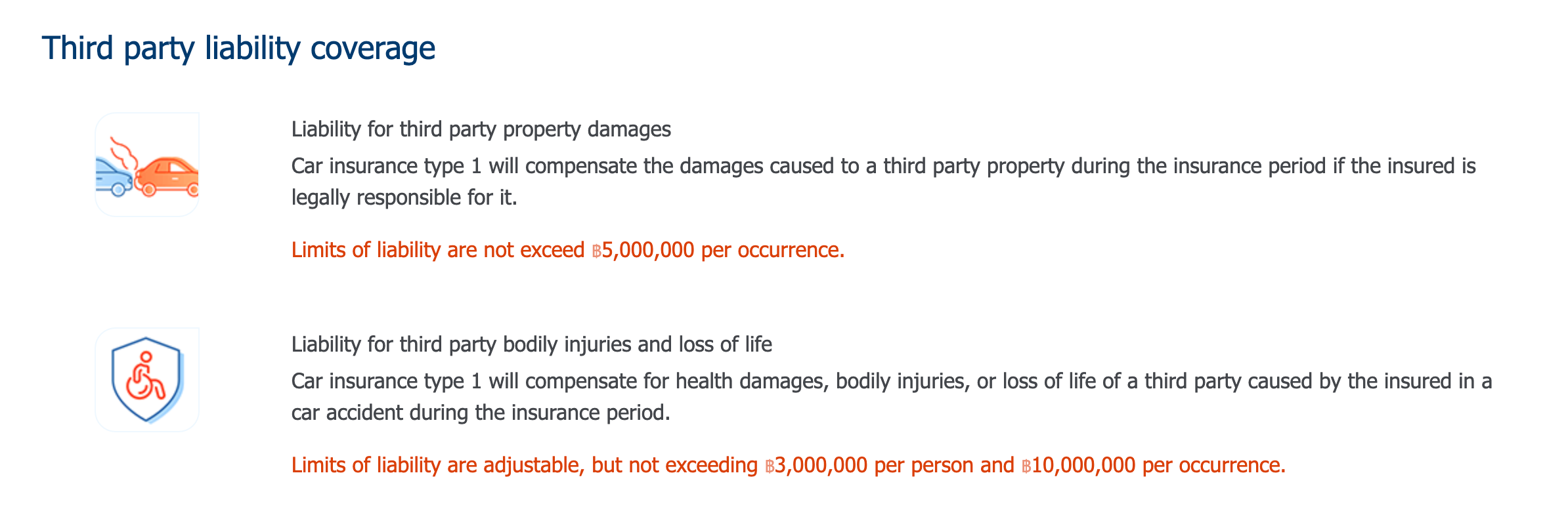

So, is that a reason not to let the Insurance representative handle the case? As the driver apparently did. At the dismay of the other injured party?

-

U ought to be specific.